Global Pro AV Market Report, Size, Share and Forecast 2026–2033

Global Pro AV Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

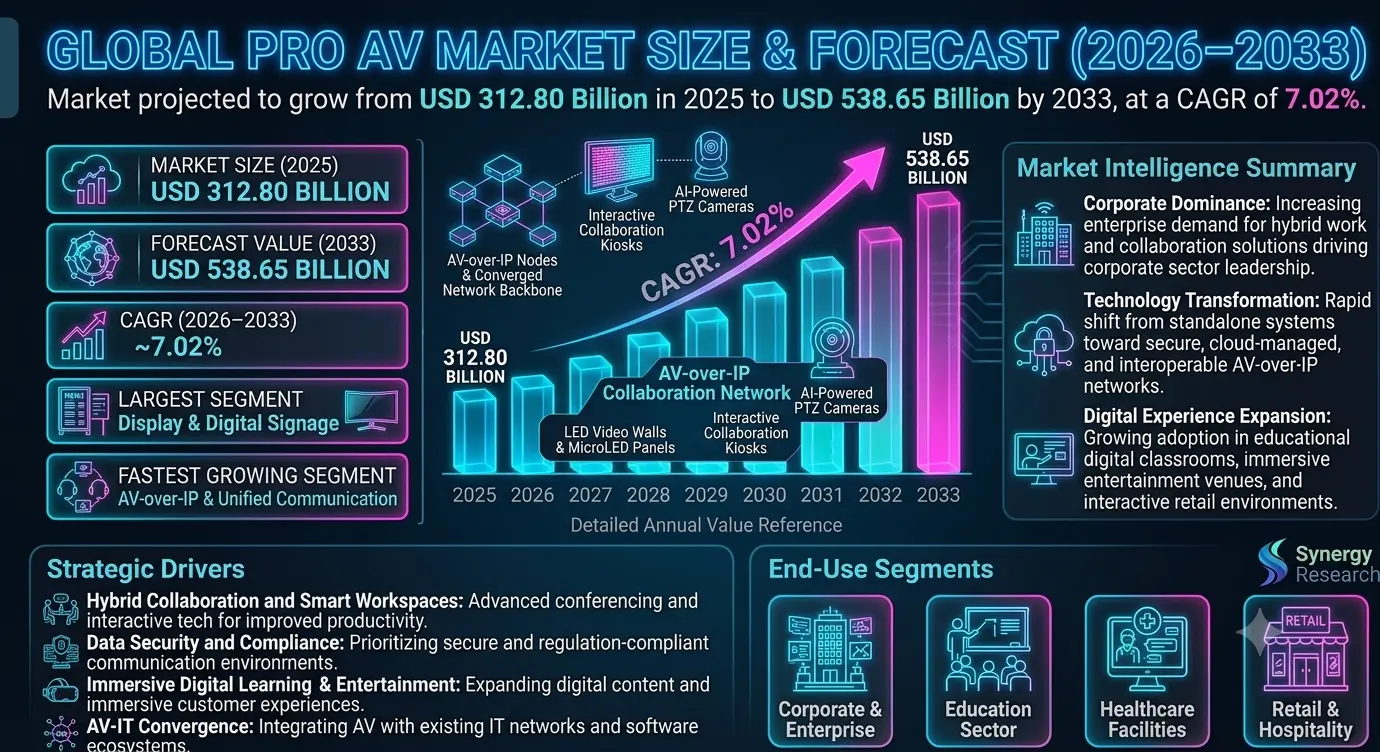

| Market Size (2025) | USD 312.80 Billion |

| Market Size (2033) | USD 538.65 Billion |

| CAGR (2026???2033) | 7.02% |

| Largest Segment | Display & Digital Signage Solutions |

| Fastest Growing Segment | AV-over-IP & Unified Communication Solutions |

| Leading End-Use Segment | Corporate & Enterprise Sector |

| Key Trend | Convergence of AV, IT Networks & Hybrid Collaboration Technologies |

| Regulatory Influence | Workplace Safety Standards, Data Security Regulations & Communication Compliance Requirements |

| Future Outlook | Growth Driven by Hybrid Workplaces, Smart Buildings & Digital Transformation Initiatives |

Global Pro AV Market Size & Forecast

The Global Professional Audio-Visual (Pro AV) Market is expected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at USD 312.80 billion in 2025 and is projected to reach approximately USD 538.65 billion by 2033, registering a CAGR of 7.02%. The market growth is primarily driven by increasing adoption of digital communication technologies, rising demand for hybrid workplace solutions, expansion of smart buildings, and growing investments in immersive customer experiences. Professional AV solutions have become essential across corporate environments, educational institutions, healthcare facilities, entertainment venues, hospitality establishments, and government organizations. In addition, advancements in AV-over-IP, cloud collaboration platforms, interactive displays, and AI-enabled communication systems are supporting long-term market expansion.Global Pro AV Market Overview

Professional Audio-Visual (Pro AV) solutions encompass integrated hardware, software, and services used for professional communication, collaboration, presentation, broadcasting, and digital engagement applications. The market includes displays, projectors, digital signage, conferencing systems, audio equipment, control systems, AV-over-IP solutions, streaming technologies, and managed AV services. Pro AV technologies are widely utilized across corporate offices, educational institutions, healthcare facilities, retail environments, transportation hubs, entertainment venues, and public infrastructure. The market is evolving from standalone AV systems toward network-connected, cloud-managed, and software-driven communication ecosystems.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid advancements in LED display technologies, AV-over-IP architectures, cloud collaboration platforms, AI-powered conferencing systems, and immersive audiovisual experiences are accelerating market growth. Organizations are increasingly adopting intelligent communication systems to improve productivity, collaboration, and customer engagement.Market Implications

Companies investing in next-generation AV platforms, software-defined infrastructure, and integrated communication technologies are expected to strengthen market leadership.2. Compliance and Risk Repricing

Data security requirements, workplace communication regulations, accessibility standards, and cybersecurity policies are influencing AV deployment strategies. Organizations are prioritizing secure and compliant communication environments.Market Implications

Firms offering secure, compliant, and interoperable AV solutions are likely to gain stronger market acceptance.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as AV equipment manufacturers, IT companies, software providers, system integrators, and managed service providers expand their portfolios. The convergence of AV, IT networking, cloud computing, and unified communications is reshaping value-chain dynamics.Market Implications

Companies focusing on integrated AV ecosystems and recurring service-based business models may gain stronger competitive advantages.4. Capital and Capacity Scaling

Increasing investments in smart workplaces, digital learning environments, connected healthcare infrastructure, and immersive entertainment facilities are supporting market expansion. Global digital transformation initiatives continue to accelerate Pro AV adoption.Market Implications

Organizations scaling cloud-based AV infrastructure and managed service capabilities are expected to capture future opportunities.Market Segmentation Analysis

By Solution Type

1. Display & Digital Signage Solutions

This remains the largest segment due to widespread adoption across corporate, retail, transportation, and public information applications.2. Audio Systems

Strong demand driven by conferencing, broadcasting, and event management applications.3. Video Conferencing & Collaboration Systems

Rapid growth supported by hybrid work and remote communication trends.4. Control & Management Systems

Widely used for centralized management of AV infrastructure.5. AV-over-IP Solutions

Fastest-growing segment due to scalability, flexibility, and network integration benefits.By Deployment Mode

1. On-Premises AV Systems

Largest segment due to extensive installations across enterprises and public infrastructure.2. Cloud-Based AV Solutions

Fast-growing segment driven by remote management and subscription-based service models.By End User

1. Corporate & Enterprise Sector

Largest segment due to increasing demand for collaboration and communication technologies.2. Education Sector

Strong adoption driven by digital classrooms and hybrid learning environments.3. Healthcare Facilities

Growing use in telemedicine, patient communication, and training applications.4. Retail & Hospitality

Increasing deployment of digital signage and customer engagement solutions.5. Entertainment & Media

Significant demand for live events, broadcasting, and immersive experiences.Regional Market Dynamics

North America

North America dominates the global Pro AV market due to advanced technology adoption, strong enterprise spending, and extensive deployment of collaboration solutions.Europe

Europe remains a major market supported by digital transformation initiatives, smart building projects, and enterprise modernization programs.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rapid urbanization, infrastructure development, smart city investments, and expanding corporate sectors.Latin America

Latin America is gradually expanding due to increasing adoption of digital communication and enterprise collaboration technologies.Middle East & Africa

The region is witnessing strong growth driven by smart city developments, hospitality expansion, and large-scale infrastructure projects.Competitive Landscape

The Global Pro AV Market is highly competitive with technology providers, AV equipment manufacturers, software vendors, and system integrators operating globally.Key Companies Operating in the Market Include:

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Sony Group Corporation

- Panasonic Holdings Corporation

- Cisco Systems, Inc.

- Crestron Electronics, Inc.

- Harman International Industries

- Barco NV

- Shure Incorporated

- AVI-SPL LLC

Strategic Outlook

The future of the Pro AV market will be shaped by AV-over-IP adoption, cloud-native collaboration platforms, AI-powered communication tools, and immersive digital experiences. Smart meeting rooms, virtual collaboration environments, interactive digital signage, and integrated workplace technologies will significantly improve organizational productivity and engagement. The rise of hybrid work models, smart infrastructure, and digital communication ecosystems is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Pro AV Market remains a vital segment within enterprise communication, digital transformation, and smart infrastructure ecosystems. Rising demand for collaboration technologies, immersive experiences, and connected communication platforms continues driving long-term market growth. Companies capable of delivering scalable, secure, intelligent, and integrated AV solutions will be best positioned to capture future opportunities. The convergence of audiovisual technologies, cloud computing, artificial intelligence, and enterprise collaboration is expected to redefine the future of the global Pro AV industry.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Pro AV Market Snapshot (2026???2033)

- 1.2 Market Size & Growth Overview

- 1.3 Key Market Highlights

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Performance Summary

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Market Introduction & Overview

- 2.1 Definition of Professional Audio-Visual (Pro AV) Solutions

- 2.2 Scope of the Global Pro AV Market

- 2.3 Evolution of Audio-Visual Communication Technologies

- 2.4 Pro AV Value Chain Analysis

- 2.5 Regulatory & Compliance Framework

- 2.6 Emerging Trends in Hybrid Collaboration & Smart Communication

- 2.7 Role of Pro AV in Digital Transformation & Smart Infrastructure

- 3. Research Methodology

- 3.1 Primary Research Approach

- 3.2 Secondary Research Sources

- 3.3 Market Size Estimation Methodology

- 3.4 Forecasting Assumptions (2026???2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Market Drivers

- 4.1.1 Rising Adoption of Hybrid Workplace Solutions

- 4.1.2 Expansion of Smart Buildings & Digital Infrastructure

- 4.1.3 Increasing Demand for Unified Communication Platforms

- 4.1.4 Growth in Digital Signage & Customer Engagement Solutions

- 4.1.5 Advancements in AV-over-IP & Cloud Collaboration Technologies

- 4.2 Market Restraints

- 4.2.1 High Initial Deployment & Integration Costs

- 4.2.2 Complex Interoperability Across Multiple Platforms

- 4.2.3 Cybersecurity & Data Privacy Concerns

- 4.3 Market Opportunities

- 4.3.1 Expansion of Smart Meeting Rooms & Collaboration Spaces

- 4.3.2 Growth in Cloud-Based AV Services

- 4.3.3 Adoption of AI-Powered Communication Tools

- 4.3.4 Increasing Investments in Digital Learning & Telehealth Infrastructure

- 4.4 Market Challenges

- 4.4.1 Managing Large-Scale AV Network Infrastructure

- 4.4.2 Ensuring Seamless User Experience Across Platforms

- 4.4.3 Rapid Technological Obsolescence & Upgrade Requirements

- 4.1 Market Drivers

- 5. Global Pro AV Market Size & Forecast (USD Billion), 2026???2033

- 5.1 Market Revenue Analysis

- 5.2 CAGR Analysis

- 5.3 Demand-Supply Trends

- 5.4 Pricing Analysis

- 5.5 Investment Trends

- 5.6 Future Market Outlook

- 6. Market Segmentation Analysis (USD Billion), 2026???2033

- 6.1 By Solution Type

- 6.1.1 Display & Digital Signage Solutions (Largest Segment)

- 6.1.2 Audio Systems

- 6.1.3 Video Conferencing & Collaboration Systems

- 6.1.4 Control & Management Systems

- 6.1.5 AV-over-IP Solutions (Fastest-Growing Segment)

- 6.2 By Deployment Mode

- 6.2.1 On-Premises AV Systems (Largest Segment)

- 6.2.2 Cloud-Based AV Solutions (Fastest-Growing Segment)

- 6.3 By End User

- 6.3.1 Corporate & Enterprise Sector (Largest Segment)

- 6.3.2 Education Sector

- 6.3.3 Healthcare Facilities

- 6.3.4 Retail & Hospitality

- 6.3.5 Entertainment & Media

- 6.1 By Solution Type

- 7. Regional Market Analysis

- 7.1 North America (Largest Market)

- 7.2 Europe

- 7.3 Asia-Pacific (Fastest-Growing Market)

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Competitive Benchmarking

- 8.3 Strategic Developments

- 8.4 Product Innovation & Unified Communication Strategies

- 8.5 Partnerships, Acquisitions & Expansion Analysis

- 9. Company Profiles

- 9.1 Samsung Electronics Co., Ltd.

- 9.2 LG Electronics Inc.

- 9.3 Sony Group Corporation

- 9.4 Panasonic Holdings Corporation

- 9.5 Cisco Systems, Inc.

- 9.6 Crestron Electronics, Inc.

- 9.7 Harman International Industries

- 9.8 Barco NV

- 9.9 Shure Incorporated

- 9.10 AVI-SPL LLC

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pro AV Demand Forecast Model

- 10.2 Hybrid Workplace Adoption Analysis

- 10.3 Unified Communication Growth Tracker

- 10.4 Smart Infrastructure Readiness Assessment

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of AV-over-IP & Cloud-Based Ecosystems

- 11.2 Investment in AI-Powered Collaboration Technologies

- 11.3 Growth Opportunities in Smart Buildings & Digital Workspaces

- 11.4 Strengthening Secure & Integrated Communication Platforms

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Market Research

- 14. Disclaimer

Competitive Landscape

Global Pro AV Market Competitive Intensity & Market Structure Overview

The global Professional Audio-Visual (Pro AV) market is highly competitive and moderately fragmented, characterized by the presence of global electronics manufacturers, enterprise communication technology providers, AV equipment specialists, software vendors, and system integration companies. Competitive intensity is primarily influenced by technological innovation, product interoperability, network integration capabilities, software-driven functionalities, and the ability to deliver end-to-end communication ecosystems.

Market participants compete across display technologies, conferencing systems, audio solutions, digital signage platforms, AV-over-IP infrastructure, and managed AV services. The growing convergence of audiovisual technologies with IT networks, cloud platforms, and unified communications is increasing competition and accelerating innovation throughout the industry.

The market structure is evolving from hardware-centric deployments toward integrated, software-defined, and cloud-managed AV ecosystems. Strategic partnerships between hardware manufacturers, software developers, and managed service providers are reshaping industry value chains and creating new recurring revenue opportunities.

Global Pro AV Market Competitive Intensity & Market Structure Current Scenario

Leading Global Pro AV Companies

Samsung Electronics Co., Ltd.: A leading provider of professional displays, digital signage solutions, LED video walls, and enterprise communication technologies with a strong global presence.

LG Electronics Inc.: Offers a comprehensive portfolio of commercial displays, digital signage solutions, interactive technologies, and smart workplace communication systems.

Sony Group Corporation: A major player in professional displays, broadcasting equipment, imaging solutions, and advanced audiovisual technologies for enterprise and entertainment applications.

Panasonic Holdings Corporation: Provides projectors, professional displays, collaboration technologies, and integrated AV solutions across multiple industry verticals.

Cisco Systems, Inc.: A global leader in enterprise collaboration platforms, video conferencing systems, unified communications, and network-based AV infrastructure.

Crestron Electronics, Inc.: Specializes in workplace automation, smart meeting room technologies, AV control systems, and enterprise collaboration solutions.

Harman International Industries: Offers professional audio systems, conferencing technologies, and integrated communication solutions through multiple global brands.

Barco NV: A recognized leader in visualization, collaboration technology, control room solutions, and professional display systems.

Shure Incorporated: A leading manufacturer of professional microphones, conferencing audio systems, and advanced communication technologies.

AVI-SPL LLC: A major global AV systems integrator providing managed services, workplace collaboration solutions, and enterprise communication infrastructure.

Key Competitive Intensity & Market Structure Drivers

The rapid adoption of hybrid work models and distributed collaboration environments is increasing demand for advanced conferencing systems, unified communication platforms, and intelligent workplace technologies.

The growing shift toward AV-over-IP architectures is transforming traditional audiovisual infrastructure by enabling scalability, centralized management, and seamless integration with enterprise IT networks.

Increasing demand for immersive customer experiences, digital signage, interactive displays, and smart building technologies is expanding competition across commercial and public-sector applications.

Cybersecurity requirements, data privacy regulations, and communication compliance standards are encouraging vendors to develop secure and enterprise-grade AV solutions.

The rise of cloud-based AV management platforms and subscription-driven service models is creating new competitive opportunities beyond traditional hardware sales.

Strategic Implications of Competitive Intensity & Market Structure

Companies offering integrated AV ecosystems that combine hardware, software, cloud services, and analytics capabilities are expected to achieve stronger competitive differentiation.

Investment in AI-powered collaboration tools, intelligent meeting room solutions, and real-time communication analytics is becoming increasingly important for long-term market leadership.

Organizations capable of delivering interoperable solutions across multiple communication platforms and enterprise environments are likely to gain stronger customer retention and recurring revenue streams.

Strategic partnerships among AV manufacturers, cloud providers, and IT infrastructure companies are becoming critical for expanding market reach and accelerating innovation.

Global service capabilities, managed AV offerings, and lifecycle support services are emerging as important competitive differentiators in large-scale enterprise deployments.

Global Pro AV Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global Pro AV market is expected to become increasingly software-driven as organizations continue investing in hybrid collaboration, smart workplaces, and digital engagement technologies. Competition will intensify around cloud-native communication platforms, intelligent automation, and integrated workplace ecosystems.

Industry participants are expected to accelerate investments in AI-enabled conferencing systems, AV-over-IP infrastructure, immersive visualization technologies, and cloud-based management platforms to strengthen their market positions.

The integration of artificial intelligence, machine learning, analytics, and automation into professional communication environments is expected to transform user experiences and operational efficiency across industries.

Over the forecast period, companies that successfully combine advanced technology innovation, cybersecurity, cloud connectivity, interoperability, and managed service capabilities will be best positioned to lead the evolving global Pro AV market.

Value Chain

Global Pro AV Market Value Chain & Supply Chain Evolution Overview

The Global Professional Audio-Visual (Pro AV) Market is undergoing a significant transformation driven by the convergence of audiovisual technologies, cloud computing, IT networking, artificial intelligence, and unified communications platforms. As organizations increasingly prioritize hybrid work environments, smart infrastructure, digital engagement, and immersive communication experiences, the Pro AV value chain is evolving from hardware-centric deployments toward integrated, software-defined, and service-oriented ecosystems. The market value chain spans component manufacturing, system design, software development, system integration, deployment services, managed support, and end-user operations.

A defining feature of the modern Pro AV ecosystem is the growing integration of AV technologies with enterprise IT networks and cloud-based collaboration platforms. Organizations are increasingly adopting connected communication systems that combine displays, conferencing solutions, digital signage, audio technologies, and centralized management software into unified environments that support productivity, engagement, and operational efficiency.

Supply chain complexity continues to increase due to global electronics sourcing, semiconductor dependencies, display manufacturing requirements, software integration needs, cybersecurity considerations, and demand for customized deployment models. Market participants must coordinate across component suppliers, hardware manufacturers, software providers, cloud platform vendors, system integrators, distributors, and managed service providers while ensuring performance, interoperability, scalability, and regulatory compliance.

Companies are investing heavily in AI-powered collaboration platforms, AV-over-IP technologies, cloud-native management systems, smart building integrations, and digital workplace infrastructure to improve service delivery and create recurring revenue opportunities. The value chain is increasingly becoming digital, connected, subscription-based, and data-driven.

Global Pro AV Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Component Manufacturing: Production of displays, cameras, microphones, speakers, processors, semiconductors, networking equipment, and control hardware.

- System Design & Product Development: Development of AV platforms, conferencing systems, digital signage solutions, AV-over-IP technologies, and management software.

- Software & Platform Integration: Integration of cloud collaboration platforms, unified communications systems, AI-enabled analytics, and centralized AV management solutions.

- System Integration & Deployment: Installation, configuration, customization, testing, and deployment of Pro AV infrastructure across end-user environments.

- Distribution & Managed Services: Distribution networks, value-added resellers, managed AV service providers, and cloud-based support services.

- End User Operations: Corporate enterprises, educational institutions, healthcare facilities, hospitality venues, retail environments, government agencies, and entertainment facilities.

Company-to-Stage Mapping

- Component Manufacturing: Samsung Electronics Co., Ltd., LG Electronics Inc., Sony Group Corporation, Panasonic Holdings Corporation.

- System Design & Product Development: Cisco Systems, Inc., Crestron Electronics, Inc., Harman International Industries, Barco NV.

- Software & Platform Integration: Cisco Systems, Microsoft Teams ecosystem partners, cloud collaboration platform providers, AV software developers.

- System Integration & Deployment: AVI-SPL LLC, global AV integrators, enterprise technology solution providers, smart building specialists.

- Distribution & Managed Services: AV distributors, managed service providers, cloud-based AV management providers, technology resellers.

- End User Operations: Corporate enterprises, universities, healthcare organizations, retail chains, hospitality operators, transportation hubs, and government agencies.

Key Value Chain & Supply Chain Evolution Signals in Global Pro AV Market

Expansion of AV-over-IP Architectures

Organizations are increasingly replacing traditional AV infrastructure with IP-based systems that provide greater scalability, interoperability, centralized management, and cost efficiency.

Acceleration of Hybrid Workplace Technology Adoption

Growing demand for seamless communication between remote and in-office employees is driving investments in conferencing systems, collaboration platforms, and intelligent meeting room technologies.

Growth of Cloud-Native AV Management Platforms

Cloud-based monitoring, remote diagnostics, centralized control, and subscription-based AV services are becoming essential components of modern deployment strategies.

Increasing Integration of AI-Powered Communication Solutions

Artificial intelligence is improving conferencing experiences through automated transcription, meeting analytics, speaker tracking, noise suppression, and content optimization.

Rising Demand for Smart Building Integration

Pro AV systems are increasingly connected with building automation platforms, occupancy management systems, energy controls, and digital workplace technologies.

Expansion of Managed and Recurring-Service Business Models

Organizations are shifting from one-time equipment purchases toward managed services, subscription-based collaboration platforms, and lifecycle support contracts.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Software-Defined AV Ecosystems

Companies developing software-centric AV solutions and cloud-enabled management platforms are expected to strengthen long-term competitive positioning.

Expansion of Integrated Collaboration Platforms

Combining audiovisual technologies with unified communications and workplace productivity tools will create stronger customer value and recurring revenue opportunities.

Strengthening Cybersecurity and Compliance Capabilities

As AV systems become increasingly network-connected, organizations must prioritize secure communication environments and regulatory compliance requirements.

Optimization of Global Electronics Supply Chains

Diversified sourcing strategies and resilient component supply networks will remain critical for ensuring operational continuity and managing supply disruptions.

Scaling Managed Service Offerings

Remote monitoring, proactive maintenance, and cloud-based support services will become increasingly important differentiators in the Pro AV market.

Strategic Partnerships Across AV and IT Ecosystems

Collaboration between hardware manufacturers, software providers, cloud vendors, and system integrators will accelerate innovation and improve customer outcomes.

Global Pro AV Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the Pro AV value chain is expected to evolve into a highly connected, cloud-enabled, and intelligence-driven communication ecosystem that supports hybrid work, digital engagement, and smart infrastructure initiatives worldwide.

Key Future Developments Include:

- Widespread adoption of AV-over-IP technologies across enterprise and institutional environments.

- Expansion of AI-powered collaboration tools and intelligent communication platforms.

- Growth of cloud-managed AV infrastructure and subscription-based service models.

- Increasing integration of Pro AV systems with smart building and workplace management platforms.

- Strengthening cybersecurity frameworks for network-connected AV environments.

- Expansion of immersive communication technologies including interactive displays, virtual collaboration environments, and advanced digital signage systems.

As the market evolves, competitive advantage will increasingly depend on the ability to integrate hardware innovation, cloud software capabilities, intelligent analytics, cybersecurity, and managed services within a unified communication ecosystem.

Companies that successfully combine advanced AV technologies, cloud-native platforms, AI-driven collaboration tools, scalable service models, and resilient supply chain operations will achieve stronger market positioning, customer retention, and long-term growth in the Global Pro AV Market.

Investment Activity

Global Pro AV Market Investment & Funding Dynamics Overview

The Global Professional Audio-Visual (Pro AV) Market is witnessing strong investment activity driven by the increasing adoption of hybrid workplace technologies, enterprise digital transformation initiatives, smart building deployments, and the growing demand for advanced collaboration and communication solutions. Technology providers, AV equipment manufacturers, cloud communication vendors, system integrators, private equity firms, and institutional investors are actively investing in AV-over-IP infrastructure, cloud-based collaboration platforms, digital signage ecosystems, intelligent conferencing technologies, and integrated workplace communication solutions.

Investment momentum is accelerating as organizations prioritize seamless communication, remote collaboration, immersive customer engagement, and intelligent workplace experiences. Capital allocation is increasingly focused on AI-powered conferencing systems, unified communication platforms, interactive display technologies, network-based AV systems, and software-driven AV management solutions.

Additionally, growing investments in smart buildings, digital learning environments, connected healthcare facilities, immersive entertainment technologies, and cloud-managed AV ecosystems are creating substantial long-term opportunities across the global Pro AV industry.

Global Pro AV Market Investment & Funding Dynamics Current Scenario

Currently, the market is experiencing significant capital inflows as enterprises, educational institutions, healthcare organizations, and government agencies modernize communication infrastructure. Leading market participants are investing heavily in cloud-native collaboration platforms, AV-over-IP technologies, digital signage networks, intelligent control systems, and AI-enabled workplace solutions.

The market is attracting strong venture capital funding, corporate investments, and strategic partnerships targeting collaboration software providers, workplace technology innovators, immersive experience developers, and managed AV service providers. Investors are prioritizing organizations with scalable subscription-based business models, recurring service revenues, and integrated communication ecosystems.

Furthermore, the industry is witnessing increasing levels of mergers, acquisitions, technology alliances, and strategic collaborations among AV manufacturers, software developers, cloud providers, and system integrators to strengthen market positioning and accelerate innovation.

Key Investment & Funding Dynamics Signals in Global Pro AV Market

- Growing demand for hybrid workplace and enterprise collaboration solutions is accelerating investment across Pro AV technologies.

- Expansion of AV-over-IP architectures and unified communication platforms is driving funding toward network-connected AV ecosystems.

- Rising adoption of cloud-managed AV services and subscription-based communication platforms is supporting long-term capital deployment.

- Strategic investments in AI-powered conferencing systems, smart meeting rooms, and intelligent workplace technologies are enhancing operational efficiency.

- Increasing demand for interactive digital signage, immersive customer experiences, and real-time content management systems is strengthening investment activity.

- Partnerships between AV equipment manufacturers, software providers, cloud vendors, and system integrators are accelerating technology commercialization.

- Growing focus on cybersecurity, interoperability, compliance, and secure communication environments is reinforcing investor confidence.

Strategic Implications of Investment & Funding Dynamics in Global Pro AV Market

- Continuous investment in AV-over-IP infrastructure, cloud collaboration technologies, and intelligent communication systems is essential for maintaining market competitiveness.

- Capital allocation toward software-driven AV platforms, managed services, and integrated communication ecosystems will strengthen long-term market positioning.

- Companies offering scalable, secure, cloud-connected, and AI-enabled AV solutions are expected to achieve stronger customer adoption.

- Strategic acquisitions and partnerships will accelerate technology innovation, platform integration, and geographic expansion opportunities.

- Investments in smart buildings, immersive experiences, workplace modernization, and digital transformation initiatives will remain key growth priorities.

- Compliance with data security regulations, workplace communication standards, and cybersecurity requirements will continue influencing funding decisions.

- Organizations developing end-to-end AV ecosystems combining hardware, software, cloud services, and managed support are expected to capture substantial future value.

Global Pro AV Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Pro AV Market is expected to maintain strong investment momentum driven by increasing enterprise digitalization, expansion of hybrid work environments, smart infrastructure development, and rising demand for immersive communication technologies.

Future capital deployment will increasingly focus on AI-enabled collaboration platforms, cloud-native AV solutions, virtual and augmented reality integration, advanced digital signage networks, and intelligent workplace ecosystems.

As organizations continue modernizing communication infrastructure and enhancing employee and customer engagement, investment activity is expected to expand across AV innovation, managed services, software platforms, and global deployment capabilities.

In conclusion, the Global Pro AV Market represents an attractive technology investment landscape where hybrid collaboration, AV-over-IP technologies, cloud communication platforms, smart building integration, artificial intelligence, and immersive digital experiences will define future funding priorities, competitive dynamics, and long-term industry growth.

Technology & Innovation

Global Pro AV Market Technology & Innovation Landscape Overview

The Global Professional Audio-Visual (Pro AV) Market is undergoing a significant technological transformation driven by advancements in AV-over-IP architectures, cloud-based collaboration platforms, artificial intelligence (AI), immersive display technologies, unified communications, and smart building integration. The market demonstrates high innovation intensity as organizations increasingly prioritize seamless communication, digital engagement, hybrid collaboration, and intelligent workplace experiences.

At the center of this transformation is the convergence of traditional AV infrastructure with IT networks, cloud computing environments, and software-defined communication platforms. This shift is enabling organizations to deploy scalable, centrally managed, and highly interoperable audiovisual ecosystems across enterprise, education, healthcare, hospitality, retail, and public sector environments.

A major innovation area is AV-over-IP technology, where audio, video, and control signals are transmitted over standard network infrastructure. This approach improves system scalability, simplifies deployment, enhances flexibility, and enables remote management of complex AV environments.

The market is also witnessing rapid advancement in display technologies, including direct-view LED displays, microLED systems, interactive touchscreens, high-resolution video walls, transparent displays, and immersive visualization platforms that improve communication effectiveness and audience engagement.

Organizations are increasingly investing in AI-powered conferencing systems equipped with intelligent camera tracking, automated framing, voice recognition, real-time transcription, language translation, and meeting analytics capabilities to improve hybrid collaboration experiences.

Product innovation further includes cloud-native AV management platforms, wireless presentation systems, digital signage software, content management solutions, virtual event technologies, and integrated workplace communication ecosystems.

Additionally, smart building integration technologies are enabling Pro AV systems to interact with lighting controls, occupancy sensors, security platforms, environmental controls, and building management systems for improved operational efficiency.

The convergence of AV-over-IP, cloud computing, AI-enabled collaboration tools, immersive display technologies, and smart infrastructure integration is redefining the future technology landscape of the global Pro AV market.

Global Pro AV Market Technology & Innovation Landscape Current Scenario

Currently, the Global Pro AV Market demonstrates strong innovation activity across networked AV solutions, intelligent communication platforms, digital display systems, and cloud-based management technologies. Organizations are increasingly deploying integrated AV ecosystems to support hybrid work, digital learning, and customer engagement initiatives.

1. AV-over-IP Infrastructure

AV-over-IP solutions are rapidly replacing traditional matrix-switching architectures by enabling scalable, flexible, and centrally managed audiovisual distribution across enterprise networks.

2. AI-Powered Collaboration Technologies

Artificial intelligence is enhancing conferencing systems through automated meeting management, speaker tracking, background noise suppression, real-time translation, and intelligent analytics.

3. Advanced Display & Visualization Systems

High-resolution LED walls, microLED displays, interactive panels, and immersive visualization technologies are improving communication quality and user engagement.

4. Cloud-Based AV Management Platforms

Cloud-native solutions enable remote monitoring, device management, software updates, content distribution, and performance optimization across distributed AV environments.

5. Wireless Presentation & Collaboration Systems

Organizations are increasingly adopting wireless connectivity solutions that improve meeting room flexibility and support bring-your-own-device (BYOD) environments.

6. Smart Building & IoT Integration

Pro AV platforms are increasingly integrated with IoT devices, occupancy analytics, environmental sensors, and building management systems to improve operational intelligence.

Key Technology & Innovation Landscape Signals in Global Pro AV Market

Several innovation signals are shaping the future development of the market:

1. Expansion of Hybrid Work Technologies

Organizations continue investing in intelligent collaboration systems that support seamless interaction between in-office and remote participants.

2. Growing Adoption of AV-over-IP Architectures

Network-based AV infrastructure is becoming the preferred deployment model due to scalability, interoperability, and centralized management capabilities.

3. Rise of AI-Enabled Communication Systems

AI technologies are increasingly improving meeting productivity, communication quality, and user experiences across enterprise environments.

4. Increased Demand for Immersive Experiences

Immersive displays, virtual collaboration environments, and interactive engagement platforms are gaining widespread adoption.

5. Cloud-Native AV Ecosystem Growth

Cloud-managed AV solutions are supporting remote administration, predictive maintenance, and scalable service delivery models.

6. Integration with Smart Buildings

Connected AV systems are becoming critical components of intelligent workplace and smart infrastructure strategies.

7. Enhanced Cybersecurity Focus

As AV systems become increasingly network-connected, cybersecurity and secure communication protocols are becoming essential technology priorities.

Strategic Implications of Technology & Innovation Landscape in Global Pro AV Market

The evolving technology landscape is significantly reshaping competition across the Pro AV industry. Companies are increasingly competing on interoperability, software capabilities, cloud integration, AI functionality, user experience, and cybersecurity performance.

Organizations investing in AV-over-IP infrastructure, AI-powered collaboration platforms, advanced display technologies, and cloud-based management systems are expected to strengthen their market positioning.

Strategic partnerships between AV manufacturers, software vendors, cloud providers, network infrastructure companies, and workplace technology specialists are accelerating innovation and commercialization activities.

The growing convergence of audiovisual technologies, enterprise IT systems, cloud computing, AI analytics, and smart building infrastructure is creating strong opportunities for operational efficiency and long-term differentiation.

Additionally, increasing requirements for secure communications, accessibility compliance, workplace productivity, and digital transformation initiatives are encouraging continued investment in next-generation Pro AV technologies.

Global Pro AV Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026???2033, the Global Pro AV Market is expected to experience substantial technological advancement driven by intelligent collaboration, immersive communication, cloud-native platforms, and connected workplace ecosystems.

Future technological developments are likely to include:

1. AI-Driven Unified Collaboration Platforms

Advanced AI capabilities will automate meeting management, content generation, translation services, communication analytics, and productivity optimization.

2. Next-Generation AV-over-IP Ecosystems

Higher-bandwidth network architectures and software-defined AV systems will further improve scalability, flexibility, and interoperability.

3. Immersive Extended Reality (XR) Experiences

Virtual reality, augmented reality, and mixed reality technologies will expand enterprise collaboration, training, education, and customer engagement applications.

4. Intelligent Smart Workplace Integration

AV systems will become increasingly integrated with workplace analytics, occupancy management, environmental controls, and building automation platforms.

5. Advanced Cloud-Based AV Operations

Cloud-native management solutions will support predictive maintenance, remote optimization, automated diagnostics, and centralized control.

6. Interactive Digital Signage Evolution

AI-enhanced digital signage systems will deliver personalized, data-driven, and context-aware content experiences.

7. Enhanced Cybersecurity & Data Protection Frameworks

Advanced security architectures, encrypted communications, and zero-trust networking models will strengthen protection for connected AV environments.

In conclusion, companies capable of combining AV-over-IP innovation, AI-powered communication tools, immersive visualization technologies, cloud-based management platforms, smart building integration, and secure collaboration ecosystems will be best positioned to lead the future evolution of the Global Pro AV Market.

Market Risk

Global Pro AV Market: Risk Factors & Disruption Threats Overview

The Global Professional Audio-Visual (Pro AV) Market is evolving rapidly as organizations invest in hybrid workplaces, smart buildings, digital communication platforms, and immersive customer experiences. While the market benefits from strong digital transformation trends, it remains exposed to a variety of technological, operational, cybersecurity, and economic risks that can affect adoption rates, investment cycles, and long-term profitability.

One of the most significant risk factors is the increasing convergence of AV and IT infrastructures. As AV systems become more dependent on cloud platforms, network connectivity, and software-defined architectures, organizations face greater complexity in deployment, integration, and ongoing system management. Compatibility challenges between hardware, software, and networking environments may delay implementations and increase operational costs.

Cybersecurity has emerged as a major disruption threat. Connected conferencing systems, cloud-managed AV platforms, digital signage networks, and collaboration tools can become targets for cyberattacks, unauthorized access, data breaches, and service disruptions. Security vulnerabilities can negatively impact business continuity and regulatory compliance.

Rapid technological change also creates market uncertainty. Continuous advancements in AV-over-IP, artificial intelligence, immersive media, extended reality (XR), and collaboration technologies can shorten product lifecycles and increase pressure on organizations to upgrade existing infrastructure more frequently.

Economic conditions and enterprise spending patterns represent another important risk. Pro AV investments are often tied to capital expenditure budgets and workplace modernization initiatives. Economic slowdowns, reduced corporate spending, or delayed infrastructure projects may temporarily affect market demand.

In addition, supply chain disruptions involving semiconductors, displays, networking equipment, and electronic components can impact manufacturing schedules, project timelines, and equipment availability across global markets.

Global Pro AV Market: Current Risk Scenario

The current market environment is characterized by growing demand for hybrid collaboration solutions, cloud-based AV platforms, and smart communication technologies. However, organizations continue to face implementation challenges associated with system interoperability, cybersecurity requirements, and rising technology costs.

The increasing adoption of AV-over-IP solutions is driving greater dependence on enterprise network infrastructure. This shift requires enhanced network performance, cybersecurity measures, and IT expertise to ensure reliable operation.

Cloud-based AV deployments are expanding rapidly, but concerns regarding data privacy, regulatory compliance, and service availability remain important considerations for enterprises and public sector organizations.

Inflationary pressures and higher technology procurement costs are also influencing purchasing decisions, particularly among small and medium-sized enterprises with limited digital transformation budgets.

Furthermore, the shortage of skilled AV and IT integration professionals continues to create deployment and support challenges across large-scale enterprise and infrastructure projects.

Key Risk Factors & Disruption Threats Signals

- Cybersecurity Vulnerabilities: Connected AV platforms and collaboration systems face increasing risks from cyberattacks, data breaches, and unauthorized access.

- Technology Obsolescence: Rapid innovation in AV, AI, cloud, and immersive technologies may shorten equipment lifecycles and increase upgrade requirements.

- System Integration Complexity: Convergence of AV, IT, networking, and cloud environments may create interoperability and deployment challenges.

- Supply Chain Disruptions: Shortages of displays, semiconductors, networking hardware, and electronic components can affect project delivery timelines.

- Economic & Budgetary Constraints: Reduced enterprise spending and delayed infrastructure investments may impact market demand.

- Data Privacy & Compliance Risks: Cloud-based communication systems must comply with evolving security, privacy, and accessibility regulations.

- Workforce Skills Gap: Limited availability of qualified AV integrators, network specialists, and support professionals may constrain project execution.

Strategic Implications of Risk Factors & Disruption Threats

The evolving risk landscape is encouraging Pro AV vendors and service providers to prioritize cybersecurity, interoperability, and cloud-native architectures. Organizations are increasingly investing in secure communication platforms, encrypted data transmission, and proactive threat monitoring to reduce cyber risks.

Manufacturers are expanding software-driven solutions and managed service offerings to create recurring revenue streams while helping customers simplify system management and technology upgrades.

Strategic partnerships between AV vendors, IT providers, cloud platform operators, and system integrators are becoming increasingly important to deliver seamless end-to-end communication ecosystems.

Companies are also investing in workforce training and certification programs to address talent shortages and support the growing complexity of integrated AV environments.

Global Pro AV Market: Forward Risk Outlook

Looking ahead, the Pro AV market is expected to remain exposed to moderate-to-high technology and cybersecurity risks as organizations continue migrating toward connected, intelligent, and cloud-managed communication infrastructures.

Emerging technologies such as AI-powered collaboration tools, extended reality (XR), immersive digital experiences, and software-defined AV ecosystems will create new growth opportunities while simultaneously increasing system complexity and security requirements.

Regulatory oversight concerning data privacy, workplace accessibility, and digital communications compliance is expected to strengthen, requiring organizations to maintain robust governance and compliance frameworks.

Supply chain resilience, cybersecurity readiness, interoperability capabilities, and recurring service-based business models will remain critical success factors for market participants seeking sustainable growth.

Overall, the Global Pro AV Market will continue to evolve within a highly dynamic technology environment shaped by digital transformation, hybrid work adoption, and intelligent communication ecosystems. Companies that successfully combine innovation, security, scalability, and operational resilience will be best positioned to capitalize on future market opportunities while mitigating disruption risks.

Regulatory Landscape

Global Pro AV Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Professional Audio-Visual (Pro AV) Market is evolving alongside the increasing convergence of audiovisual technologies, information technology (IT) infrastructure, cloud communications, and digital collaboration ecosystems. Governments, regulatory authorities, and industry organizations are focusing on workplace safety, cybersecurity, accessibility, data privacy, and communication compliance standards to ensure the secure and effective deployment of professional AV solutions across commercial, educational, healthcare, and public-sector environments.

Pro AV solution providers, system integrators, equipment manufacturers, and cloud communication vendors must comply with a broad range of regulations governing electronic equipment safety, network security, digital communications, accessibility requirements, data protection, and spectrum usage. As AV systems become increasingly connected and software-driven, regulatory oversight is expanding beyond hardware compliance to include cybersecurity and digital governance requirements.

The growing adoption of hybrid workplaces, smart buildings, digital learning environments, and cloud-based collaboration platforms is encouraging regulatory agencies to strengthen standards related to communication reliability, information security, and user accessibility.

Global Pro AV Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by increasing attention to data security, workplace technology standards, and digital communication compliance. Organizations deploying Pro AV systems are required to ensure that conferencing platforms, collaboration tools, and network-connected AV devices comply with applicable privacy, cybersecurity, and enterprise governance requirements.

Workplace safety regulations continue to influence the installation and operation of AV systems in commercial buildings, educational institutions, healthcare facilities, and public venues. Compliance with electrical safety standards, fire protection requirements, emergency communication systems, and occupational health guidelines remains essential for deployment projects.

Data privacy regulations are becoming increasingly important as video conferencing, cloud collaboration, digital signage analytics, and AI-powered communication platforms collect and process user information. Organizations must ensure compliance with regional and national data protection laws governing information storage, transmission, and access controls.

Accessibility regulations are also playing a significant role in market development. Governments are promoting inclusive communication environments by requiring support for captioning, hearing assistance technologies, accessible digital displays, and other features that improve access for individuals with disabilities.

At the same time, cybersecurity frameworks are expanding to address risks associated with connected AV devices, cloud-managed platforms, and enterprise communication networks. Organizations are increasingly prioritizing secure architectures, encrypted communications, and network monitoring capabilities to meet evolving compliance expectations.

Key Regulatory & Policy Environment Signals in Global Pro AV Market

- Workplace Safety Standards: Regulations governing safe installation, operation, and maintenance of AV equipment in commercial and public environments.

- Data Privacy & Protection Requirements: Compliance obligations for video conferencing platforms, cloud collaboration tools, and digital communication systems handling user data.

- Cybersecurity Regulations: Growing focus on securing connected AV devices, communication networks, and cloud-based collaboration ecosystems.

- Accessibility Compliance Standards: Requirements supporting inclusive communication through captioning, assistive technologies, and accessible audiovisual content.

- Electronic Equipment Certification: Product safety, electromagnetic compatibility (EMC), and performance certification requirements for AV hardware manufacturers.

- Communication & Broadcasting Compliance: Regulatory oversight of professional communication systems, digital signage deployments, and media transmission infrastructure.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging organizations to prioritize secure, compliant, and interoperable AV solutions capable of supporting increasingly complex communication requirements. Compliance capabilities are becoming an important competitive differentiator for manufacturers, software vendors, and system integrators.

Cybersecurity regulations are driving investments in encrypted communications, secure device management, network segmentation, and cloud security technologies. AV vendors that can demonstrate strong security credentials are likely to gain greater acceptance in enterprise, healthcare, and government deployments.

Data privacy requirements are influencing the design of collaboration platforms and communication ecosystems, encouraging vendors to implement transparent data handling practices, stronger access controls, and compliance-oriented software architectures.

Accessibility mandates are creating opportunities for solution providers offering inclusive communication technologies, advanced captioning systems, hearing assistance solutions, and accessible digital engagement platforms across public and private sectors.

Overall, regulatory compliance is becoming increasingly integrated into purchasing decisions, particularly among large enterprises, educational institutions, healthcare organizations, and government agencies seeking long-term operational reliability and risk management.

Global Pro AV Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global Pro AV market is expected to become more comprehensive as organizations continue adopting cloud-native collaboration platforms, AI-enabled communication tools, and network-connected AV ecosystems. Policymakers are likely to introduce stronger requirements governing cybersecurity, digital resilience, and communication infrastructure reliability.

Data protection regulations are expected to expand further, requiring greater transparency regarding data collection, storage, analytics, and cross-border information transfers within collaborative communication environments.

Cybersecurity compliance standards will likely become increasingly stringent, particularly for AV-over-IP systems, smart building integrations, and cloud-managed communication platforms. Security certification and continuous monitoring capabilities are expected to become standard procurement requirements.

Accessibility regulations are anticipated to broaden globally, driving increased adoption of inclusive communication technologies and standardized accessibility features across enterprise and public-sector deployments.

Overall, the future regulatory landscape will be defined by the convergence of workplace technology governance, cybersecurity oversight, digital communication compliance, and accessibility standards. Companies capable of delivering secure, compliant, scalable, and interoperable Pro AV solutions will be best positioned to capitalize on long-term opportunities within the rapidly evolving global audiovisual ecosystem.