Global Textile Market Report, Size, Share and Forecast 2026–2033

Global Textile Market Forecast Snapshot (2026???2033)

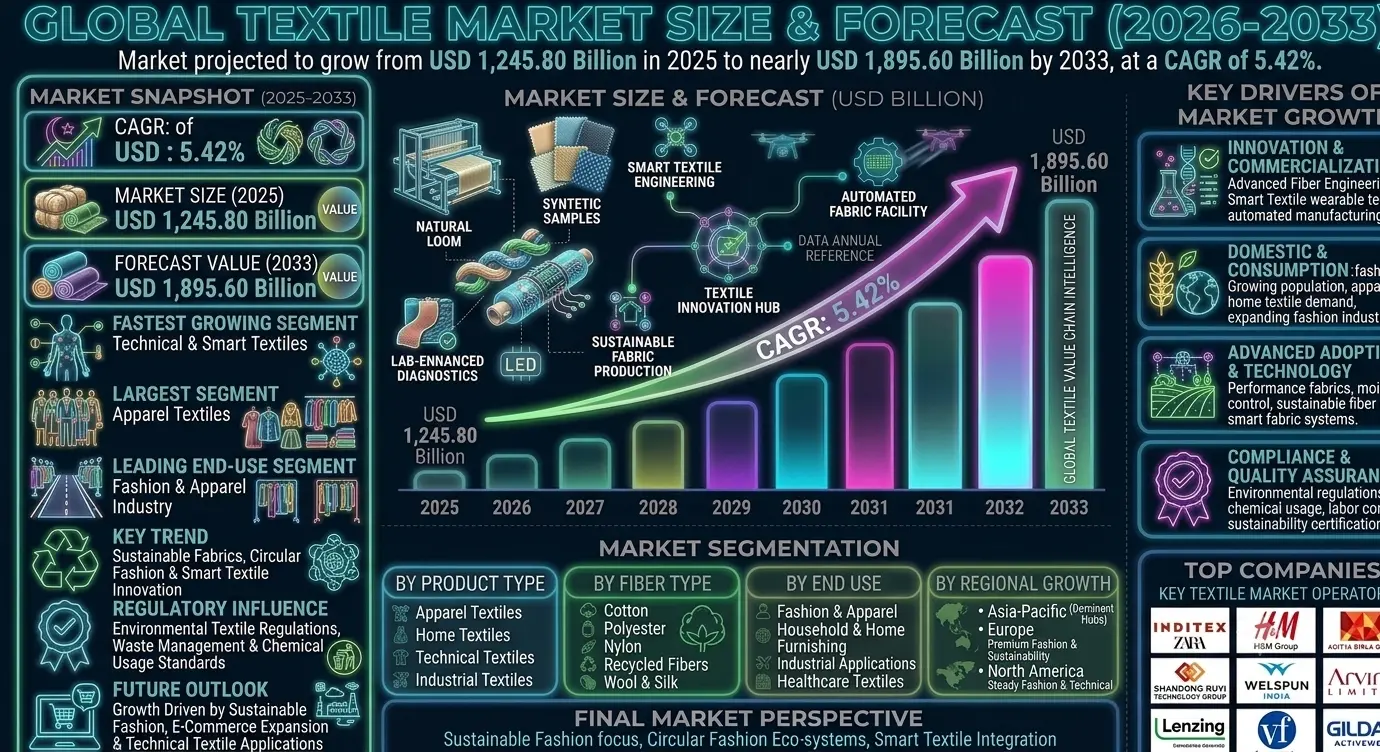

| Metric | Value |

|---|---|

| Market Size (2025) | USD 1,245.80 Billion |

| Market Size (2033) | USD 1,895.60 Billion |

| CAGR (2026???2033) | 5.42% |

| Largest Segment | Apparel Textiles |

| Fastest Growing Segment | Technical & Smart Textiles |

| Leading End-Use Segment | Fashion & Apparel Industry |

| Key Trend | Sustainable Fabrics, Circular Fashion & Smart Textile Innovation |

| Regulatory Influence | Environmental Textile Regulations, Waste Management Policies & Chemical Usage Standards |

| Future Outlook | Growth Driven by Sustainable Fashion, E-Commerce Expansion & Technical Textile Applications |

Global Textile Market Size & Forecast

The Global Textile Market is expected to witness steady expansion during the forecast period from 2026 to 2033. The market was valued at USD 1,245.80 billion in 2025 and is projected to reach approximately USD 1,895.60 billion by 2033, registering a CAGR of 5.42%. The market growth is primarily driven by rising global population, increasing demand for apparel and home textiles, expanding fashion industry, and rapid growth of e-commerce retail channels. Textiles remain a foundational industry supporting apparel, industrial applications, automotive interiors, medical textiles, and technical fabric systems. In addition, growing demand for sustainable fabrics, recycled fibers, and smart textiles is accelerating long-term industry transformation.Global Textile Market Overview

The textile industry involves the production, processing, and distribution of fibers, yarns, fabrics, and finished textile products used across multiple end-use sectors. The market includes natural fibers (cotton, wool, silk), synthetic fibers (polyester, nylon), blended fabrics, technical textiles, and smart textile solutions. Textile products are widely utilized across apparel, home furnishings, industrial applications, automotive interiors, healthcare textiles, and protective clothing. The industry is shifting toward sustainable production methods, circular economy models, digital textile manufacturing, and high-performance functional fabrics.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Advancements in fiber engineering, smart textiles, nanotechnology-based fabrics, and automated weaving and knitting technologies are transforming textile manufacturing. Growing demand for performance-enhancing fabrics, moisture control textiles, and wearable technology integration is accelerating innovation.Market Implications

Companies investing in smart textiles, sustainable fibers, and advanced manufacturing technologies are expected to strengthen market competitiveness.2. Compliance and Risk Repricing

Environmental regulations, chemical usage restrictions, labor compliance standards, and sustainability certifications are reshaping textile production processes. Governments and global organizations are pushing for reduced textile waste and sustainable manufacturing practices.Market Implications

Firms adopting eco-friendly production, recycled materials, and compliant supply chains are likely to gain stronger global acceptance.3. Competitive and Value-Chain Reconfiguration

The market is highly fragmented with fiber producers, textile mills, apparel brands, and retail chains competing across global supply networks. E-commerce platforms and fast fashion models are reshaping traditional textile value chains.Market Implications

Companies focusing on vertical integration, digital supply chains, and sustainable fashion ecosystems may achieve stronger market positioning.4. Capital and Capacity Scaling

Rising investments in textile manufacturing hubs, automation technologies, and sustainable fabric production are supporting market expansion. Emerging economies are becoming key production centers for global textile supply chains.Market Implications

Organizations scaling sustainable and high-efficiency production facilities are expected to capture future opportunities.Market Segmentation Analysis

By Product Type

1. Apparel Textiles

Largest segment due to high global demand for clothing and fashion products.2. Home Textiles

Strong demand driven by residential furnishing and interior design trends.3. Technical Textiles

Fastest-growing segment supported by industrial, automotive, and healthcare applications.4. Industrial Textiles

Widely used in construction, filtration, and protective applications.By Fiber Type

1. Cotton

Largest segment due to comfort, breathability, and widespread usage.2. Polyester

Strong growth due to durability, cost efficiency, and versatility.3. Nylon

Used in industrial and performance applications.4. Wool & Silk

Premium segment driven by luxury fashion demand.5. Recycled Fibers

Fastest-growing segment due to sustainability trends.By End Use

1. Fashion & Apparel Industry

Largest segment due to continuous global clothing demand.2. Household & Home Furnishing

Strong demand from residential and hospitality sectors.3. Industrial Applications

Growing usage in automotive, construction, and engineering sectors.4. Healthcare Textiles

Increasing demand for medical clothing, masks, and hygiene products.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global textile market due to large-scale manufacturing, low production costs, strong export capacity, and presence of major textile hubs in China, India, Bangladesh, and Vietnam.Europe

Europe remains a key market driven by premium fashion brands, sustainable textile innovation, and high-quality production standards.North America

North America is witnessing steady growth supported by fashion demand, technical textiles, and increasing sustainable fabric adoption.Latin America

Latin America is gradually expanding due to rising apparel consumption and regional manufacturing development.Middle East & Africa

The region is experiencing emerging growth driven by retail expansion, textile imports, and growing fashion consumption.Competitive Landscape

The Global Textile Market is highly fragmented with global manufacturers, fashion brands, and industrial textile producers competing across different segments.Key Companies Operating in the Market Include:

- Inditex (Zara)

- H&M Group

- Aditya Birla Group

- Shandong Ruyi Technology Group

- Welspun India

- Arvind Limited

- Toray Industries

- Lenzing AG

- VF Corporation

- Gildan Activewear

Strategic Outlook

The future of the textile market will be shaped by sustainable fashion, circular economy models, smart textiles, and digital manufacturing technologies. Automation, AI-driven design systems, recycled fiber innovation, and on-demand manufacturing will significantly improve efficiency and sustainability. The rise of e-commerce, fast fashion evolution, and technical textile applications is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Textile Market remains a core pillar of the global manufacturing and consumer goods ecosystem. Rising fashion demand, sustainability initiatives, and technological advancements continue driving long-term growth. Companies capable of delivering sustainable, innovative, and cost-efficient textile solutions will be best positioned to capture future opportunities. The convergence of smart fabrics, circular fashion, and global supply chain transformation is expected to redefine the future of the textile industry.Table of Contents

Table of Contents

- Executive Summary

- Global Textile Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends & Sustainability Transformation

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of the Textile Industry

- Scope of the Global Textile Market

- Evolution of Textile Manufacturing & Fabric Technologies

- Role of Textiles in Global Industrial & Consumer Economy

- Value Chain Analysis of Textile Production

- Regulatory Influence (Environmental Textile Regulations, Waste Management Policies & Chemical Usage Standards)

- Transition Toward Sustainable Fashion & Circular Economy Models

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Innovation and Commercialization Acceleration in Smart & Technical Textiles

- Compliance and Risk Repricing in Environmental & Textile Regulations

- Competitive and Value-Chain Reconfiguration Across Global Textile Industry

- Capital and Capacity Scaling in Textile Manufacturing & Production Hubs

- Market Restraints

- High Environmental Impact of Textile Production

- Volatility in Raw Material Prices

- Intense Competition from Low-Cost Manufacturing Regions

- Market Opportunities

- Expansion of Smart & Technical Textiles

- Growth in Recycled Fiber & Circular Fashion Models

- Increasing Demand for Sustainable Apparel

- Integration of Digital & On-Demand Manufacturing

- Market Challenges

- Supply Chain Fragmentation Across Global Textile Industry

- Environmental Compliance Costs

- Transition Toward Sustainable Production Models

- Structural Drivers of Market Growth

- Global Textile Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Demand-Supply Trends

- Pricing Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Product Type

- Apparel Textiles (Largest Segment)

- Home Textiles

- Technical Textiles (Fastest-Growing Segment)

- Industrial Textiles

- By Fiber Type

- Cotton (Largest Segment)

- Polyester

- Nylon

- Wool & Silk

- Recycled Fibers (Fastest-Growing Segment)

- By End Use

- Fashion & Apparel Industry (Largest Segment)

- Household & Home Furnishing

- Industrial Applications

- Healthcare Textiles

- By Product Type

- Regional Market Analysis

- Asia-Pacific (Largest Market)

- Europe

- North America

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Fragmentation Analysis

- Key Player Benchmarking

- Strategic Developments

- Sustainable Fashion & Digital Manufacturing Strategies

- Supply Chain, Partnerships & Expansion Trends

- Company Profiles

- Inditex (Zara)

- H&M Group

- Aditya Birla Group

- Shandong Ruyi Technology Group

- Welspun India

- Arvind Limited

- Toray Industries

- Lenzing AG

- VF Corporation

- Gildan Activewear

- Strategic Outlook

- Future of Sustainable Fashion & Circular Economy Models

- AI-Driven Textile Design & Automation

- Expansion of Recycled Fiber & Eco-Friendly Materials

- Growth of Smart Textile Applications

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Textile Market Competitive Intensity & Market Structure Overview

The Global Textile Market is highly fragmented and intensely competitive, comprising large multinational apparel conglomerates, integrated textile manufacturers, regional fabric producers, and emerging technical textile innovators. Competitive intensity is primarily driven by cost efficiency, production scale, supply chain integration, product innovation, sustainability compliance, and global sourcing capabilities.

Companies compete across apparel textiles, home textiles, technical textiles, and industrial textile segments, serving fashion brands, industrial users, healthcare providers, and automotive manufacturers. Rising demand for fast fashion, sustainable fabrics, and high-performance technical textiles is intensifying competition across both developed and emerging economies.

The market structure is shifting from traditional mass textile production toward digitally enabled, sustainable, and vertically integrated supply chains. Increasing adoption of circular fashion models, recycled fibers, and smart textile technologies is reshaping competitive positioning across the industry.

Global Textile Market Competitive Intensity & Market Structure Current Scenario

Leading Global Textile Market Participants

Inditex (Zara): A global leader in fast fashion retail with a highly integrated supply chain enabling rapid textile-to-apparel production and distribution.

H&M Group: A major fashion retailer driving large-scale textile demand with a strong focus on sustainable fashion and recycled materials.

Aditya Birla Group: A diversified conglomerate with a strong presence in fiber production, textiles, and apparel manufacturing across global markets.

Shandong Ruyi Technology Group: A major textile and apparel manufacturer with extensive global acquisitions and vertically integrated production capabilities.

Welspun India: A leading home textile manufacturer specializing in bedding, towels, and furnishing products for global retail chains.

Arvind Limited: A major textile producer known for denim manufacturing, apparel fabrics, and advanced textile solutions.

Toray Industries: A global leader in advanced fibers, synthetic textiles, and high-performance industrial materials.

Lenzing AG: A key producer of sustainable cellulose fibers widely used in eco-friendly textile manufacturing.

VF Corporation: A global apparel and footwear company with strong demand for textile sourcing across multiple fashion brands.

Gildan Activewear: A major manufacturer of basic apparel and textile products with large-scale production capabilities and global distribution.

Key Competitive Intensity & Market Structure Drivers

Rising demand for sustainable fabrics, recycled fibers, and environmentally responsible production is intensifying competition among textile manufacturers globally.

The rapid expansion of fast fashion and e-commerce platforms is increasing pressure on supply chains to deliver cost-efficient and high-speed textile production.

Advancements in technical textiles, smart fabrics, and performance materials are creating new competitive opportunities in industrial and specialty applications.

Environmental regulations, chemical usage restrictions, and sustainability certification requirements are forcing companies to modernize production processes and material sourcing strategies.

Increasing adoption of vertical integration and digital supply chain management is reshaping competitive advantage across global textile networks.

Strategic Implications of Competitive Intensity & Market Structure

Companies with large-scale manufacturing capacity, integrated supply chains, and strong global retail partnerships are expected to maintain significant competitive advantages.

Investment in sustainable fiber technologies, recycled materials, and circular fashion production systems is becoming a key differentiator in the evolving textile landscape.

Manufacturers focusing on automation, AI-driven production planning, and digital textile design are likely to strengthen operational efficiency and market positioning.

Strategic expansion into technical textiles and high-performance fabric applications is enabling companies to diversify revenue streams beyond traditional apparel markets.

Organizations capable of balancing cost efficiency, sustainability compliance, innovation, and global scalability will be best positioned to compete effectively across the global textile market.

Global Textile Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global textile market is expected to become increasingly innovation-driven as sustainable fashion, circular economy models, and smart textile technologies gain momentum worldwide.

Future competition will be shaped by advancements in recycled fiber production, AI-enabled manufacturing, on-demand apparel systems, and digital supply chain optimization.

Manufacturers are expected to increase investments in automation, sustainable materials, and high-performance textile development to strengthen long-term competitiveness.

Over the forecast period, companies that successfully integrate sustainability, cost efficiency, technological innovation, and global supply chain resilience will be best positioned to lead the evolving global textile industry.

Value Chain

Global Textile Market Value Chain & Supply Chain Evolution Overview

The Global Textile Market operates through a complex and highly interconnected value chain spanning raw fiber production, yarn spinning, fabric manufacturing, textile processing, garment production, distribution, retail, and end-user consumption. The industry serves as a foundational pillar for multiple sectors including apparel, home furnishings, automotive interiors, healthcare textiles, and industrial applications.

A defining characteristic of the textile value chain is its globalized and multi-tiered structure, where raw material sourcing, manufacturing, and consumption are often distributed across different regions. This has led to highly optimized but also complex supply chain networks that depend on cost efficiency, production capacity, and trade logistics.

The industry is undergoing a major transition toward sustainability, circular economy models, digital manufacturing systems, and smart textile integration. Manufacturers are increasingly focusing on recycled fibers, eco-friendly dyeing processes, and low-impact production technologies to meet environmental regulations and consumer expectations.

At the same time, technological advancements in automation, AI-driven design, and smart fabric engineering are reshaping how textiles are produced and delivered. This is creating a more responsive, efficient, and innovation-led value chain across the global textile ecosystem.

Global Textile Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Fiber Production: Cultivation and production of cotton, wool, silk, and synthetic fiber manufacturing including polyester, nylon, and recycled fiber inputs.

- Yarn Spinning & Fiber Processing: Conversion of raw fibers into yarns and threads through spinning, blending, and chemical processing operations.

- Fabric Manufacturing: Weaving, knitting, and non-woven fabric production for apparel, home textiles, and industrial applications.

- Dyeing, Finishing & Processing: Application of color, texture enhancement, chemical finishing, and functional treatment including waterproofing, flame resistance, and antimicrobial properties.

- Garment & Product Manufacturing: Production of apparel, home furnishings, technical textiles, and industrial textile products.

- Distribution & Retail Channels: Supply through fashion brands, retail stores, e-commerce platforms, wholesalers, and export distribution networks.

- End User Consumption: Fashion consumers, households, industrial users, healthcare institutions, and automotive manufacturers utilizing textile products.

Company-to-Stage Mapping

- Raw Fiber Production: Cotton producers, polyester and synthetic fiber manufacturers, Lenzing AG, Toray Industries, and recycled fiber suppliers.

- Yarn Spinning & Fiber Processing: Aditya Birla Group, Arvind Limited, Shandong Ruyi Technology Group, and regional spinning mills.

- Fabric Manufacturing: Welspun India, Arvind Limited, and global textile mill operators producing woven, knitted, and non-woven fabrics.

- Dyeing, Finishing & Processing: Specialized textile processing units, chemical treatment providers, and finishing technology companies.

- Garment & Product Manufacturing: Inditex (Zara), H&M Group, VF Corporation, Gildan Activewear, and apparel manufacturing networks.

- Distribution & Retail Channels: Global fashion retailers, e-commerce platforms, wholesale distributors, and export networks.

- End User Consumption: Fashion consumers, households, industrial users, and institutional buyers across global markets.

Key Value Chain & Supply Chain Evolution Signals in Global Textile Market

Expansion of Sustainable Fabric Production

The adoption of recycled fibers, organic cotton, and eco-friendly materials is increasing as brands respond to environmental concerns and sustainability regulations.

Growth of Circular Fashion Models

Textile recycling, reuse systems, and closed-loop production processes are gaining traction to reduce waste and improve resource efficiency.

Digital Transformation in Textile Manufacturing

AI-driven design tools, automated weaving systems, and digital textile printing are improving production speed, customization, and cost efficiency.

Expansion of Technical and Smart Textiles

High-performance fabrics with functional properties such as moisture control, durability, and embedded sensors are driving new application areas.

Global Supply Chain Diversification

Manufacturers are diversifying production bases across Asia-Pacific, Africa, and Latin America to reduce dependency risks and optimize costs.

Rise of E-Commerce and Fast Fashion Integration

Digital retail platforms and fast fashion business models are reshaping demand cycles and accelerating product turnover in global markets.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Sustainable Manufacturing Technologies

Companies adopting low-impact dyeing, recycled fiber integration, and energy-efficient production systems can strengthen long-term competitiveness.

Expansion of Digital Supply Chain Systems

AI-based forecasting, automated production planning, and real-time inventory management are improving supply chain responsiveness.

Strengthening Vertical Integration Strategies

Firms integrating fiber production, fabric manufacturing, and apparel production can achieve better cost control and supply chain efficiency.

Growth of Smart Textile Innovation

Development of wearable textiles and functional fabrics is creating new opportunities in healthcare, sports, and industrial applications.

Expansion of Recycled Fiber Ecosystems

Investments in fiber recycling infrastructure and circular material systems are becoming critical for sustainability compliance.

Enhancement of Global Manufacturing Hubs

Emerging economies are strengthening their role as global textile production centers, improving export competitiveness.

Global Textile Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the textile value chain is expected to become more digital, sustainable, and innovation-driven, with strong emphasis on circular economy practices and smart textile integration.

Key Future Developments Include:

- Expansion of recycled fiber and circular textile production systems.

- Increased adoption of AI-powered textile design and manufacturing automation.

- Growth of smart textiles and wearable technology applications.

- Strengthening of sustainable fashion and eco-friendly production standards.

- Diversification of global manufacturing and supply chain networks.

- Expansion of e-commerce-driven textile consumption models.

As the market evolves, competitive advantage will increasingly depend on the ability to combine sustainability, digital transformation, cost efficiency, and product innovation within an integrated textile value chain ecosystem.

Companies that successfully integrate advanced manufacturing technologies, sustainable fiber systems, digital supply chain management, and innovative textile solutions will achieve stronger global positioning and long-term growth in the Global Textile Market.

Investment Activity

Global Halal Market Investment & Funding Dynamics Overview

The Global Halal Market is witnessing significant investment activity driven by the expanding Muslim population, increasing demand for certified halal products, rising global halal trade, and growing adoption of premium halal lifestyle offerings. Food manufacturers, consumer goods companies, private equity firms, sovereign investment funds, certification agencies, and digital commerce platforms are actively investing in halal production infrastructure, certification technologies, halal supply chains, export capabilities, and digital verification systems.

Investment momentum is accelerating as governments and private-sector participants prioritize halal ecosystem development to strengthen domestic industries and expand export competitiveness. Capital deployment is increasingly focused on halal food processing facilities, halal cosmetics manufacturing, pharmaceutical compliance systems, halal logistics networks, and digital certification platforms.

Additionally, growing investments in blockchain-based traceability solutions, premium halal branding, halal industrial parks, and e-commerce-enabled halal marketplaces are creating substantial long-term opportunities across the global halal industry.

Global Halal Market Investment & Funding Dynamics Current Scenario

Currently, the market is experiencing strong capital inflows as businesses expand halal-certified product portfolios and strengthen supply chain transparency. Industry participants are investing heavily in certification compliance systems, export-oriented manufacturing facilities, quality assurance infrastructure, and digital consumer engagement platforms.

The market is benefiting from government-backed halal development initiatives, trade promotion programs, and regulatory frameworks designed to strengthen halal industry competitiveness. Significant investments are being directed toward halal industrial zones, certification infrastructure, digital verification technologies, and international market expansion strategies.

Furthermore, strategic collaborations among food manufacturers, cosmetics companies, pharmaceutical firms, certification bodies, logistics providers, and technology companies are accelerating investment activity and enhancing value-chain integration.

Key Investment & Funding Dynamics Signals in Global Halal Market

- Growing demand for halal-certified food, beverages, cosmetics, and pharmaceutical products is driving large-scale investment activity.

- Expansion of global halal export markets is increasing capital deployment across production and distribution infrastructure.

- Government-supported halal ecosystem development programs and certification initiatives are accelerating industry funding.

- Rising adoption of digital halal certification and verification platforms is attracting technology-focused investments.

- Strategic investments in halal logistics, cold-chain infrastructure, and supply-chain traceability are creating long-term growth opportunities.

- Growing consumer preference for ethical, transparent, and certified products is strengthening investment confidence.

- Increasing adoption of blockchain-enabled traceability and compliance monitoring systems is supporting innovation-led funding.

Strategic Implications of Investment & Funding Dynamics in Global Halal Market

- Continuous investment in certification technology, compliance systems, and supply-chain transparency is essential for maintaining market credibility.

- Capital allocation toward halal manufacturing facilities, export infrastructure, and digital commerce platforms will strengthen competitive positioning.

- Companies developing premium halal lifestyle products and services are expected to secure stronger long-term growth opportunities.

- Strategic partnerships between manufacturers, certification agencies, technology providers, and retailers will accelerate market expansion.

- Investments in automation, digital verification, and consumer trust platforms will remain key growth priorities.

- Compliance with mandatory halal certification regulations, BPJPH requirements, and international export standards will continue influencing investment decisions.

- Organizations building integrated halal ecosystems across production, certification, logistics, and retail channels are expected to capture substantial future value.

Global Halal Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Halal Market is expected to maintain strong investment momentum driven by rising halal consumption, expanding international trade opportunities, increasing certification adoption, and accelerating digital transformation across halal value chains.

Future capital deployment will increasingly focus on digital certification platforms, blockchain-based traceability systems, export-oriented manufacturing facilities, halal logistics infrastructure, and premium halal consumer products.

As governments and industry stakeholders continue prioritizing halal compliance, consumer trust, and export competitiveness, investment activity is expected to expand across certification ecosystems, production infrastructure, digital commerce platforms, and global distribution networks.

In conclusion, the Global Halal Market represents a highly attractive investment landscape where digital certification, halal supply-chain integration, premium lifestyle branding, export development, and compliance-driven innovation will define future funding priorities, competitive differentiation, and long-term market growth.

Technology & Innovation

Global Textile Market Value Chain & Supply Chain Evolution Overview

The Global Textile Market operates through a complex and highly interconnected value chain spanning raw fiber production, yarn spinning, fabric manufacturing, textile processing, garment production, distribution, retail, and end-user consumption. The industry serves as a foundational pillar for multiple sectors including apparel, home furnishings, automotive interiors, healthcare textiles, and industrial applications.

A defining characteristic of the textile value chain is its globalized and multi-tiered structure, where raw material sourcing, manufacturing, and consumption are often distributed across different regions. This has led to highly optimized but also complex supply chain networks that depend on cost efficiency, production capacity, and trade logistics.

The industry is undergoing a major transition toward sustainability, circular economy models, digital manufacturing systems, and smart textile integration. Manufacturers are increasingly focusing on recycled fibers, eco-friendly dyeing processes, and low-impact production technologies to meet environmental regulations and consumer expectations.

At the same time, technological advancements in automation, AI-driven design, and smart fabric engineering are reshaping how textiles are produced and delivered. This is creating a more responsive, efficient, and innovation-led value chain across the global textile ecosystem.

Global Textile Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Fiber Production: Cultivation and production of cotton, wool, silk, and synthetic fiber manufacturing including polyester, nylon, and recycled fiber inputs.

- Yarn Spinning & Fiber Processing: Conversion of raw fibers into yarns and threads through spinning, blending, and chemical processing operations.

- Fabric Manufacturing: Weaving, knitting, and non-woven fabric production for apparel, home textiles, and industrial applications.

- Dyeing, Finishing & Processing: Application of color, texture enhancement, chemical finishing, and functional treatment including waterproofing, flame resistance, and antimicrobial properties.

- Garment & Product Manufacturing: Production of apparel, home furnishings, technical textiles, and industrial textile products.

- Distribution & Retail Channels: Supply through fashion brands, retail stores, e-commerce platforms, wholesalers, and export distribution networks.

- End User Consumption: Fashion consumers, households, industrial users, healthcare institutions, and automotive manufacturers utilizing textile products.

Company-to-Stage Mapping

- Raw Fiber Production: Cotton producers, polyester and synthetic fiber manufacturers, Lenzing AG, Toray Industries, and recycled fiber suppliers.

- Yarn Spinning & Fiber Processing: Aditya Birla Group, Arvind Limited, Shandong Ruyi Technology Group, and regional spinning mills.

- Fabric Manufacturing: Welspun India, Arvind Limited, and global textile mill operators producing woven, knitted, and non-woven fabrics.

- Dyeing, Finishing & Processing: Specialized textile processing units, chemical treatment providers, and finishing technology companies.

- Garment & Product Manufacturing: Inditex (Zara), H&M Group, VF Corporation, Gildan Activewear, and apparel manufacturing networks.

- Distribution & Retail Channels: Global fashion retailers, e-commerce platforms, wholesale distributors, and export networks.

- End User Consumption: Fashion consumers, households, industrial users, and institutional buyers across global markets.

Key Value Chain & Supply Chain Evolution Signals in Global Textile Market

Expansion of Sustainable Fabric Production

The adoption of recycled fibers, organic cotton, and eco-friendly materials is increasing as brands respond to environmental concerns and sustainability regulations.

Growth of Circular Fashion Models

Textile recycling, reuse systems, and closed-loop production processes are gaining traction to reduce waste and improve resource efficiency.

Digital Transformation in Textile Manufacturing

AI-driven design tools, automated weaving systems, and digital textile printing are improving production speed, customization, and cost efficiency.

Expansion of Technical and Smart Textiles

High-performance fabrics with functional properties such as moisture control, durability, and embedded sensors are driving new application areas.

Global Supply Chain Diversification

Manufacturers are diversifying production bases across Asia-Pacific, Africa, and Latin America to reduce dependency risks and optimize costs.

Rise of E-Commerce and Fast Fashion Integration

Digital retail platforms and fast fashion business models are reshaping demand cycles and accelerating product turnover in global markets.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Sustainable Manufacturing Technologies

Companies adopting low-impact dyeing, recycled fiber integration, and energy-efficient production systems can strengthen long-term competitiveness.

Expansion of Digital Supply Chain Systems

AI-based forecasting, automated production planning, and real-time inventory management are improving supply chain responsiveness.

Strengthening Vertical Integration Strategies

Firms integrating fiber production, fabric manufacturing, and apparel production can achieve better cost control and supply chain efficiency.

Growth of Smart Textile Innovation

Development of wearable textiles and functional fabrics is creating new opportunities in healthcare, sports, and industrial applications.

Expansion of Recycled Fiber Ecosystems

Investments in fiber recycling infrastructure and circular material systems are becoming critical for sustainability compliance.

Enhancement of Global Manufacturing Hubs

Emerging economies are strengthening their role as global textile production centers, improving export competitiveness.

Global Textile Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the textile value chain is expected to become more digital, sustainable, and innovation-driven, with strong emphasis on circular economy practices and smart textile integration.

Key Future Developments Include:

- Expansion of recycled fiber and circular textile production systems.

- Increased adoption of AI-powered textile design and manufacturing automation.

- Growth of smart textiles and wearable technology applications.

- Strengthening of sustainable fashion and eco-friendly production standards.

- Diversification of global manufacturing and supply chain networks.

- Expansion of e-commerce-driven textile consumption models.

As the market evolves, competitive advantage will increasingly depend on the ability to combine sustainability, digital transformation, cost efficiency, and product innovation within an integrated textile value chain ecosystem.

Companies that successfully integrate advanced manufacturing technologies, sustainable fiber systems, digital supply chain management, and innovative textile solutions will achieve stronger global positioning and long-term growth in the Global Textile Market.

Market Risk

Global Textile Market Risk Factors & Disruption Threats Overview

The Global Textile Market is a foundational component of the global manufacturing and consumer goods ecosystem, supporting apparel, home furnishings, industrial applications, automotive interiors, and technical textile systems. While the industry benefits from strong demand driven by population growth, fashion consumption, and expanding e-commerce channels, it faces significant structural risks related to environmental regulations, raw material price volatility, supply chain fragmentation, labor cost pressures, and rapidly changing consumer preferences.

A major structural risk is the increasing regulatory pressure on environmental sustainability. Textile manufacturing is resource-intensive and heavily scrutinized for water usage, chemical processing, dyeing impacts, and waste generation. Stricter environmental regulations and compliance standards are increasing production costs and operational complexity across global supply chains.

Another key disruption factor is raw material and input cost volatility. Fluctuations in cotton, polyester, synthetic fibers, and energy prices can significantly impact manufacturing margins, especially in highly competitive and price-sensitive apparel segments.

The market is also exposed to supply chain fragmentation risks due to its globally distributed production model. Dependence on multiple countries for fiber production, fabric processing, garment assembly, and retail distribution creates vulnerability to geopolitical disruptions, trade restrictions, and logistics bottlenecks.

Additionally, the fast fashion cycle and rapidly shifting consumer preferences create demand unpredictability, forcing manufacturers and brands to continuously adapt production volumes, designs, and sourcing strategies.

Global Textile Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by strong demand recovery across apparel, home textiles, and industrial textile segments, supported by e-commerce growth and global fashion consumption trends.

Sustainability has become a central industry focus, with increasing adoption of recycled fibers, eco-friendly fabrics, and circular fashion models aimed at reducing environmental impact.

At the same time, manufacturers are facing rising production costs due to energy inflation, labor shortages in key manufacturing regions, and stricter environmental compliance requirements.

Global supply chain realignment is underway as companies diversify sourcing locations to reduce dependency on concentrated manufacturing hubs and improve resilience against disruptions.

Competition remains intense across all segments, with fast fashion brands, premium apparel companies, and industrial textile manufacturers competing on cost efficiency, innovation, and sustainability credentials.

Key Risk Factors & Disruption Threats Signals in Global Textile Market

A major disruption signal is the rapid acceleration of sustainable fashion initiatives, including circular economy models, textile recycling technologies, and biodegradable fabric development.

Another important signal is the rise of smart textiles and technical fabrics, integrating electronics, sensors, and performance-enhancing properties into traditional textile applications.

The expansion of digital fashion platforms, AI-driven design systems, and on-demand manufacturing is reshaping production cycles and reducing reliance on mass inventory models.

Increasing regulatory focus on chemical usage, textile waste management, and carbon emissions is influencing production processes and material selection across global supply chains.

E-commerce-driven demand shifts are accelerating product lifecycle changes, requiring faster turnaround times and more flexible manufacturing systems.

Strategic Implications of Risk Factors & Disruption Threats in Global Textile Market

Companies must strengthen supply chain resilience by diversifying sourcing networks and investing in nearshoring or regional manufacturing strategies to reduce geopolitical and logistics risks.

Investment in sustainable materials, recycled fiber technologies, and eco-friendly production processes will be essential to meet tightening environmental regulations and consumer expectations.

Manufacturers and brands should adopt digital manufacturing systems, AI-driven design tools, and automated production technologies to improve efficiency and reduce time-to-market.

Product differentiation through technical textiles, smart fabrics, and high-performance materials will become increasingly important in reducing price-based competition.

Organizations that integrate sustainability, innovation, and agile supply chain management will be better positioned to maintain competitiveness in a rapidly evolving market landscape.

Global Textile Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Textile Market is expected to undergo significant transformation driven by sustainability imperatives, technological innovation, and evolving consumer behavior.

Circular fashion systems, recycled fiber adoption, and sustainable manufacturing practices are expected to become mainstream across global textile production networks.

Technical textiles and smart fabrics will continue expanding across industrial, healthcare, automotive, and wearable technology applications, creating new high-value growth segments.

Digitalization of textile design, manufacturing, and supply chain operations will enhance efficiency, reduce waste, and enable more responsive production systems.

Overall, the market will remain highly competitive and structurally complex, with long-term success determined by sustainability leadership, innovation capability, supply chain agility, and the ability to adapt to rapidly changing global fashion and industrial demand patterns.

Regulatory Landscape

Global Textile Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Textile Market is undergoing significant transformation as governments, environmental agencies, and international trade bodies intensify focus on sustainability, chemical safety, labor standards, and circular economy practices. As textiles remain one of the most resource-intensive industries globally, regulatory frameworks are increasingly aimed at reducing environmental impact across production, consumption, and end-of-life disposal stages.

Textile manufacturers, fiber producers, apparel brands, and supply chain participants must comply with a broad spectrum of regulations covering environmental emissions, chemical usage restrictions, wastewater management, labor compliance, product labeling, and sustainability reporting. With rising demand for sustainable fashion and technical textiles, regulatory oversight is expanding across both traditional textile manufacturing and advanced functional fabric segments.

The rapid growth of e-commerce, fast fashion cycles, and global textile trade is further driving the need for harmonized regulations and stricter compliance standards to ensure environmental protection and ethical production practices.

Global Textile Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by increasing enforcement of environmental protection laws, chemical safety standards, and sustainability-focused textile production guidelines. Governments are implementing stricter controls on dyeing processes, wastewater discharge, and hazardous chemical usage in textile manufacturing.

Chemical regulations such as restrictions on azo dyes, formaldehyde, per- and polyfluoroalkyl substances (PFAS), and other hazardous substances are significantly influencing textile production processes and material selection. Compliance with such standards is becoming essential for market access in developed economies.

Environmental sustainability regulations are also shaping industry behavior, with growing emphasis on carbon footprint reduction, water conservation, and waste minimization across textile supply chains. Many regions are encouraging adoption of recycled fibers, organic cotton, and circular fashion models.

Labor and social compliance regulations continue to play a key role in textile sourcing decisions, particularly in export-oriented manufacturing hubs. International buyers are increasingly enforcing ethical sourcing standards, fair labor practices, and supply chain transparency requirements.

In addition, product labeling and sustainability disclosure requirements are gaining importance, requiring brands to provide transparent information regarding material composition, recyclability, and environmental impact.

Key Regulatory & Policy Environment Signals in Global Textile Market

- Environmental Textile Regulations: Rules governing emissions, wastewater treatment, carbon reduction, and resource efficiency in textile manufacturing.

- Chemical Usage Standards: Restrictions on hazardous substances such as dyes, finishing agents, and industrial chemicals used in textile processing.

- Waste Management & Circular Economy Policies: Regulations promoting textile recycling, reuse, and reduction of landfill waste.

- Labor & Ethical Sourcing Standards: Compliance requirements related to worker safety, fair wages, and ethical manufacturing practices.

- Sustainability Labeling Requirements: Rules governing product transparency, eco-labels, and environmental impact disclosures.

- Trade & Export Compliance Regulations: International standards affecting textile imports, exports, and global supply chain operations.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is driving a structural shift toward sustainable textile production, encouraging companies to adopt cleaner technologies, recycled materials, and environmentally responsible manufacturing processes. Compliance with environmental and chemical regulations is becoming a critical determinant of market access and brand competitiveness.

Chemical restrictions are accelerating innovation in eco-friendly dyes, non-toxic finishing agents, and sustainable fiber alternatives. Companies investing in green chemistry and low-impact production technologies are expected to gain long-term competitive advantages.

Sustainability regulations are pushing the industry toward circular economy models, including textile recycling, fiber regeneration, and waste reduction initiatives. This is creating new business opportunities in recycled fiber production and sustainable fashion ecosystems.

Labor and ethical sourcing regulations are reinforcing supply chain transparency and encouraging global brands to adopt responsible procurement practices. Compliance with these standards is increasingly linked to brand reputation and export eligibility.

Overall, regulatory pressures are reshaping product development strategies, encouraging integration of sustainability metrics into design, manufacturing, and distribution processes across the textile value chain.

Global Textile Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global textile market is expected to become more stringent and globally harmonized, with stronger emphasis on environmental sustainability, circular economy adoption, and chemical safety compliance. Governments are likely to introduce stricter limits on textile waste, emissions, and resource consumption.

Chemical regulations are expected to expand further, with broader restrictions on harmful substances and increased adoption of safer alternatives across textile processing operations. This will accelerate innovation in sustainable materials and green manufacturing technologies.

Circular fashion policies and extended producer responsibility frameworks are anticipated to gain traction, requiring manufacturers and brands to take greater responsibility for textile waste collection, recycling, and lifecycle management.

Sustainability disclosure requirements are expected to become more standardized, requiring companies to provide verified environmental impact data and transparency across supply chains.

Overall, the future regulatory landscape will be defined by the convergence of environmental compliance, chemical safety regulation, circular economy policies, ethical sourcing standards, and global trade requirements. Companies capable of delivering sustainable, compliant, transparent, and innovative textile solutions will be best positioned to capture long-term opportunities in the evolving global textile industry.