Global Vendor Management System (VMS) Market Report, Size, Share and Forecast 2026–2033

Global Vendor Management System (VMS) Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

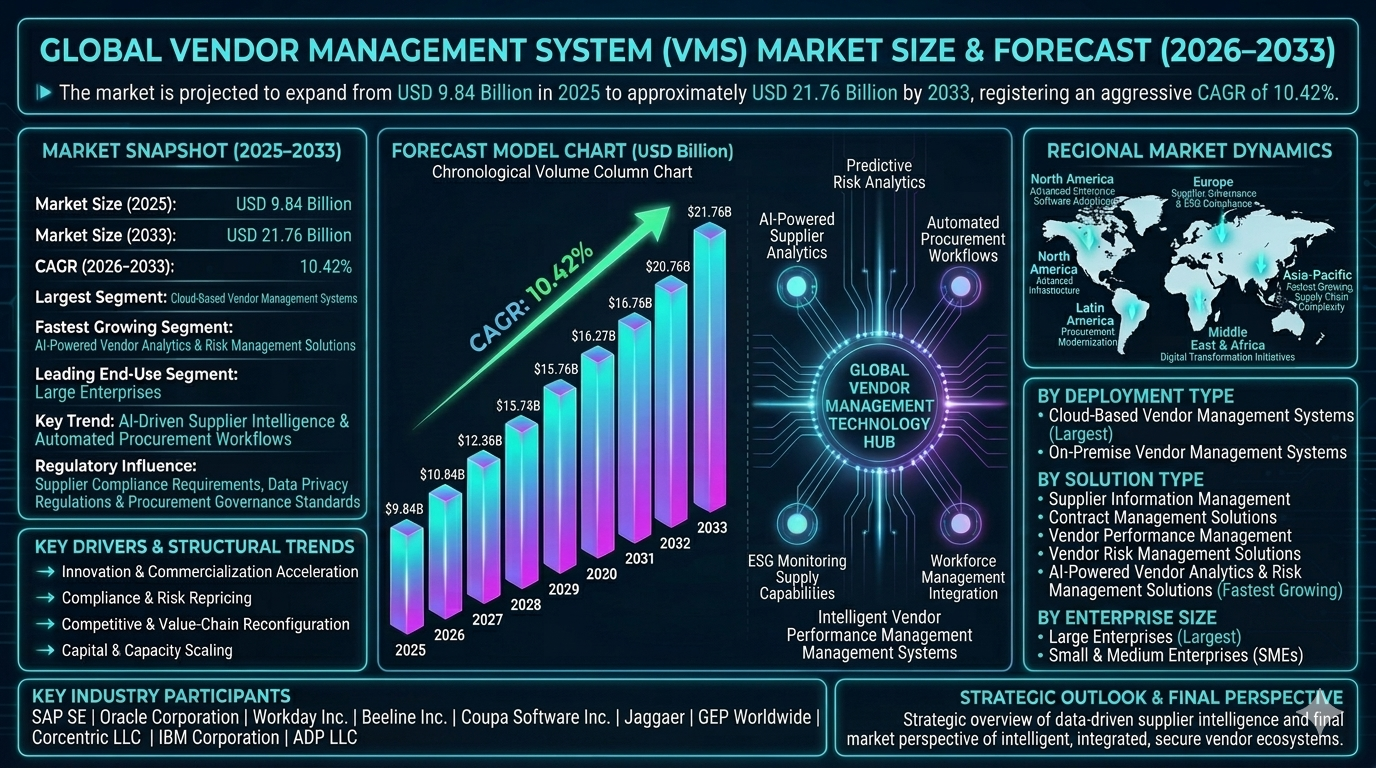

| Market Size (2025) | USD 9.84 Billion |

| Market Size (2033) | USD 21.76 Billion |

| CAGR (2026???2033) | 10.42% |

| Largest Segment | Cloud-Based Vendor Management Systems |

| Fastest Growing Segment | AI-Powered Vendor Analytics & Risk Management Solutions |

| Leading End-Use Segment | Large Enterprises |

| Key Trend | AI-Driven Supplier Intelligence & Automated Procurement Workflows |

| Regulatory Influence | Supplier Compliance Requirements, Data Privacy Regulations & Procurement Governance Standards |

| Future Outlook | Growth Driven by Digital Procurement, Third-Party Risk Management & Supply Chain Visibility |

Global Vendor Management System (VMS) Market Size & Forecast

The Global Vendor Management System (VMS) Market is expected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 9.84 billion in 2025 and is projected to reach approximately USD 21.76 billion by 2033, registering a CAGR of 10.42%. The market growth is primarily driven by increasing demand for supplier visibility, growing procurement digitization initiatives, rising third-party risk management requirements, and expanding global supply chain networks. Vendor Management Systems are becoming critical tools for organizations seeking to streamline supplier onboarding, contract management, procurement workflows, performance monitoring, and compliance tracking. In addition, the adoption of cloud computing, artificial intelligence, analytics platforms, and automated procurement technologies is supporting long-term market expansion.Global Vendor Management System (VMS) Market Overview

Vendor Management Systems (VMS) are software platforms designed to manage vendor relationships, procurement processes, supplier performance, compliance requirements, and workforce suppliers through centralized digital environments. The market includes cloud-based VMS platforms, on-premise systems, supplier information management tools, procurement automation solutions, contract management systems, and vendor risk management software. VMS solutions are widely utilized across manufacturing, healthcare, retail, IT & telecommunications, financial services, government, and logistics sectors. The market is shifting from manual supplier management processes toward AI-enabled, data-driven, and fully integrated vendor management ecosystems.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in artificial intelligence, predictive analytics, robotic process automation (RPA), and cloud-based procurement platforms is transforming vendor management operations. Advanced technologies are enabling automated supplier evaluations, performance monitoring, and real-time procurement intelligence.Market Implications

Companies investing in AI-powered supplier analytics, workflow automation, and integrated procurement platforms are expected to strengthen market leadership.2. Compliance and Risk Repricing

Supplier compliance requirements, ESG reporting obligations, cybersecurity standards, and data protection regulations are influencing vendor management strategies. Organizations are increasingly prioritizing supplier transparency and third-party risk mitigation.Market Implications

Firms offering compliant, secure, and audit-ready vendor management solutions are likely to gain stronger enterprise adoption.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as enterprise software vendors, procurement technology providers, ERP companies, and supply chain management firms expand their capabilities. Integration with ERP, procurement, and workforce management systems is reshaping value-chain structures.Market Implications

Companies focusing on end-to-end supplier lifecycle management and platform integration may gain stronger competitive advantages.4. Capital and Capacity Scaling

Rising investments in digital transformation, procurement modernization, cloud infrastructure, and supplier management technologies are supporting market growth. Organizations are increasing spending on vendor governance and supply chain resilience initiatives.Market Implications

Providers scaling cloud-based and AI-enabled VMS capabilities are expected to capture future opportunities.Market Segmentation Analysis

By Deployment Type

1. Cloud-Based Vendor Management Systems

This remains the largest segment due to scalability, flexibility, and lower implementation costs.2. On-Premise Vendor Management Systems

Preferred by organizations requiring extensive customization and data control.By Solution Type

1. Supplier Information Management

Widely utilized for centralized vendor data management.2. Contract Management Solutions

Strong demand driven by procurement governance requirements.3. Vendor Performance Management

Used for supplier evaluation and operational optimization.4. Vendor Risk Management Solutions

Growing demand due to compliance and cybersecurity concerns.5. AI-Powered Vendor Analytics & Risk Management Solutions

Fastest-growing segment due to predictive insights and automation capabilities.By Enterprise Size

1. Large Enterprises

Largest segment due to extensive supplier networks and procurement complexity.2. Small & Medium Enterprises (SMEs)

Growing adoption driven by cloud-based affordability and operational efficiency benefits.By End User

1. Manufacturing

Largest contributor due to complex supplier ecosystems and global sourcing activities.2. Healthcare

Strong demand for supplier compliance and procurement management.3. Retail & E-Commerce

Growing utilization for supplier coordination and inventory support.4. IT & Telecommunications

Increasing adoption for service provider and contractor management.5. BFSI & Government

Utilized for vendor governance and regulatory compliance management.Regional Market Dynamics

North America

North America dominates the global VMS market due to advanced enterprise software adoption, strong procurement digitization, and mature cloud infrastructure.Europe

Europe remains a major market supported by supplier governance requirements, ESG compliance initiatives, and digital transformation programs.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rapid industrialization, expanding enterprise software adoption, and growing supply chain complexity.Latin America

Latin America is gradually expanding due to increasing procurement modernization and business process automation.Middle East & Africa

The region is witnessing growing adoption driven by digital transformation initiatives and enterprise technology investments.Competitive Landscape

The Global Vendor Management System (VMS) Market is highly competitive with enterprise software providers, procurement technology companies, and cloud platform vendors expanding globally.Key Companies Operating in the Market Include:

- SAP SE

- Oracle Corporation

- Workday Inc.

- Beeline Inc.

- Coupa Software Inc.

- Jaggaer

- GEP Worldwide

- Corcentric LLC

- IBM Corporation

- ADP LLC

Strategic Outlook

The future of the VMS market will be shaped by AI-driven supplier intelligence, predictive risk analytics, automated procurement workflows, and integrated supply chain visibility platforms. Advanced analytics, ESG monitoring capabilities, and intelligent vendor performance management systems will significantly improve operational efficiency and supplier collaboration. The rise of digital procurement, supplier risk management, and cloud-native enterprise platforms is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Vendor Management System (VMS) Market remains a critical segment within enterprise software, procurement technology, and supply chain management ecosystems. Rising demand for supplier transparency, procurement automation, and third-party risk management continues driving long-term market growth. Companies capable of delivering scalable, intelligent, secure, and integrated vendor management ecosystems will be best positioned to capture future opportunities. The convergence of AI, cloud computing, procurement automation, and supplier intelligence is expected to redefine the future of global vendor management operations.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Vendor Management System (VMS) Market Snapshot (2026???2033)

- 1.2 Market Size & Growth Overview

- 1.3 Key Market Highlights

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Performance Summary

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Market Introduction & Overview

- 2.1 Definition of Vendor Management System (VMS)

- 2.2 Scope of the Global VMS Market

- 2.3 Evolution of Vendor & Supplier Management Technologies

- 2.4 Vendor Management Value Chain Analysis

- 2.5 Regulatory & Compliance Framework

- 2.6 Emerging Trends in Procurement Digitalization

- 2.7 Third-Party Risk Management & Supply Chain Visibility

- 3. Research Methodology

- 3.1 Primary Research Approach

- 3.2 Secondary Research Sources

- 3.3 Market Size Estimation Methodology

- 3.4 Forecasting Assumptions (2026???2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Market Drivers

- 4.1.1 Growing Demand for Supplier Visibility & Transparency

- 4.1.2 Increasing Procurement Digitalization Initiatives

- 4.1.3 Rising Third-Party Risk Management Requirements

- 4.1.4 Expansion of Global Supply Chain Networks

- 4.1.5 Adoption of AI, Analytics & Cloud-Based Procurement Platforms

- 4.2 Market Restraints

- 4.2.1 High Integration Complexity with Legacy Systems

- 4.2.2 Data Security & Privacy Concerns

- 4.2.3 Implementation Costs for Large-Scale Deployments

- 4.3 Market Opportunities

- 4.3.1 AI-Powered Supplier Intelligence Platforms

- 4.3.2 Expansion of ESG & Supplier Compliance Monitoring

- 4.3.3 Growth of Cloud-Native Procurement Ecosystems

- 4.3.4 Increasing Adoption Among SMEs

- 4.4 Market Challenges

- 4.4.1 Managing Complex Global Supplier Networks

- 4.4.2 Ensuring Real-Time Vendor Data Accuracy

- 4.4.3 Balancing Automation with Procurement Governance

- 4.1 Market Drivers

- 5. Global Vendor Management System (VMS) Market Size & Forecast (USD Billion), 2026???2033

- 5.1 Market Revenue Analysis

- 5.2 CAGR Analysis

- 5.3 Demand-Supply Trends

- 5.4 Pricing Analysis

- 5.5 Investment Trends

- 5.6 Future Market Outlook

- 6. Market Segmentation Analysis (USD Billion), 2026???2033

- 6.1 By Deployment Type

- 6.1.1 Cloud-Based Vendor Management Systems (Largest Segment)

- 6.1.2 On-Premise Vendor Management Systems

- 6.2 By Solution Type

- 6.2.1 Supplier Information Management

- 6.2.2 Contract Management Solutions

- 6.2.3 Vendor Performance Management

- 6.2.4 Vendor Risk Management Solutions

- 6.2.5 AI-Powered Vendor Analytics & Risk Management Solutions (Fastest-Growing Segment)

- 6.3 By Enterprise Size

- 6.3.1 Large Enterprises (Largest Segment)

- 6.3.2 Small & Medium Enterprises (SMEs)

- 6.4 By End User

- 6.4.1 Manufacturing (Largest Segment)

- 6.4.2 Healthcare

- 6.4.3 Retail & E-Commerce

- 6.4.4 IT & Telecommunications

- 6.4.5 BFSI & Government

- 6.1 By Deployment Type

- 7. Regional Market Analysis

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Competitive Benchmarking

- 8.3 Strategic Developments

- 8.4 AI Innovation & Procurement Automation Strategies

- 8.5 Partnerships, Acquisitions & Expansion Analysis

- 9. Company Profiles

- 9.1 SAP SE

- 9.2 Oracle Corporation

- 9.3 Workday Inc.

- 9.4 Beeline Inc.

- 9.5 Coupa Software Inc.

- 9.6 Jaggaer

- 9.7 GEP Worldwide

- 9.8 Corcentric LLC

- 9.9 IBM Corporation

- 9.10 ADP LLC

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Vendor Management Demand Forecast Model

- 10.2 Supplier Risk Intelligence Assessment

- 10.3 Procurement Automation Opportunity Tracker

- 10.4 Supply Chain Visibility & Compliance Analysis

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of AI-Driven Supplier Intelligence Solutions

- 11.2 Investment in Cloud-Based Procurement Platforms

- 11.3 Growth Opportunities in Vendor Risk Management

- 11.4 Strengthening Supply Chain Visibility & Compliance Capabilities

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Market Research

- 14. Disclaimer

Competitive Landscape

Global Vendor Management System (VMS) Market Competitive Intensity & Market Structure Overview

The global Vendor Management System (VMS) market is highly competitive and moderately consolidated, with leading enterprise software providers, procurement technology firms, workforce management specialists, and cloud-based platform vendors competing for market share. Competitive intensity is driven by platform functionality, integration capabilities, AI-powered analytics, supplier risk management features, scalability, regulatory compliance support, and user experience.

Market participants are increasingly investing in artificial intelligence, predictive analytics, procurement automation, supplier intelligence, and cloud-native architectures to strengthen their competitive positioning. As organizations seek greater visibility across complex supplier networks and third-party relationships, competition is intensifying among vendors offering comprehensive and data-driven vendor management solutions.

The market structure is evolving from standalone supplier management tools toward integrated enterprise ecosystems that connect procurement, contract management, risk monitoring, workforce management, and supply chain operations through centralized digital platforms. This transformation is creating opportunities for both established software providers and emerging procurement technology innovators.

Global Vendor Management System (VMS) Market Competitive Intensity & Market Structure Current Scenario

Leading Global Vendor Management System (VMS) Companies

SAP SE: A leading enterprise software provider offering integrated supplier management, procurement automation, and supply chain solutions through its SAP Ariba platform.

Oracle Corporation: Major provider of cloud-based procurement, supplier management, and vendor risk management solutions integrated within its enterprise software ecosystem.

Workday Inc.: Prominent provider of workforce and vendor management solutions with advanced analytics, automation, and cloud-native platform capabilities.

Beeline Inc.: Specialized VMS provider focused on contingent workforce management, supplier engagement, and vendor performance optimization.

Coupa Software Inc.: Leading business spend management company offering procurement, supplier collaboration, contract management, and risk intelligence solutions.

Jaggaer: Global procurement technology provider delivering end-to-end supplier lifecycle management, sourcing, and procurement automation platforms.

GEP Worldwide: Provider of procurement and supply chain software solutions featuring AI-driven supplier management and spend analytics capabilities.

Corcentric LLC: Enterprise procurement and financial process automation company offering vendor management, sourcing, and supplier collaboration solutions.

IBM Corporation: Technology leader delivering AI-powered procurement intelligence, supplier risk analytics, and digital transformation solutions for enterprise clients.

ADP LLC: Workforce and vendor management solutions provider supporting contingent labor management, compliance tracking, and supplier administration functions.

Key Competitive Intensity & Market Structure Drivers

The increasing complexity of global supply chains and third-party ecosystems is driving demand for advanced vendor visibility, supplier intelligence, and risk management capabilities.

Artificial intelligence, machine learning, and predictive analytics are becoming major competitive differentiators by enabling automated supplier evaluation, risk forecasting, and performance optimization.

Growing regulatory requirements related to supplier compliance, ESG reporting, cybersecurity governance, and data privacy are encouraging organizations to adopt more sophisticated VMS platforms.

Integration with ERP systems, procurement software, supply chain platforms, and workforce management applications is becoming essential for achieving operational efficiency and competitive differentiation.

Cloud-based deployment models are accelerating market adoption by offering scalability, lower implementation costs, continuous updates, and improved accessibility across global operations.

Strategic Implications of Competitive Intensity & Market Structure

Companies investing in AI-powered supplier intelligence, automated procurement workflows, and predictive risk management capabilities are expected to gain significant competitive advantages in the evolving VMS market.

Enterprise software providers with extensive ecosystem integration capabilities are likely to strengthen customer retention and expand platform adoption across procurement and supply chain functions.

Strategic partnerships between procurement technology providers, ERP vendors, and supply chain management companies are accelerating innovation and enhancing end-to-end vendor management capabilities.

Organizations offering comprehensive supplier lifecycle management solutions that combine procurement, compliance, performance tracking, and risk management are expected to achieve stronger enterprise adoption.

The growing importance of ESG monitoring, sustainability reporting, and supplier governance is creating new opportunities for differentiated vendor management solutions and value-added services.

Global Vendor Management System (VMS) Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global VMS market is expected to become increasingly intelligence-driven as organizations prioritize supplier resilience, procurement optimization, and third-party risk management. AI-powered decision support systems and predictive supplier analytics will play a central role in future market competition.

Market participants are expected to increase investments in automation, cloud-native platforms, ESG compliance tools, and real-time supplier monitoring technologies to enhance operational efficiency and strategic value creation.

North America is expected to remain a leading market due to advanced enterprise software adoption and procurement digitization, while Asia-Pacific is projected to experience the fastest growth driven by expanding industrial activity, supply chain modernization, and digital transformation initiatives.

Over the forecast period, companies that successfully combine technological innovation, platform integration, regulatory compliance, supplier intelligence, and customer-centric service delivery will be best positioned to strengthen their leadership within the evolving global Vendor Management System (VMS) market.

Value Chain

Global Vendor Management System (VMS) Market Value Chain & Supply Chain Evolution Overview

The Global Vendor Management System (VMS) Market is undergoing significant transformation driven by procurement digitization, supplier risk management requirements, cloud computing adoption, and increasing demand for end-to-end supply chain visibility. The market???s value chain is characterized by a highly integrated digital ecosystem connecting enterprise software providers, cloud infrastructure vendors, procurement technology companies, analytics platforms, compliance solution providers, system integrators, and enterprise customers. This interconnected framework is reshaping how organizations manage supplier relationships, procurement processes, vendor performance, and regulatory compliance.

A defining feature of the value chain is the convergence of traditional supplier management functions with artificial intelligence, predictive analytics, robotic process automation (RPA), and cloud-native platforms. Modern VMS solutions are evolving beyond vendor record management to provide intelligent supplier insights, automated workflows, risk monitoring, contract lifecycle management, and real-time performance evaluation capabilities.

Supply chain complexity continues to increase as organizations manage global supplier networks, third-party compliance requirements, cybersecurity risks, ESG reporting obligations, and procurement governance standards. Companies must coordinate across software development, cloud infrastructure, data integration, compliance monitoring, procurement operations, and supplier engagement processes while ensuring operational efficiency and transparency.

Industry participants are investing heavily in AI-powered supplier analytics, cloud-based procurement platforms, workflow automation technologies, and integrated enterprise ecosystems to improve supplier collaboration and business resilience. The value chain is evolving into a highly connected, data-driven, and intelligence-enabled ecosystem focused on supplier optimization and strategic procurement management.

Global Vendor Management System (VMS) Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Technology Infrastructure & Data Sources: Cloud computing platforms, enterprise databases, supplier information repositories, cybersecurity systems, API frameworks, and business intelligence platforms.

- VMS Platform Development: Vendor management software development, procurement automation systems, contract management solutions, supplier information management tools, and vendor risk management platforms.

- AI & Analytics Integration: Predictive supplier analytics, AI-driven risk assessment, performance monitoring systems, workflow automation tools, and procurement intelligence engines.

- Compliance & Governance Management: Supplier compliance monitoring, ESG tracking systems, regulatory reporting tools, cybersecurity assessment platforms, and audit management solutions.

- Deployment & Integration Services: Cloud deployment, ERP integration, procurement system connectivity, workforce management integration, and enterprise software implementation services.

- End-User Operations: Procurement teams, supply chain departments, vendor governance offices, contract management teams, finance departments, and enterprise leadership functions.

Company-to-Stage Mapping

- Technology Infrastructure & Data Sources: Cloud infrastructure providers, cybersecurity companies, enterprise data management vendors, and analytics platform providers.

- VMS Platform Development: SAP SE, Oracle Corporation, Workday Inc., Beeline Inc., Coupa Software Inc., Jaggaer, Corcentric LLC.

- AI & Analytics Integration: IBM Corporation, SAP SE, Oracle Corporation, GEP Worldwide, AI and procurement analytics solution providers.

- Compliance & Governance Management: Vendor risk management providers, ESG compliance solution vendors, cybersecurity assessment firms, and governance technology companies.

- Deployment & Integration Services: System integrators, enterprise software consultants, managed service providers, and cloud deployment specialists.

- End-User Operations: Manufacturing enterprises, healthcare organizations, retailers, BFSI institutions, government agencies, and IT & telecommunications companies.

Key Value Chain & Supply Chain Evolution Signals in Global Vendor Management System (VMS) Market

- Expansion of AI-Driven Supplier Intelligence:

AI-powered analytics are improving supplier evaluation, risk prediction, procurement optimization, and strategic sourcing decisions. - Growth of Automated Procurement Workflows:

Organizations are increasingly deploying automation technologies to streamline vendor onboarding, approvals, contract management, and purchasing processes. - Increasing Focus on Third-Party Risk Management:

Vendor risk monitoring is becoming a critical component of enterprise governance and operational resilience strategies. - Integration with Enterprise Software Ecosystems:

VMS platforms are increasingly integrated with ERP, SCM, finance, HR, and procurement systems to enable end-to-end operational visibility. - Growing Importance of ESG & Supplier Compliance Monitoring:

Organizations are expanding supplier governance programs to address sustainability, regulatory compliance, and ethical sourcing requirements. - Rise of Cloud-Native Vendor Management Platforms:

Cloud deployment models are improving scalability, accessibility, implementation speed, and operational flexibility.

Strategic Implications of Value Chain & Supply Chain Evolution

- Investment in AI-Powered Risk & Performance Analytics:

Advanced analytics capabilities enable proactive supplier management and stronger procurement decision-making. - Expansion of Integrated Procurement Ecosystems:

Seamless connectivity between procurement, ERP, and supplier management platforms improves efficiency and governance. - Strengthening Supplier Compliance Infrastructure:

Automated compliance monitoring supports regulatory adherence and reduces operational risk exposure. - Enhancement of Vendor Lifecycle Management:

End-to-end supplier lifecycle visibility improves collaboration, accountability, and supplier performance outcomes. - Development of ESG-Focused Supplier Governance Models:

Sustainability monitoring is becoming an essential element of modern vendor management strategies. - Optimization of Cloud-Based Deployment Strategies:

Cloud-native architectures enhance scalability, cost efficiency, and global accessibility for enterprise customers.

Global Vendor Management System (VMS) Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the VMS value chain is expected to evolve into a highly intelligent, automated, and interconnected supplier management ecosystem powered by AI, cloud computing, predictive analytics, and real-time procurement intelligence.

Key Future Developments Include:

- Expansion of AI-driven supplier intelligence and predictive risk management systems.

- Increased adoption of automated procurement and contract lifecycle management platforms.

- Growth of cloud-native vendor management ecosystems across global enterprises.

- Advancement of ESG monitoring and supplier sustainability analytics capabilities.

- Integration of real-time supplier performance dashboards and procurement intelligence tools.

- Strengthening of cybersecurity and third-party risk assessment frameworks within vendor ecosystems.

As the market evolves, competitive advantage will increasingly depend on the ability to combine supplier intelligence, compliance automation, procurement efficiency, and enterprise integration capabilities. Organizations capable of delivering secure, scalable, and data-driven vendor management solutions will be best positioned to capture future growth opportunities.

Companies that successfully integrate AI-powered analytics, cloud-based procurement platforms, automated governance tools, and comprehensive supplier lifecycle management capabilities will achieve stronger customer adoption, improved operational efficiency, and long-term leadership in the Global Vendor Management System (VMS) Market.

Investment Activity

Global Vendor Management System (VMS) Market Investment & Funding Dynamics Overview

The Global Vendor Management System (VMS) Market is witnessing significant investment activity driven by accelerating procurement digitization, growing third-party risk management requirements, increasing demand for supplier transparency, and expanding adoption of cloud-based enterprise software solutions. Enterprise software vendors, procurement technology providers, ERP companies, supply chain management firms, and private equity investors are actively investing in AI-powered vendor analytics, cloud-native VMS platforms, supplier intelligence solutions, procurement automation technologies, and integrated risk management systems.

Investment momentum is strengthening as organizations seek to improve vendor governance, streamline procurement workflows, enhance supplier collaboration, and mitigate operational risks across complex global supply chains. Capital deployment is increasingly focused on automated supplier onboarding systems, predictive risk analytics, digital contract management platforms, ESG monitoring tools, and real-time supplier performance management solutions.

Additionally, rising investments in artificial intelligence, machine learning, robotic process automation (RPA), cloud infrastructure, and advanced procurement analytics are creating long-term growth opportunities across the global VMS ecosystem.

Global Vendor Management System (VMS) Market Investment & Funding Dynamics Current Scenario

Currently, the VMS market is experiencing robust funding activity as enterprises accelerate digital transformation initiatives and modernize procurement operations. Leading market participants are investing heavily in AI-driven supplier intelligence platforms, cloud-based procurement ecosystems, vendor risk assessment technologies, and automated compliance management solutions.

The market is attracting substantial venture capital, private equity, and strategic corporate investments into procurement software providers, supplier management technology firms, contract lifecycle management platforms, and supply chain visibility solution developers. Investors are increasingly targeting companies capable of improving procurement efficiency, supplier resilience, and regulatory compliance.

Furthermore, the industry is witnessing active mergers, acquisitions, strategic partnerships, and platform integrations as software providers expand functionality, strengthen analytics capabilities, and create end-to-end vendor management ecosystems.

Key Investment & Funding Dynamics Signals in Global Vendor Management System (VMS) Market

- Growing demand for AI-powered vendor analytics and predictive supplier intelligence is accelerating technology-focused investments.

- Expansion of digital procurement and automated sourcing workflows is increasing capital allocation across enterprise software platforms.

- Rising focus on third-party risk management and supplier compliance monitoring is strengthening investment activity.

- Strategic investments in cloud-based VMS solutions and integrated procurement ecosystems are supporting digital transformation initiatives.

- Increasing emphasis on ESG compliance, supplier transparency, and governance standards is influencing long-term funding priorities.

- Partnerships between ERP vendors, procurement technology providers, and supply chain software companies are improving platform interoperability and scalability.

- Growing demand for real-time supplier performance tracking and contract lifecycle automation is driving innovation-focused investments.

Strategic Implications of Investment & Funding Dynamics in Global Vendor Management System (VMS) Market

- Continuous investment in AI-driven procurement intelligence and vendor risk management technologies is becoming essential for competitive differentiation.

- Capital allocation toward cloud infrastructure, workflow automation, and advanced analytics capabilities will strengthen long-term market positioning.

- Companies offering integrated, scalable, and data-driven vendor management platforms are expected to gain stronger enterprise adoption.

- Strategic acquisitions and technology partnerships will accelerate product innovation, ecosystem expansion, and service diversification.

- Investments in supplier compliance management, ESG reporting tools, and intelligent procurement solutions will remain major growth priorities.

- Compliance with data privacy regulations, supplier governance standards, and procurement compliance requirements will continue shaping investment strategies.

- Organizations developing end-to-end supplier lifecycle management platforms and predictive risk intelligence systems are expected to capture substantial future opportunities.

Global Vendor Management System (VMS) Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Vendor Management System (VMS) Market is expected to maintain strong investment growth driven by increasing procurement automation, expanding supplier networks, rising regulatory scrutiny, and growing demand for supply chain resilience.

Future capital deployment will increasingly focus on AI-powered procurement intelligence, autonomous vendor management workflows, predictive supplier risk analytics, ESG-focused supplier monitoring systems, and fully integrated digital procurement ecosystems.

As enterprises continue to prioritize operational efficiency and supplier visibility, investment activity is expected to expand across cloud-native platforms, intelligent automation technologies, and next-generation supplier collaboration solutions.

In conclusion, the Global Vendor Management System (VMS) Market represents a high-growth enterprise software investment landscape where artificial intelligence, cloud computing, procurement automation, supplier intelligence, and risk management innovation will define future funding priorities, competitive strategies, and long-term market expansion.

Technology & Innovation

Global Vendor Management System (VMS) Market Technology & Innovation Landscape Overview

The global Vendor Management System (VMS) market is undergoing significant technological transformation driven by advancements in artificial intelligence (AI), cloud computing, predictive analytics, robotic process automation (RPA), supplier intelligence platforms, and integrated procurement technologies. Organizations are increasingly adopting digital vendor management solutions to enhance supplier visibility, streamline procurement operations, improve compliance management, and strengthen third-party risk oversight across complex supply chains.

Modern VMS platforms integrate AI-powered supplier analytics, automated vendor onboarding tools, contract lifecycle management systems, risk assessment engines, and real-time performance monitoring dashboards to optimize vendor relationships and procurement efficiency. These technologies are helping enterprises reduce procurement costs, improve supplier collaboration, and strengthen operational resilience.

The market is also witnessing growing adoption of cloud-native VMS platforms, ESG monitoring solutions, intelligent workflow automation, and data-driven supplier performance management systems that are transforming traditional vendor management practices into intelligent and proactive business functions.

Global Vendor Management System (VMS) Market Technology & Innovation Current Scenario

Current innovation in the VMS market is focused on supplier intelligence, procurement automation, and predictive vendor risk management. Traditional manual supplier management processes are increasingly being replaced by centralized digital platforms capable of providing real-time insights and automated decision support.

AI-powered supplier analytics platforms are gaining widespread adoption as organizations seek deeper visibility into supplier performance, financial stability, operational risks, and compliance status.

Automated procurement workflows are improving efficiency by reducing manual intervention in vendor onboarding, contract approvals, invoice processing, and supplier evaluations.

Cloud-based VMS solutions continue to dominate implementation strategies due to their scalability, lower deployment costs, and seamless integration with enterprise applications.

Predictive analytics technologies are increasingly enabling organizations to identify potential supplier disruptions, compliance risks, and operational bottlenecks before they impact business operations.

Integration with ERP, procurement, supply chain, and workforce management systems is enhancing enterprise-wide visibility and vendor governance capabilities.

Key Technology & Innovation Trends in Global Vendor Management System (VMS) Market

- AI-Powered Supplier Intelligence: Enabling advanced supplier evaluation, performance analysis, and risk assessment.

- Predictive Vendor Risk Analytics: Identifying potential disruptions and compliance issues before they occur.

- Cloud-Native VMS Platforms: Supporting scalable, flexible, and globally accessible vendor management operations.

- Automated Procurement Workflows: Streamlining supplier onboarding, approvals, and procurement processes.

- Contract Lifecycle Management Systems: Improving contract visibility, compliance, and governance.

- ESG Monitoring & Supplier Sustainability Analytics: Supporting responsible sourcing and regulatory compliance.

- Robotic Process Automation (RPA): Reducing manual administrative tasks and operational costs.

- Integrated Supplier Performance Dashboards: Providing real-time operational and performance insights.

- Third-Party Risk Management Platforms: Strengthening cybersecurity, compliance, and operational risk controls.

- Advanced API-Based Integrations: Connecting VMS platforms with ERP, procurement, and supply chain ecosystems.

Strategic Implications of Technology & Innovation

Technological innovation is reshaping competitive dynamics in the VMS market by shifting vendor management from administrative procurement functions toward intelligent, predictive, and data-driven supplier ecosystem management.

Organizations investing in AI-powered analytics, procurement automation, and integrated supplier intelligence platforms are achieving stronger supplier collaboration, improved compliance management, and enhanced operational efficiency.

The convergence of AI, predictive analytics, and cloud technologies is enabling enterprises to make faster procurement decisions while proactively managing supplier risks and performance challenges.

Advanced automation capabilities are reducing procurement cycle times, minimizing human error, and improving transparency across vendor management operations.

However, integration complexity, data quality challenges, cybersecurity risks, and evolving regulatory requirements remain key challenges for large-scale VMS deployments.

Global Vendor Management System (VMS) Market Technology & Innovation Forward Outlook

The future of the VMS market is expected to evolve toward fully autonomous, AI-driven, and predictive supplier management ecosystems capable of continuously optimizing procurement, compliance, and vendor performance outcomes.

Emerging innovations include generative AI procurement assistants, autonomous supplier risk monitoring systems, digital supplier twins, intelligent contract analytics, and real-time ESG compliance tracking platforms.

Advanced machine learning models are expected to improve supplier forecasting, procurement planning, and risk mitigation capabilities while supporting strategic sourcing initiatives.

Cloud-based ecosystems will further strengthen collaboration between buyers, suppliers, procurement teams, and compliance stakeholders through unified digital platforms.

Overall, the global Vendor Management System market is evolving toward a highly connected ecosystem where AI, cloud computing, automation, predictive analytics, and supplier intelligence collectively redefine procurement efficiency, supplier governance, and enterprise supply chain resilience.

Market Risk

Vendor Management System (VMS) Market Risk Factors & Disruption Threats Overview

The global Vendor Management System (VMS) market operates within a dynamic and increasingly complex business environment shaped by digital procurement transformation, third-party risk management requirements, evolving regulatory frameworks, and supply chain uncertainties. While demand for vendor management solutions continues to grow as organizations seek greater supplier visibility and operational efficiency, the market remains exposed to technological, cybersecurity, compliance, and integration-related risks.

Vendor Management Systems have become essential for managing supplier relationships, procurement workflows, contract administration, compliance monitoring, and vendor performance evaluation. As organizations expand global supplier networks and rely more heavily on third-party service providers, the need for centralized vendor governance platforms continues to increase.

However, growing dependence on digital procurement ecosystems, cloud-based infrastructure, and interconnected enterprise systems creates new operational challenges. Data security concerns, regulatory obligations, and increasing supplier complexity are reshaping risk management priorities across the market.

Additionally, economic uncertainty, geopolitical disruptions, and supply chain volatility continue to influence procurement strategies and vendor management investments, creating both opportunities and challenges for VMS providers.

Vendor Management System (VMS) Market Risk Factors & Disruption Threats Current Scenario

The current VMS market is characterized by rapid cloud adoption, growing AI integration, and increasing focus on supplier risk management. Organizations are prioritizing vendor transparency, compliance monitoring, and procurement automation to improve operational resilience and reduce third-party exposure.

One of the most significant risks facing the market is cybersecurity vulnerability. Vendor management platforms often store sensitive supplier information, contractual data, financial records, and procurement intelligence. As cyberattacks become more sophisticated, organizations face growing pressure to secure vendor ecosystems and protect critical business information.

Regulatory complexity continues to increase across global markets. Data privacy regulations, ESG reporting requirements, anti-corruption laws, supplier due diligence obligations, and procurement governance standards require organizations to maintain comprehensive compliance monitoring capabilities. Failure to meet these requirements can result in legal penalties, reputational damage, and operational disruption.

Integration challenges also remain prevalent. Many enterprises operate multiple procurement, ERP, supply chain, and financial management systems. Ensuring seamless interoperability between VMS platforms and existing enterprise technologies can be resource-intensive and may delay implementation timelines.

Furthermore, supply chain disruptions and geopolitical instability are increasing the importance of vendor risk assessment. Organizations are placing greater emphasis on supplier diversification, business continuity planning, and real-time visibility into third-party risks.

Key Risk Factors & Disruption Threats Signals in the VMS Market

- Cybersecurity and Data Breach Risks: Vendor management platforms contain sensitive procurement, supplier, and financial information that may be targeted by cybercriminals.

- Regulatory Compliance Complexity: Evolving data privacy laws, ESG reporting requirements, supplier due diligence regulations, and procurement governance standards increase compliance obligations.

- Third-Party Risk Exposure: Dependence on suppliers, contractors, and service providers can create operational, financial, reputational, and compliance risks.

- Supply Chain Disruptions: Geopolitical tensions, logistics bottlenecks, trade restrictions, and supplier failures can impact procurement continuity and vendor performance.

- Technology Integration Challenges: Complex integration with ERP systems, procurement platforms, workforce management solutions, and legacy infrastructure may delay adoption.

- Data Quality and Vendor Information Accuracy: Incomplete, outdated, or inconsistent supplier data can reduce decision-making effectiveness and compliance accuracy.

- AI Governance and Transparency Concerns: Increased use of AI-driven supplier analytics may introduce risks related to algorithm transparency, bias, and regulatory oversight.

- Vendor Concentration Risk: Overreliance on a limited number of suppliers can increase exposure to disruptions and operational vulnerabilities.

- Economic and Budgetary Constraints: Economic uncertainty may lead organizations to delay enterprise software investments and procurement modernization initiatives.

- Competitive Market Pressure: Rapid innovation among software providers, procurement technology firms, and ERP vendors may intensify pricing competition and customer retention challenges.

Strategic Implications of Risk Factors & Disruption Threats in the VMS Market

The evolving risk landscape is encouraging organizations to move beyond basic supplier management and adopt comprehensive vendor governance frameworks. Enterprises are increasingly integrating vendor risk management, compliance monitoring, procurement automation, and performance analytics into unified digital platforms.

Cybersecurity investments are becoming a strategic necessity for VMS providers and enterprise users alike. Advanced encryption, identity management systems, access controls, and continuous monitoring capabilities are being implemented to strengthen platform security and maintain stakeholder trust.

Artificial intelligence and predictive analytics are emerging as important tools for identifying supplier risks, monitoring performance trends, and improving procurement decision-making. However, organizations must ensure transparency and accountability in AI-driven processes to satisfy regulatory and governance requirements.

Strategic supplier diversification and enhanced visibility into supplier ecosystems are becoming critical priorities. Organizations are increasingly leveraging VMS platforms to identify potential disruptions, monitor compliance status, and improve supply chain resilience.

In addition, cloud-based deployment models continue to accelerate due to scalability, flexibility, and lower operational costs. Vendors that offer highly secure, integrated, and user-friendly cloud solutions are expected to gain stronger market adoption.

Vendor Management System (VMS) Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead, the VMS market is expected to experience sustained growth as organizations continue investing in digital procurement, supplier intelligence, and third-party risk management capabilities. However, market participants will need to navigate increasing regulatory scrutiny, cybersecurity challenges, and evolving supplier ecosystems.

AI-powered vendor analytics, automated compliance monitoring, and predictive supplier risk assessment tools are expected to become standard features within modern VMS platforms. These technologies will improve operational efficiency but also require stronger governance frameworks and transparency measures.

Regulatory requirements related to ESG reporting, supply chain transparency, data privacy, and third-party accountability are likely to expand globally. Organizations that proactively adapt to these requirements will be better positioned to maintain compliance and strengthen stakeholder confidence.

Supply chain resilience will remain a major strategic priority as businesses seek to reduce exposure to geopolitical instability, supplier disruptions, and market volatility. Real-time vendor intelligence and risk monitoring capabilities will become increasingly valuable in supporting continuity planning.

Overall, the global Vendor Management System market is expected to remain highly strategic within procurement and enterprise software ecosystems. Companies that prioritize cybersecurity, supplier transparency, AI-driven insights, regulatory compliance, and platform integration will be best positioned to mitigate disruption risks and capitalize on long-term growth opportunities.

Regulatory Landscape

Global Vendor Management System (VMS) Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Vendor Management System (VMS) Market is increasingly shaped by supplier compliance requirements, third-party risk management regulations, procurement governance standards, data privacy laws, and corporate transparency mandates. As organizations become more reliant on global supplier networks and outsourced service providers, regulatory authorities and industry bodies are placing greater emphasis on vendor accountability, operational transparency, and compliance monitoring.

Vendor Management System providers and enterprise users must comply with a broad range of regulations covering supplier due diligence, contract governance, data security, labor compliance, cybersecurity requirements, anti-corruption policies, and environmental, social, and governance (ESG) reporting obligations. These regulations are driving demand for centralized platforms capable of managing vendor information, monitoring supplier performance, and ensuring regulatory compliance across complex procurement ecosystems.

The rapid adoption of cloud-based procurement platforms, AI-driven supplier analytics, and digital supply chain technologies is also encouraging the development of modern governance frameworks designed to improve vendor visibility, risk assessment, and compliance automation.

Global Vendor Management System (VMS) Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for VMS solutions combines procurement governance requirements, supplier risk management standards, corporate compliance mandates, and digital data protection regulations. Organizations are increasingly required to maintain detailed records of vendor relationships, contract obligations, supplier certifications, and third-party risk assessments.

In North America and Europe, regulations governing data privacy, cybersecurity, anti-bribery compliance, and supply chain transparency are significantly influencing vendor management practices. Frameworks such as GDPR, CCPA, anti-corruption laws, and vendor risk management guidelines are encouraging enterprises to adopt automated compliance monitoring solutions.

Supplier due diligence requirements are becoming more stringent across industries, particularly in sectors such as healthcare, manufacturing, financial services, and government procurement. Organizations are expected to evaluate vendor reliability, financial stability, cybersecurity readiness, and regulatory compliance before establishing business relationships.

Asia-Pacific markets including China, India, Japan, South Korea, and Australia are strengthening procurement governance policies and digital transformation initiatives, encouraging broader adoption of cloud-based vendor management platforms to improve supplier oversight and operational efficiency.

At the same time, ESG reporting regulations and responsible sourcing requirements are increasing the importance of supplier sustainability monitoring and ethical procurement practices within vendor management strategies.

Key Regulatory & Policy Environment Signals in Global VMS Market

- Supplier Compliance Requirements: Organizations must ensure vendors comply with contractual, operational, legal, and industry-specific standards.

- Data Privacy & Protection Regulations: Vendor management platforms must comply with regulations governing the collection, storage, and processing of supplier and enterprise data.

- Third-Party Risk Management Standards: Enterprises are required to assess and monitor operational, financial, cybersecurity, and compliance risks associated with vendors.

- Procurement Governance Frameworks: Regulations promote transparency, accountability, and standardized procurement processes across supplier ecosystems.

- Cybersecurity & Information Security Compliance: Vendor evaluation increasingly includes security assessments and ongoing cyber risk monitoring.

- ESG & Responsible Sourcing Regulations: Organizations are expected to track supplier sustainability performance and ethical business practices.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging enterprises to invest heavily in automated compliance management, AI-powered vendor risk assessment tools, and integrated supplier governance platforms. Organizations are increasingly using VMS solutions to centralize vendor data, streamline audits, and improve regulatory reporting capabilities.

Third-party risk management requirements are accelerating demand for predictive analytics, supplier scoring systems, and continuous monitoring technologies that enable proactive identification of compliance vulnerabilities and operational risks.

Data protection and cybersecurity regulations are driving investment in secure cloud architectures, access control systems, encryption technologies, and vendor security assessment frameworks to safeguard sensitive enterprise and supplier information.

ESG reporting obligations are also encouraging organizations to expand supplier sustainability monitoring programs and integrate environmental and social performance metrics into procurement decision-making processes.

Companies capable of combining procurement automation, compliance management, supplier intelligence, and risk monitoring within unified VMS platforms are expected to achieve stronger competitive positioning and long-term customer retention.

Global Vendor Management System (VMS) Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global VMS market is expected to become increasingly digital, data-driven, and risk-focused. Governments and regulatory agencies are likely to expand supplier transparency requirements, strengthen third-party accountability standards, and introduce more comprehensive governance frameworks for procurement and supply chain operations.

Organizations will face increasing pressure to demonstrate vendor compliance, supply chain resilience, and ESG performance through automated reporting systems and real-time supplier monitoring capabilities. Regulatory authorities may also require more detailed documentation of vendor due diligence and ongoing risk management activities.

Artificial intelligence and automation technologies used within vendor management platforms are expected to face greater scrutiny regarding transparency, accountability, and decision-making governance. This may result in additional compliance standards for AI-driven supplier evaluation and risk assessment systems.

Cross-border harmonization of procurement governance standards, data protection regulations, and supplier compliance frameworks is expected to strengthen as global supply chains become increasingly interconnected and digitally managed.

Overall, regulatory and policy developments will remain a major driver of innovation and adoption within the VMS market. Organizations investing in secure, compliant, intelligent, and transparent vendor management ecosystems are expected to maintain a significant competitive advantage throughout the forecast period.