Global Internet of Things (IoT) in Food Market Report, Size, Share and Forecast 2026–2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

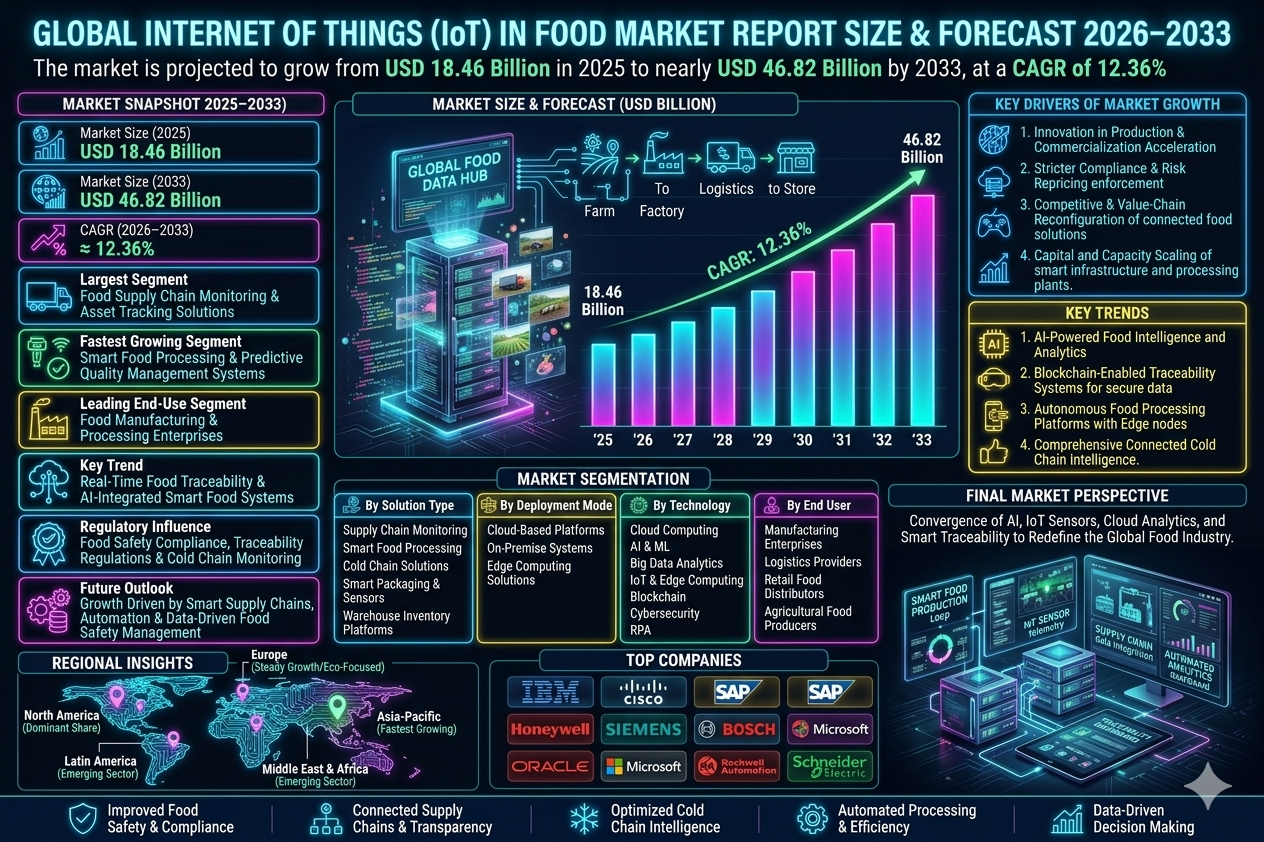

| Market Size (2025) | USD 18.46 Billion |

| Market Size (2033) | USD 46.82 Billion |

| CAGR (2026???2033) | 12.36% |

| Largest Segment | Food Supply Chain Monitoring & Asset Tracking Solutions |

| Fastest Growing Segment | Smart Food Processing & Predictive Quality Management Systems |

| Leading End-Use Segment | Food Manufacturing & Processing Enterprises |

| Key Trend | Real-Time Food Traceability & AI-Integrated Smart Food Systems |

| Regulatory Influence | Food Safety Compliance, Traceability Regulations & Cold Chain Monitoring Standards |

| Future Outlook | Growth Driven by Smart Supply Chains, Automation & Data-Driven Food Safety Management |

Global Internet of Things (IoT) in Food Market Size & Forecast

The Global Internet of Things (IoT) in Food Market is expected to witness strong expansion during the forecast period from 2026 to 2033. The market was valued at USD 18.46 billion in 2025 and is projected to reach approximately USD 46.82 billion by 2033, registering a CAGR of 12.36%. The market growth is primarily driven by increasing food safety concerns, rising demand for real-time supply chain visibility, expanding automation in food processing, and growing adoption of connected monitoring systems. IoT technologies are increasingly critical for food production optimization, cold chain management, quality assurance, predictive maintenance, and inventory control. Rising deployment of connected sensors, RFID systems, smart packaging, and AI-powered analytics is accelerating market growth. In addition, increasing digital transformation across food manufacturing and stricter regulatory requirements for traceability are supporting long-term market expansion.Global Internet of Things (IoT) in Food Market Overview

IoT in food refers to connected digital technologies that enable data collection, monitoring, automation, and analytics across food production, processing, storage, transportation, and retail operations. The market includes smart sensors, RFID-enabled tracking systems, connected cold chain monitoring devices, automated food processing systems, predictive maintenance platforms, and smart food inventory management solutions. IoT-enabled food systems are widely utilized across food manufacturing, processing plants, logistics operations, retail distribution, and agricultural food production environments. The market is shifting from manual monitoring systems toward real-time connected ecosystems, AI-integrated automation, cloud-based food analytics platforms, and end-to-end digital traceability frameworks.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in smart sensors, AI-powered analytics, blockchain-enabled traceability, and connected automation systems is accelerating digital transformation across food ecosystems. Advanced monitoring technologies are significantly improving food safety, operational efficiency, and predictive decision-making.Market Implications

Companies investing in integrated IoT ecosystems, real-time analytics, and automation platforms are expected to strengthen market leadership.2. Compliance and Risk Repricing

Food safety regulations, cold chain monitoring requirements, traceability mandates, and contamination prevention standards are influencing technology modernization. Regulatory agencies are increasingly enforcing digital compliance and transparent food monitoring frameworks.Market Implications

Firms offering compliant, traceable, and digitally secure food monitoring solutions are likely to gain stronger market trust.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as food technology providers, sensor manufacturers, cloud analytics companies, and industrial automation firms expand connected food solutions. Integrated digital supply chain ecosystems and data-driven decision frameworks are altering value-chain economics.Market Implications

Companies focusing on full-stack IoT integration and predictive food management systems may gain stronger margins.4. Capital and Capacity Scaling

Rising investment in smart processing facilities, connected logistics infrastructure, edge computing platforms, and cloud analytics systems is supporting market expansion. Food manufacturers are increasing digital modernization spending to improve resilience and efficiency.Market Implications

Operators scaling smart infrastructure and data analytics capabilities are expected to capture future opportunities.Market Segmentation Analysis

By Solution Type

1. Food Supply Chain Monitoring & Asset Tracking Solutions

This remains the largest segment due to widespread traceability and logistics optimization requirements.2. Smart Food Processing Systems

Fast-growing due to automation and predictive maintenance benefits.3. Cold Chain Monitoring Solutions

Strong demand driven by temperature-sensitive food transportation.4. Smart Packaging & Sensor Systems

Growing adoption for freshness tracking and contamination prevention.5. Inventory & Warehouse Monitoring Platforms

Used for operational efficiency and stock optimization.By Deployment Mode

1. Cloud-Based Platforms

Largest segment due to scalability and centralized analytics capabilities.2. On-Premise Systems

Widely used by large-scale food enterprises with internal infrastructure.3. Edge Computing Solutions

Fastest-growing due to real-time local processing efficiency.By End User

1. Food Manufacturing & Processing Enterprises

Largest segment due to large-scale automation requirements.2. Food Logistics & Cold Chain Providers

Strong demand for shipment visibility and temperature monitoring.3. Retail Food Distributors

Growing adoption for inventory and freshness management.4. Agricultural Food Producers

Used for farm-to-table digital monitoring applications.Regional Market Dynamics

North America

North America dominates the global IoT in food market due to advanced digital food infrastructure, strong regulatory compliance, and early IoT technology adoption.Europe

Europe remains a major market supported by stringent food safety standards and strong smart manufacturing investments.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rapid food industry digitalization, industrial automation growth, and expanding connected supply chain networks.Latin America

Latin America is gradually expanding due to food export modernization and digital logistics investments.Middle East & Africa

The region is witnessing emerging adoption driven by food security initiatives and supply chain digital transformation.Competitive Landscape

The Global Internet of Things (IoT) in Food Market is highly competitive with industrial automation providers, cloud technology firms, food tech innovators, and sensor manufacturers expanding globally.Key Companies Operating in the Market Include:

- IBM Corporation

- Cisco Systems

- SAP SE

- Honeywell International Inc.

- Siemens AG

- Bosch Connected Industry

- Oracle Corporation

- Microsoft Corporation

- Rockwell Automation

- Schneider Electric

Strategic Outlook

The future of the IoT in food market will be shaped by AI-powered food intelligence, blockchain traceability systems, autonomous food processing platforms, and edge-enabled real-time monitoring. Predictive analytics, automated contamination detection, and connected cold chain intelligence will significantly improve operational efficiency. The rise of smart food ecosystems, digital compliance frameworks, and connected food logistics is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Internet of Things (IoT) in Food Market remains a major segment within food technology and digital industrial ecosystems. Rising food safety requirements, connected automation adoption, and supply chain modernization continue driving long-term market growth. Companies capable of delivering scalable, secure, intelligent, and compliance-driven IoT food ecosystems will be best positioned to capture future opportunities. The convergence of AI, IoT sensors, cloud analytics, and smart traceability is expected to redefine the future of the global food industry.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Internet of Things (IoT) in Food Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of IoT in Food Market

- 2.2 Scope of the Study

- 2.3 Evolution of Smart Food Systems

- 2.4 Digital Food Supply Chain Ecosystem Analysis

- 2.5 Regulatory & Compliance Framework

- 2.6 Food Safety Digitization Trends

- 2.7 Industrial IoT Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Food Safety Concerns

- 4.1.2 Demand for Real-Time Traceability

- 4.1.3 Expansion of Smart Food Processing

- 4.1.4 Growth of Cold Chain Digitization

- 4.1.5 Increasing Automation in Food Manufacturing

- 4.2 Restraints

- 4.2.1 High Implementation Costs

- 4.2.2 Data Security & Privacy Risks

- 4.2.3 Integration Complexity with Legacy Systems

- 4.2.4 Limited Digital Skills in Small Enterprises

- 4.3 Opportunities

- 4.3.1 AI-Powered Food Intelligence Systems

- 4.3.2 Blockchain-Based Traceability Platforms

- 4.3.3 Edge Computing in Food Monitoring

- 4.3.4 Smart Packaging Innovations

- 4.4 Challenges

- 4.4.1 System Interoperability Issues

- 4.4.2 Cybersecurity Threats in Connected Systems

- 4.4.3 Scalability of IoT Infrastructure

- 4.4.4 Standardization Across Global Food Chains

- 4.1 Drivers

- 5. Global IoT in Food Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Technology Adoption Trends

- 5.5 Industry Demand Analysis

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Solution Type

- 6.1.1 Food Supply Chain Monitoring & Asset Tracking Solutions

- 6.1.2 Smart Food Processing Systems

- 6.1.3 Cold Chain Monitoring Solutions

- 6.1.4 Smart Packaging & Sensor Systems

- 6.1.5 Inventory & Warehouse Monitoring Platforms

- 6.2 By Deployment Mode

- 6.2.1 Cloud-Based Platforms

- 6.2.2 On-Premise Systems

- 6.2.3 Edge Computing Solutions

- 6.3 By End User

- 6.3.1 Food Manufacturing & Processing Enterprises

- 6.3.2 Food Logistics & Cold Chain Providers

- 6.3.3 Retail Food Distributors

- 6.3.4 Agricultural Food Producers

- 6.1 By Solution Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Technology Benchmarking

- 8.3 Strategic Partnerships & Ecosystem Development

- 8.4 Platform Integration Analysis

- 8.5 Brand Positioning Strategies

- 9. Company Profiles

- 9.1 IBM Corporation

- 9.2 Cisco Systems

- 9.3 SAP SE

- 9.4 Honeywell International Inc.

- 9.5 Siemens AG

- 9.6 Bosch Connected Industry

- 9.7 Oracle Corporation

- 9.8 Microsoft Corporation

- 9.9 Rockwell Automation

- 9.10 Schneider Electric

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 IoT Food Intelligence Forecast Engine

- 10.2 Real-Time Supply Chain Analytics Dashboard

- 10.3 Food Safety Risk Prediction Tracker

- 10.4 Cold Chain Optimization Analyzer

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of AI-Driven Food Monitoring Systems

- 11.2 Integration of Blockchain Traceability

- 11.3 Deployment of Edge Computing in Food Logistics

- 11.4 Strengthening Cybersecurity in Food IoT Systems

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Internet of Things (IoT) in Food Market Competitive Intensity & Market Structure Overview

The global Internet of Things (IoT) in food market is highly competitive and moderately fragmented, characterized by strong competition among industrial automation providers, cloud technology companies, food technology innovators, sensor manufacturers, and supply chain analytics solution providers. Competitive intensity is driven by platform integration capabilities, real-time monitoring accuracy, predictive analytics sophistication, food traceability compliance, digital infrastructure scalability, and end-to-end automation expertise.

The market structure consists of established industrial technology leaders with diversified IoT portfolios alongside specialized food-tech solution providers and emerging smart analytics companies focused on connected food ecosystem innovation. Competition is increasingly shaped by AI-powered food intelligence, edge computing deployment, blockchain-enabled traceability, and integrated cloud-based monitoring systems.

Rising food safety regulations, increasing demand for real-time traceability, expanding cold chain monitoring requirements, and rapid digital transformation across food manufacturing are significantly intensifying competition across the global IoT in food market.

Global Internet of Things (IoT) in Food Market Competitive Intensity & Market Structure Current Scenario

Leading Global IoT in Food Companies

IBM Corporation: Leading provider of blockchain-enabled food traceability and AI-powered food analytics solutions.

Cisco Systems: Major digital infrastructure company specializing in connected food monitoring and secure IoT network systems.

SAP SE: Prominent enterprise technology provider offering integrated food supply chain visibility and analytics platforms.

Honeywell International Inc.: Established industrial automation company focused on food processing automation and connected monitoring systems.

Siemens AG: Major smart manufacturing provider delivering advanced food processing and industrial IoT solutions.

Bosch Connected Industry: Strong market participant focused on intelligent sensor systems and connected industrial food ecosystems.

Oracle Corporation: Leading cloud technology company offering scalable food traceability and operational analytics platforms.

Microsoft Corporation: Major cloud and AI provider enabling smart food system intelligence and digital compliance frameworks.

Rockwell Automation: Key industrial automation provider delivering connected food manufacturing optimization solutions.

Schneider Electric: Recognized smart infrastructure company focused on energy-efficient food automation and connected operational intelligence.

Key Competitive Intensity & Market Structure Drivers

Stringent food safety and traceability regulations are intensifying competition around compliant digital monitoring platforms.

Rising adoption of predictive analytics and AI-powered quality management is accelerating technology differentiation.

Growing demand for cold chain monitoring solutions is strengthening competition around sensor precision and real-time alert systems.

Cloud-based platform scalability and edge computing integration are reshaping competitive positioning.

The increasing need for automated contamination prevention and supply chain visibility is driving innovation-focused competition.

Strategic Implications of Competitive Intensity & Market Structure

Technology providers are increasingly investing in AI-integrated analytics and real-time food intelligence platforms.

Strategic partnerships with food manufacturers and logistics operators are becoming essential for market penetration.

Blockchain-enabled traceability frameworks are strengthening product differentiation and compliance positioning.

Integrated cloud-edge infrastructure development is becoming central to operational efficiency and scalability.

Cybersecurity investment and secure food data management systems are enhancing competitive trust and resilience.

Global Internet of Things (IoT) in Food Market Competitive Intensity & Market Structure Forward Outlook

The global IoT in food market is expected to remain highly competitive as connected food ecosystems and digital compliance requirements continue accelerating.

Future competition will increasingly focus on autonomous food monitoring systems, AI-driven predictive quality analytics, blockchain-integrated traceability, and edge-enabled real-time operational intelligence.

North America will remain the dominant competitive region, while Asia-Pacific is expected to witness the fastest competitive expansion due to food industry digitalization.

Advancements in smart sensors, automated contamination detection systems, and cloud-native food intelligence platforms are expected to significantly reshape market dynamics.

Overall, companies that successfully combine scalable digital infrastructure, predictive analytics expertise, regulatory compliance capabilities, and intelligent automation solutions will remain strongly positioned in the evolving global IoT in food market.

Value Chain

Global Internet of Things (IoT) in Food Market Value Chain & Supply Chain Evolution Overview

The Global Internet of Things (IoT) in Food Market value chain is evolving from fragmented manual monitoring systems into a fully connected, data-driven, and AI-integrated food ecosystem. This transformation is being driven by rising food safety concerns, stricter regulatory compliance requirements, increasing demand for real-time supply chain visibility, and rapid automation across food manufacturing and logistics operations.

The IoT in food value chain is becoming increasingly interconnected through smart sensors, RFID systems, cloud platforms, edge computing, predictive analytics, and blockchain-enabled traceability solutions. These technologies are enabling end-to-end visibility across food production, processing, storage, transportation, and retail distribution networks.

The upstream segment begins with IoT hardware manufacturing, sensor development, RFID tag production, edge device engineering, cloud infrastructure services, and industrial software development. This includes semiconductor providers, sensor manufacturers, industrial automation firms, and cloud computing platform providers.

The operational core consists of food production monitoring, processing automation, cold chain management, real-time tracking systems, predictive maintenance platforms, and quality assurance analytics. AI-driven analytics and edge computing systems are increasingly enabling real-time decision-making and automated control across food systems.

The downstream segment includes logistics providers, cold chain operators, food retailers, manufacturing enterprises, agricultural producers, and digital supply chain platforms that integrate IoT-enabled monitoring into daily operations.

Overall, the IoT in food value chain is transitioning into a highly intelligent, real-time, and compliance-driven ecosystem where data transparency, automation, traceability, and predictive intelligence define competitive advantage.

Global Internet of Things (IoT) in Food Market Value Chain & Supply Chain Evolution Current Scenario

The current market structure reflects a rapidly evolving ecosystem combining traditional food supply chain systems with advanced digital monitoring and automation technologies.

Food manufacturers and processors are increasingly adopting IoT-enabled sensors and automation systems to improve production efficiency, reduce waste, and ensure compliance with food safety regulations.

Cold chain logistics is becoming highly digitized, with real-time temperature monitoring, GPS tracking, and automated alerts ensuring product quality and reducing spoilage risks.

Retailers are integrating smart inventory systems and RFID-based tracking solutions to optimize stock management and improve product freshness monitoring.

Despite rapid adoption, challenges such as interoperability issues, high initial deployment costs, and cybersecurity risks continue to influence operational scalability across the ecosystem.

Key Value Chain & Supply Chain Evolution Signals in Global IoT in Food Market

Real-time traceability expansion is transforming food supply chains by enabling end-to-end visibility from farm to consumer.

AI-integrated food analytics is improving predictive quality control, contamination detection, and operational decision-making.

Cold chain digitization is enhancing temperature-sensitive food logistics through continuous monitoring and automated alerts.

Edge computing adoption is enabling faster data processing and localized decision-making in food production environments.

Smart packaging integration is improving freshness tracking, spoilage detection, and consumer transparency.

Strategic Implications of Value Chain & Supply Chain Evolution in Global IoT in Food Market

The evolving IoT in food value chain presents strong strategic opportunities for technology providers, sensor manufacturers, cloud platform developers, and food industry operators.

Competitive advantage is increasingly determined by system interoperability, data accuracy, cybersecurity strength, scalability of IoT infrastructure, and predictive analytics capabilities.

Companies investing in integrated IoT ecosystems, AI-powered food intelligence platforms, and end-to-end traceability systems are expected to strengthen market leadership.

Strategic partnerships between food manufacturers, logistics providers, technology firms, and cloud service providers are becoming essential for large-scale deployment and operational efficiency.

Organizations capable of delivering secure, scalable, and fully integrated IoT food systems will achieve stronger long-term positioning in the market.

Global Internet of Things (IoT) in Food Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the IoT in food value chain is expected to evolve into a fully autonomous, AI-driven, and real-time intelligent food ecosystem.

AI-powered predictive systems will enable automated food safety monitoring, contamination detection, and demand forecasting across global supply chains.

Edge-enabled IoT systems will significantly reduce latency and improve real-time decision-making across production and logistics networks.

Blockchain-integrated traceability systems will enhance transparency, regulatory compliance, and consumer trust in food sourcing and handling.

Autonomous food processing and smart manufacturing facilities will further increase efficiency and reduce operational risks.

Ultimately, the future IoT in food value chain will be defined by intelligent automation, real-time data ecosystems, predictive analytics, and fully connected food supply networks.

Market-Specific Value Chain

- IoT Hardware Manufacturing: Sensor producers, RFID manufacturers, smart device developers, semiconductor suppliers

- Platform & Software Development: Cloud service providers, AI analytics platforms, food monitoring software developers

- Food Production Integration: Food manufacturers, processing plants, quality control systems, automation providers

- Cold Chain & Logistics: Refrigerated transport operators, warehouse monitoring systems, logistics tracking providers

- Retail & Distribution Systems: Smart retailers, inventory management systems, digital supply chain platforms

- Regulatory & Compliance Systems: Food safety authorities, certification bodies, traceability compliance platforms

- End-Use Applications: Food manufacturers, agricultural producers, logistics operators, retail consumers

Investment Activity

Global Internet of Things (IoT) in Food Market Investment & Funding Dynamics Overview

The Global Internet of Things (IoT) in Food Market is experiencing significant investment momentum driven by increasing demand for food safety monitoring, digital supply chain transformation, connected processing systems, and real-time traceability infrastructure. Technology providers, industrial automation companies, food processing enterprises, cloud analytics firms, and smart sensor manufacturers are actively investing in AI-powered food intelligence platforms, connected cold chain infrastructure, predictive maintenance systems, and smart traceability ecosystems.

Investment activity is accelerating due to rising demand for automated food processing systems, blockchain-enabled traceability solutions, smart packaging technologies, RFID tracking platforms, and cloud-based food analytics systems. The transition toward digitally connected food ecosystems is reshaping capital allocation across the market.

Additionally, growing investments in edge computing solutions, intelligent contamination detection systems, autonomous monitoring infrastructure, and AI-integrated compliance platforms are strengthening long-term growth opportunities globally.

Global Internet of Things (IoT) in Food Market Investment & Funding Dynamics Current Scenario

Currently, the global IoT in food market is witnessing strong capital inflows due to rising investment requirements for food safety modernization, supply chain digitization, automation upgrades, and connected quality assurance systems. Leading companies are heavily investing in real-time monitoring infrastructure, smart processing platforms, connected sensor networks, and predictive food analytics technologies.

The market is attracting increased funding into food traceability startups, industrial IoT solution providers, cloud food intelligence platforms, smart cold chain technology firms, and connected automation innovators.

The industry is witnessing active strategic partnerships, acquisitions, digital platform integrations, and food-tech collaborations as market participants seek to strengthen digital infrastructure and improve food system resilience.

Key Investment & Funding Dynamics Signals in Global Internet of Things (IoT) in Food Market

- Rising demand for real-time food traceability systems is accelerating digital infrastructure investments.

- Expansion of AI-powered food processing automation is increasing technology-focused capital deployment.

- Growing adoption of connected cold chain monitoring solutions is strengthening ecosystem funding.

- Strategic investments in edge computing and predictive analytics platforms are reshaping operational priorities.

- Partnerships between food manufacturers, automation firms, cloud providers, and IoT platform developers are improving ecosystem scalability.

- Increasing regulatory emphasis on food safety compliance, digital traceability, and contamination monitoring is supporting investor confidence.

- Rising demand for data-driven food quality optimization systems is accelerating R&D spending.

Strategic Implications of Investment & Funding Dynamics in Global Internet of Things (IoT) in Food Market

- Continuous investment in connected food monitoring infrastructure is essential for long-term competitiveness.

- Capital allocation toward AI-powered analytics and automation platforms will strengthen market positioning.

- Companies delivering secure, scalable, and compliance-driven food IoT ecosystems are expected to gain stronger market share.

- Strategic acquisitions and ecosystem partnerships will accelerate digital food infrastructure expansion.

- Investments in blockchain traceability, smart packaging, and autonomous monitoring systems will remain major priorities.

- Compliance with food safety regulations, cold chain standards, and traceability frameworks will remain critical for sustained growth.

- Organizations scaling intelligent food monitoring ecosystems are expected to capture substantial future opportunities.

Global Internet of Things (IoT) in Food Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Internet of Things (IoT) in Food Market is expected to maintain strong investment growth driven by digital food transformation, automation expansion, connected supply chain modernization, and stricter food safety regulations.

Future capital deployment will increasingly focus on AI-powered food intelligence systems, autonomous processing infrastructure, edge-enabled monitoring platforms, blockchain verification systems, and predictive contamination prevention technologies.

Advanced food analytics and connected operational intelligence are expected to become major long-term innovation priorities.

In conclusion, the Global Internet of Things (IoT) in Food Market represents a high-growth technology investment landscape where automation, AI integration, digital traceability, and intelligent food ecosystem development will define future capital strategies.

Technology & Innovation

Global Internet of Things (IoT) in Food Market Technology & Innovation Landscape Overview

The global IoT in food market is undergoing rapid technological transformation driven by advancements in smart sensor networks, AI-powered food analytics, blockchain-enabled traceability systems, edge computing architectures, and cloud-based food intelligence platforms. The evolution of IoT technologies in the food sector is increasingly focused on improving food safety, enhancing supply chain transparency, reducing waste, and enabling real-time operational decision-making across production and distribution networks.

Modern food IoT ecosystems are integrating connected temperature and humidity sensors, RFID tracking systems, machine learning-based quality prediction engines, automated alert systems, and digital twin supply chain models to optimize food production, storage, and logistics operations. These innovations are significantly improving traceability, reducing contamination risks, and enhancing compliance with global food safety standards.

The market is also witnessing widespread adoption of smart packaging technologies, AI-driven predictive quality monitoring, autonomous cold chain systems, and edge-enabled real-time analytics platforms that are redefining how food systems are monitored and managed globally.

Global IoT in Food Market Technology & Innovation Current Scenario

Currently, innovation in the IoT food market is centered around end-to-end digital traceability and real-time food safety intelligence systems. Traditional manual inspection and monitoring systems are being replaced by fully connected IoT infrastructures that provide continuous data visibility across the entire food value chain.

Smart supply chain monitoring systems are being widely deployed to track food products from farm to retail, ensuring transparency and reducing operational inefficiencies.

AI-powered predictive analytics are emerging as a major innovation driver, enabling early detection of spoilage risks, contamination events, and logistics disruptions.

Cold chain IoT systems are increasingly being used to maintain optimal temperature conditions during transportation and storage, significantly reducing food wastage.

Edge computing is enabling faster local data processing in food production environments, improving response times and operational accuracy.

Blockchain integration is strengthening food traceability by providing immutable records of product origin, processing history, and distribution pathways.

Key Technology & Innovation Trends in Global IoT in Food Market

- Smart Sensor Networks: Enabling continuous monitoring of temperature, humidity, and freshness conditions.

- AI-Powered Food Quality Analytics: Predicting spoilage and ensuring safety compliance.

- Blockchain-Based Traceability Systems: Enhancing transparency across the food supply chain.

- Edge Computing Integration: Supporting real-time data processing at production sites.

- Smart Cold Chain Monitoring: Maintaining temperature-sensitive food integrity during transport.

- RFID & Asset Tracking Technologies: Improving logistics visibility and inventory accuracy.

- Digital Twin Food Supply Chains: Simulating and optimizing end-to-end food operations.

- Smart Packaging Systems: Monitoring freshness and contamination in real time.

- Predictive Maintenance Platforms: Reducing downtime in food processing equipment.

- Cloud-Based Food Intelligence Platforms: Enabling centralized analytics and decision-making.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the IoT in food market by shifting competition from traditional monitoring systems toward fully connected, intelligent, and predictive food ecosystem platforms.

Companies investing in AI-driven analytics, integrated IoT platforms, and blockchain-based traceability systems are achieving stronger competitive differentiation through improved food safety, operational efficiency, and regulatory compliance.

The increasing convergence of IoT and artificial intelligence is enabling food companies to transition from reactive quality control to proactive, predictive food safety management.

Advanced automation systems are helping reduce human error, optimize logistics efficiency, and improve resource utilization across food supply chains.

However, high infrastructure costs, cybersecurity risks, interoperability challenges, and data integration complexities remain key barriers to large-scale deployment.

Global IoT in Food Market Technology & Innovation Forward Outlook

The future of IoT in the food industry is expected to evolve toward fully autonomous, AI-orchestrated, and self-optimizing food supply chain ecosystems capable of ensuring real-time safety, efficiency, and transparency.

Emerging innovations include autonomous cold chain logistics systems, AI-powered contamination detection sensors, hyper-connected digital food twins, and predictive global food security platforms.

Advanced IoT ecosystems may increasingly integrate with robotics and automation technologies to enable self-regulating food processing environments.

Real-time adaptive supply chain networks will further enhance resilience against disruptions, spoilage risks, and demand fluctuations.

Overall, the global IoT in food market is evolving toward a highly intelligent ecosystem combining connected sensors, AI-driven analytics, blockchain traceability, and automated decision systems to redefine global food safety, logistics, and supply chain efficiency.

Market Risk

Global Internet of Things (IoT) in Food Market Risk & Disruption Analysis

The Global Internet of Things (IoT) in Food Market operates within a high-growth, technology-intensive, and compliance-sensitive disruption environment shaped by cybersecurity vulnerabilities, system integration complexity, evolving food safety regulations, infrastructure modernization gaps, and digital transformation costs.

While the market demonstrates strong long-term growth driven by increasing food traceability requirements, automation adoption, smart supply chain development, and AI-powered operational optimization, it remains exposed to data security risks, interoperability challenges, implementation barriers, and regulatory compliance complexity.

A defining structural characteristic of the market is its dependence on connected sensor ecosystems, cloud-based analytics platforms, edge computing infrastructure, and seamless integration across fragmented food production and logistics systems, where profitability is strongly influenced by deployment scalability, system reliability, compliance readiness, and operational efficiency gains.

Food supply chain monitoring and asset tracking solutions remain dominant by market volume, while high-value growth is increasingly shifting toward predictive quality management systems, autonomous food processing intelligence, and AI-driven food safety analytics.

The market is also transitioning from isolated digital monitoring systems toward fully integrated, real-time, and intelligent food ecosystems, increasing strategic pressure for full-stack interoperability and digital resilience.

Global IoT in Food Market Current Risk Environment

The current market environment is characterized by accelerating digital adoption, operational integration challenges, and increasing compliance expectations.

One of the most significant disruption factors involves cybersecurity exposure. Connected food systems are increasingly vulnerable to cyberattacks, data breaches, ransomware threats, and operational disruptions that may compromise food safety monitoring systems.

Another major risk area is integration complexity across legacy food infrastructure. Many food manufacturers and logistics operators continue to operate fragmented systems that limit interoperability and delay digital transformation initiatives.

The market also faces implementation cost sensitivity, particularly among small and medium-sized food enterprises that may lack capital for large-scale IoT deployment.

Additionally, evolving food safety regulations, digital traceability requirements, and cross-border compliance standards remain structurally important operational risks.

In parallel, data reliability, sensor calibration inconsistencies, and infrastructure downtime risks continue to influence system trust and operational performance.

Key Market Risk & Disruption Signals in Global IoT in Food Market

- Cybersecurity Vulnerability: Connected food systems face increasing risks of cyberattacks and data compromise.

- Legacy System Integration Challenges: Interoperability issues may delay deployment and reduce efficiency gains.

- Regulatory Compliance Complexity: Evolving food traceability and monitoring standards increase operational requirements.

- High Deployment Costs: Infrastructure modernization demands significant capital investment.

- Sensor Reliability Risk: Calibration failures may compromise monitoring accuracy.

- Data Governance Pressure: Secure handling of operational and supply chain data is becoming increasingly critical.

- Operational Downtime Exposure: System failures can disrupt food processing and logistics continuity.

- Scalability Constraints: Expanding connected infrastructure across fragmented supply chains remains complex.

Strategic Implications of Market Risk & Disruption

The evolving disruption environment creates both substantial innovation opportunities and operational complexity.

One of the most important strategic implications is the need for secure, interoperable, and resilient digital food ecosystems.

Companies increasingly must invest in cybersecurity frameworks, cloud-edge hybrid architectures, predictive analytics, and automated compliance monitoring systems to remain competitive.

Vertical integration across sensors, software analytics, cloud infrastructure, food automation systems, and regulatory reporting platforms is becoming increasingly valuable.

The convergence of AI, blockchain traceability, autonomous food processing, and real-time analytics is reshaping value-chain economics.

Organizations with stronger digital infrastructure, system interoperability capabilities, and compliance-oriented innovation are expected to strengthen long-term market leadership.

Global IoT in Food Market Risk & Disruption Forward Outlook

Looking ahead to 2026???2033, the Global IoT in Food Market is expected to become increasingly intelligent, autonomous, and compliance-driven.

- Expansion of AI-Powered Predictive Food Systems: Intelligent analytics will capture growing strategic value.

- Greater Blockchain Traceability Adoption: Secure end-to-end food monitoring will strengthen trust.

- Rising Edge Computing Integration: Real-time localized processing will improve operational responsiveness.

- Higher Cybersecurity Investment: Digital resilience will become a critical competitive differentiator.

- Growth of Autonomous Food Processing: Connected automation systems will improve production efficiency.

- Stronger Regulatory Digitalization: Compliance reporting automation will become standard.

- Greater Food Ecosystem Interoperability: Unified data architectures will improve supply chain coordination.

- Increased Strategic Consolidation: Technology partnerships and acquisitions will strengthen platform capabilities.

In conclusion, the Global Internet of Things (IoT) in Food Market represents a highly dynamic, compliance-sensitive, and digitally transforming technology ecosystem where cybersecurity resilience, system interoperability, intelligent automation, and regulatory alignment will define long-term competitive success.

Regulatory Landscape

Global Internet of Things (IoT) in Food Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global Internet of Things (IoT) in food market is shaped by food safety compliance frameworks, traceability regulations, cold chain monitoring standards, data security laws, and digital infrastructure governance policies. As food systems become increasingly connected through IoT-enabled devices, regulators are placing greater emphasis on real-time transparency, contamination prevention, and end-to-end supply chain accountability.

IoT solution providers, food manufacturers, and logistics operators must comply with a wide range of regulations covering food hygiene standards, temperature monitoring requirements, product traceability mandates, cybersecurity protocols, and data integrity assurance across digital food ecosystems.

The rapid integration of smart sensors, AI-driven analytics, and cloud-based food monitoring systems is accelerating the development of digital compliance frameworks and standardized regulatory approaches for connected food supply chains.

Global IoT in Food Market Regulatory & Policy Environment Current Scenario

The current regulatory framework for IoT in the food market combines food safety laws, supply chain traceability requirements, industrial automation standards, and data protection regulations governing digital monitoring systems.

In North America and Europe, stringent food safety authorities enforce regulations requiring real-time monitoring of temperature-sensitive goods, hazard analysis systems, and digital traceability across food supply chains. Compliance with HACCP, FDA, and EFSA standards increasingly depends on IoT-enabled monitoring infrastructure.

Cold chain logistics regulations are particularly strict for perishable food products, requiring continuous temperature tracking, automated alerts, and documented compliance records throughout transportation and storage.

Asia-Pacific markets including China, India, Japan, and South Korea are strengthening food safety enforcement systems while rapidly adopting smart manufacturing and digital food monitoring technologies to support expanding food production and export networks.

Data privacy and cybersecurity regulations are also becoming increasingly important as IoT food systems generate large volumes of sensitive operational and supply chain data.

Key Regulatory & Policy Environment Signals in Global IoT in Food Market

- Food Safety Compliance Regulations: Mandatory standards ensure hygiene, contamination control, and safe food handling practices across the supply chain.

- Traceability Requirements: End-to-end digital tracking systems are required for monitoring food origin, processing, and distribution.

- Cold Chain Monitoring Standards: Temperature-sensitive food products must comply with continuous monitoring and reporting requirements.

- Data Security & Privacy Laws: IoT platforms must ensure secure handling of operational and consumer data.

- Industrial Automation Standards: Smart food processing systems must comply with operational safety and performance benchmarks.

- Digital Compliance Frameworks: Governments are introducing structured guidelines for connected food ecosystem governance.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging food companies and IoT solution providers to invest heavily in real-time monitoring infrastructure, blockchain-based traceability systems, AI-powered compliance analytics, and secure cloud-based food data platforms.

Food safety compliance requirements are accelerating the deployment of predictive contamination detection systems, automated hazard alerts, and continuous quality monitoring technologies across production and logistics operations.

Cold chain regulations are driving increased adoption of smart temperature sensors, edge computing devices, and automated logistics tracking systems to ensure uninterrupted compliance throughout transportation networks.

Cybersecurity and data governance requirements are also supporting greater innovation in encrypted IoT communication systems, secure device authentication protocols, and regulated cloud analytics platforms.

Global alignment of food safety and digital traceability standards is creating competitive advantages for companies operating fully integrated, compliant, and transparent IoT food ecosystems.

Global IoT in Food Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global IoT in food market is expected to become increasingly data-driven, automation-centric, and digitally standardized across global food supply chains.

Governments are likely to enforce stricter real-time food monitoring requirements, expanded digital traceability mandates, and enhanced cybersecurity compliance obligations for connected food systems.

Emerging technologies such as AI-powered food safety prediction systems, blockchain traceability platforms, and autonomous food logistics networks may face more detailed regulatory validation and certification requirements.

Cross-border harmonization of food safety and digital compliance frameworks is expected to strengthen as global food trade becomes more dependent on IoT-enabled transparency systems.

Overall, regulatory and policy developments will remain a core growth driver, with companies investing in secure IoT infrastructure, advanced compliance automation, and intelligent food monitoring systems expected to maintain long-term competitive advantage.