Global Consumer Electronics Market Report, Size, Share and Forecast 2026–2033

Global Consumer Electronics Market Forecast Snapshot (2026???2033)

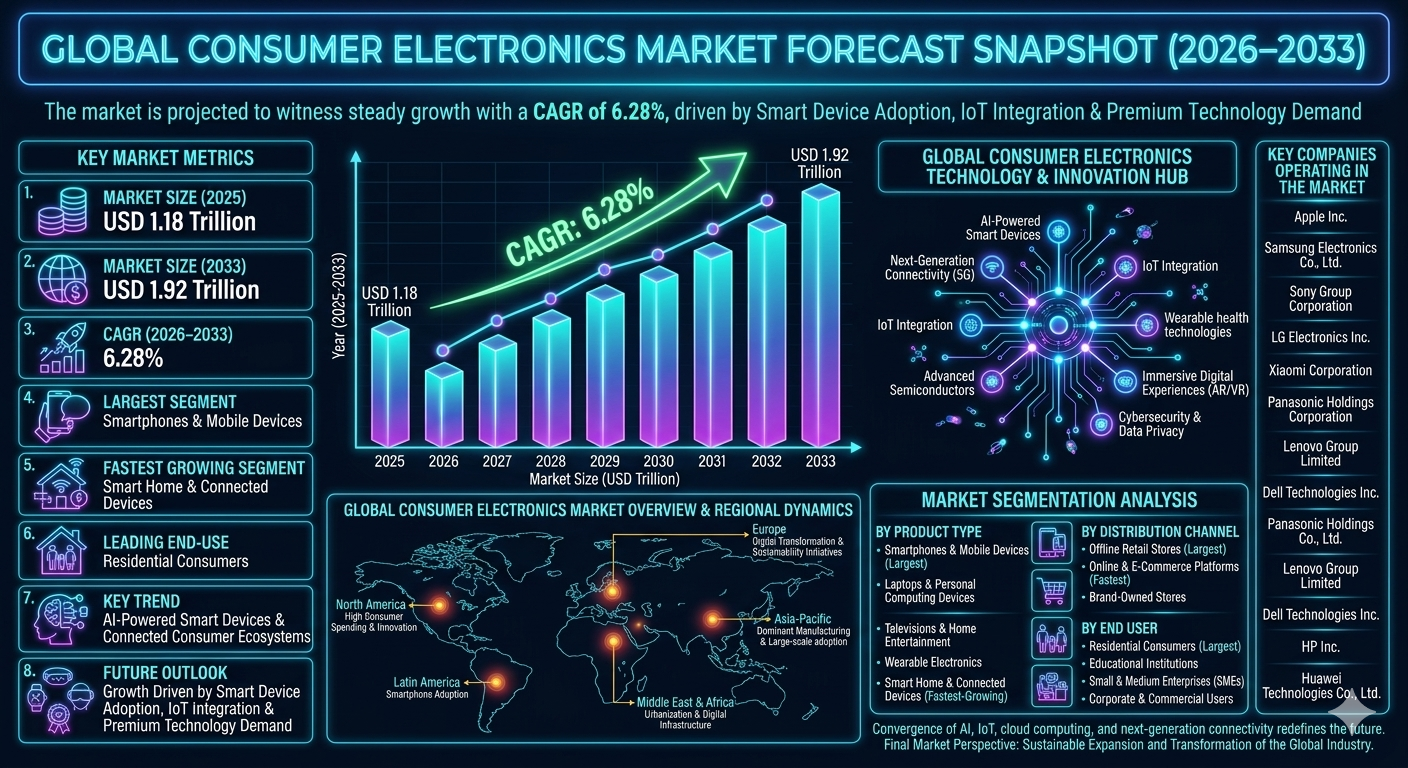

| Metric | Value |

|---|---|

| Market Size (2025) | USD 1.18 Trillion |

| Market Size (2033) | USD 1.92 Trillion |

| CAGR (2026???2033) | 6.28% |

| Largest Segment | Smartphones & Mobile Devices |

| Fastest Growing Segment | Smart Home & Connected Devices |

| Leading End-Use Segment | Residential Consumers |

| Key Trend | AI-Powered Smart Devices & Connected Consumer Ecosystems |

| Regulatory Influence | Electronic Safety Standards, Energy Efficiency Regulations & Data Privacy Requirements |

| Future Outlook | Growth Driven by Smart Device Adoption, IoT Integration & Premium Consumer Technology Demand |

Global Consumer Electronics Market??Size & Forecast

The Global Consumer Electronics Market is expected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at USD 1.18 trillion in 2025 and is projected to reach approximately USD 1.92 trillion by 2033, registering a CAGR of 6.28%. The market growth is primarily driven by rising disposable incomes, increasing digital connectivity, rapid smartphone adoption, growing demand for smart home devices, and continuous technological advancements. Consumer electronics have become integral to modern lifestyles, supporting communication, entertainment, productivity, health monitoring, and home automation. The growing convergence of artificial intelligence, Internet of Things (IoT), and cloud connectivity is accelerating market expansion. In addition, increasing demand for premium devices, wearable technology, and connected home ecosystems is supporting long-term market growth.Global Consumer Electronics Market Overview

Consumer electronics comprise electronic devices designed for everyday personal, household, and entertainment use.These products are widely utilized across communication, entertainment, education, fitness tracking, home automation, and digital lifestyle applications. The market is evolving from standalone electronic devices toward intelligent, connected, and AI-enabled consumer technology ecosystems.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in artificial intelligence, advanced semiconductors, 5G connectivity, augmented reality, wearable technologies, and smart home systems is transforming the consumer electronics landscape. Manufacturers are continuously introducing advanced features, enhanced user experiences, and seamless device interoperability.Market Implications

Companies investing in AI-powered devices, next-generation connectivity, and integrated digital ecosystems are expected to strengthen market leadership.2. Compliance and Risk Repricing

Electronic safety standards, energy efficiency regulations, cybersecurity requirements, and consumer data protection laws are influencing product development and manufacturing practices. Manufacturers are increasingly prioritizing sustainable materials and environmentally responsible production processes.Market Implications

Firms offering compliant, secure, and energy-efficient consumer electronics are likely to gain stronger consumer trust and regulatory approval.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as global technology companies, electronics manufacturers, semiconductor providers, and software firms expand their product portfolios. Vertical integration, direct-to-consumer sales models, and ecosystem-based strategies are reshaping industry value chains.Market Implications

Companies focusing on ecosystem integration, premium experiences, and digital services may gain stronger competitive advantages.4. Capital and Capacity Scaling

Rising investments in semiconductor manufacturing, smart device production, research and development, and digital infrastructure are supporting market expansion. Growing global demand for connected technologies is increasing manufacturing capacity requirements.Market Implications

Manufacturers scaling innovation capabilities and production efficiency are expected to capture future opportunities.Market Segmentation Analysis

By Product Type

1. Smartphones & Mobile Devices

This remains the largest segment due to widespread global adoption and continuous product upgrades.2. Laptops & Personal Computing Devices

Strong demand driven by remote work, education, and digital productivity requirements.3. Televisions & Home Entertainment Systems

Growing adoption of smart TVs and high-definition display technologies.4. Wearable Electronics

Increasing demand for fitness tracking, health monitoring, and connected lifestyle applications.5. Smart Home & Connected Devices

Fastest-growing segment due to expanding IoT ecosystems and home automation adoption.By Distribution Channel

1. Offline Retail Stores

Largest segment due to product demonstration and consumer purchasing preferences.2. Online & E-Commerce Platforms

Fastest-growing channel driven by digital shopping convenience and wider product availability.3. Brand-Owned Stores

Strong demand for premium customer experiences and direct sales strategies.By End User

1. Residential Consumers

Largest segment due to widespread personal and household electronics consumption.2. Educational Institutions

Growing demand for digital learning devices and connected technologies.3. Small & Medium Enterprises (SMEs)

Increasing utilization of computing and communication devices.4. Corporate & Commercial Users

Strong adoption of advanced digital productivity solutions.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global consumer electronics market due to large-scale manufacturing capabilities, growing middle-class populations, and strong technology adoption.North America

North America remains a major market supported by high consumer spending, technological innovation, and premium device adoption.Europe

Europe demonstrates strong demand driven by digital transformation, sustainability initiatives, and advanced consumer technology penetration.Latin America

Latin America is gradually expanding due to increasing smartphone adoption and improving internet connectivity.Middle East & Africa

The region is witnessing growing demand supported by urbanization, rising disposable incomes, and digital infrastructure development.Competitive Landscape

The Global Consumer Electronics Market is highly competitive with multinational technology companies, electronics manufacturers, and digital ecosystem providers operating globally.Key Companies Operating in the Market Include:

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Sony Group Corporation

- LG Electronics Inc.

- Xiaomi Corporation

- Panasonic Holdings Corporation

- Lenovo Group Limited

- Dell Technologies Inc.

- HP Inc.

- Huawei Technologies Co., Ltd.

Strategic Outlook

The future of the consumer electronics market will be shaped by artificial intelligence, IoT-enabled ecosystems, 5G connectivity, immersive digital experiences, and sustainable product innovation. Smart homes, wearable health technologies, cloud-connected devices, and AI-powered personal assistants will significantly improve consumer experiences and operational efficiency. The rise of connected lifestyles, premium electronics demand, and intelligent device ecosystems is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Consumer Electronics Market remains one of the most influential segments within the technology and digital economy ecosystem. Rising digital adoption, smart device penetration, and technological innovation continue driving long-term market growth. Companies capable of delivering innovative, connected, secure, and user-centric consumer technologies will be best positioned to capture future opportunities. The convergence of AI, IoT, cloud computing, and next-generation connectivity is expected to redefine the future of the global consumer electronics industry.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Consumer Electronics Market Snapshot (2026???2033)

- 1.2 Market Size & Growth Overview

- 1.3 Key Market Highlights

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Performance Summary

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Market Introduction & Overview

- 2.1 Definition of Consumer Electronics

- 2.2 Scope of the Global Consumer Electronics Market

- 2.3 Evolution of Connected Consumer Technologies

- 2.4 Consumer Electronics Value Chain Analysis

- 2.5 Regulatory & Compliance Framework

- 2.6 Emerging Trends in Smart Devices & Digital Lifestyles

- 2.7 AI, IoT & Connected Ecosystem Integration

- 3. Research Methodology

- 3.1 Primary Research Approach

- 3.2 Secondary Research Sources

- 3.3 Market Size Estimation Methodology

- 3.4 Forecasting Assumptions (2026???2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Market Drivers

- 4.1.1 Rising Smartphone & Mobile Device Adoption

- 4.1.2 Growing Demand for Smart Home Technologies

- 4.1.3 Increasing Digital Connectivity & Internet Penetration

- 4.1.4 Expansion of Wearable Electronics & Health Monitoring Devices

- 4.1.5 Continuous Innovation in AI, IoT & 5G Technologies

- 4.2 Market Restraints

- 4.2.1 Short Product Replacement Cycles & Market Saturation

- 4.2.2 Supply Chain Disruptions & Semiconductor Shortages

- 4.2.3 Rising Data Privacy & Cybersecurity Concerns

- 4.3 Market Opportunities

- 4.3.1 Expansion of Smart Home & Connected Device Ecosystems

- 4.3.2 Growth of AI-Powered Consumer Electronics

- 4.3.3 Increasing Demand for Premium Consumer Technologies

- 4.3.4 Sustainable & Energy-Efficient Product Development

- 4.4 Market Challenges

- 4.4.1 Intense Competition & Price Pressure

- 4.4.2 Rapid Technological Obsolescence

- 4.4.3 Compliance with Global Safety & Environmental Standards

- 4.1 Market Drivers

- 5. Global Consumer Electronics Market Size & Forecast (USD Trillion), 2026???2033

- 5.1 Market Revenue Analysis

- 5.2 CAGR Analysis

- 5.3 Demand-Supply Trends

- 5.4 Pricing Analysis

- 5.5 Investment Trends

- 5.6 Future Market Outlook

- 6. Market Segmentation Analysis (USD Trillion), 2026???2033

- 6.1 By Product Type

- 6.1.1 Smartphones & Mobile Devices (Largest Segment)

- 6.1.2 Laptops & Personal Computing Devices

- 6.1.3 Televisions & Home Entertainment Systems

- 6.1.4 Wearable Electronics

- 6.1.5 Smart Home & Connected Devices (Fastest-Growing Segment)

- 6.2 By Distribution Channel

- 6.2.1 Offline Retail Stores (Largest Segment)

- 6.2.2 Online & E-Commerce Platforms (Fastest-Growing Segment)

- 6.2.3 Brand-Owned Stores

- 6.3 By End User

- 6.3.1 Residential Consumers (Largest Segment)

- 6.3.2 Educational Institutions

- 6.3.3 Small & Medium Enterprises (SMEs)

- 6.3.4 Corporate & Commercial Users

- 6.1 By Product Type

- 7. Regional Market Analysis

- 7.1 Asia-Pacific

- 7.2 North America

- 7.3 Europe

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Competitive Benchmarking

- 8.3 Strategic Developments

- 8.4 Product Innovation & Ecosystem Expansion Strategies

- 8.5 Mergers, Partnerships & Investment Analysis

- 9. Company Profiles

- 9.1 Apple Inc.

- 9.2 Samsung Electronics Co., Ltd.

- 9.3 Sony Group Corporation

- 9.4 LG Electronics Inc.

- 9.5 Xiaomi Corporation

- 9.6 Panasonic Holdings Corporation

- 9.7 Lenovo Group Limited

- 9.8 Dell Technologies Inc.

- 9.9 HP Inc.

- 9.10 Huawei Technologies Co., Ltd.

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Consumer Electronics Demand Forecast Model

- 10.2 Smart Home Adoption Opportunity Analysis

- 10.3 AI-Powered Device Innovation Tracker

- 10.4 Connected Consumer Ecosystem Assessment

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of AI-Powered Consumer Devices

- 11.2 Investment in Smart Home & IoT Ecosystems

- 11.3 Growth Opportunities in Wearables & Connected Health Technologies

- 11.4 Strengthening Sustainable & Energy-Efficient Product Portfolios

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Market Research

- 14. Disclaimer

Competitive Landscape

Global Consumer Electronics Market Competitive Intensity & Market Structure Overview

The global consumer electronics market is highly competitive and moderately consolidated, dominated by multinational technology companies, consumer device manufacturers, semiconductor innovators, and ecosystem-based digital service providers. Competitive intensity is driven by technological innovation, product differentiation, brand strength, pricing strategies, distribution reach, software integration capabilities, and the ability to deliver seamless connected user experiences.

Market participants are continuously investing in artificial intelligence, advanced semiconductor technologies, Internet of Things (IoT) integration, cloud connectivity, and next-generation user interfaces to strengthen their competitive positions. Competition is particularly intense in smartphones, wearables, smart home devices, and premium consumer technology categories, where rapid innovation cycles influence purchasing decisions.

The market structure is increasingly shifting from standalone hardware products toward integrated digital ecosystems that combine devices, software platforms, cloud services, content offerings, and subscription-based services. This ecosystem-centric approach is becoming a key differentiator among leading market players.

Global Consumer Electronics Market Competitive Intensity & Market Structure Current Scenario

Leading Global Consumer Electronics Companies

Apple Inc.: Global technology leader known for its integrated ecosystem of smartphones, computers, wearables, entertainment services, and software platforms, supported by strong brand loyalty and premium positioning.

Samsung Electronics Co., Ltd.: One of the world’s largest consumer electronics manufacturers with a diversified portfolio spanning smartphones, televisions, home appliances, semiconductors, and connected devices.

Sony Group Corporation: Major player in entertainment electronics, gaming systems, imaging technologies, audio equipment, and premium consumer devices.

LG Electronics Inc.: Leading manufacturer of home appliances, televisions, display technologies, smart home products, and connected consumer electronics solutions.

Xiaomi Corporation: Rapidly growing technology company offering smartphones, IoT devices, smart home products, and connected ecosystem solutions at competitive price points.

Panasonic Holdings Corporation: Diversified electronics manufacturer with strong expertise in consumer electronics, home appliances, audiovisual products, and energy-efficient technologies.

Lenovo Group Limited: Global leader in personal computing devices, laptops, tablets, and enterprise technology solutions with a strong international presence.

Dell Technologies Inc.: Prominent provider of personal computers, gaming systems, and digital productivity devices serving both consumer and commercial markets.

HP Inc.: Leading manufacturer of personal computing devices, printers, and hybrid work technologies with strong global distribution networks.

Huawei Technologies Co., Ltd.: Major technology company offering smartphones, wearable devices, smart home products, and connected digital ecosystem solutions.

Key Competitive Intensity & Market Structure Drivers

Rapid technological advancements in artificial intelligence, 5G connectivity, smart sensors, and advanced semiconductor architectures are intensifying innovation-based competition across consumer electronics categories.

Growing consumer demand for interconnected digital experiences is encouraging manufacturers to develop integrated ecosystems that connect smartphones, wearables, smart homes, entertainment systems, and cloud services.

Product differentiation through design innovation, premium features, energy efficiency, and enhanced user experiences is becoming increasingly important in mature device categories.

The expansion of e-commerce, direct-to-consumer channels, and omnichannel retail strategies is reshaping competitive dynamics and strengthening customer engagement opportunities.

Data privacy requirements, cybersecurity concerns, and sustainability regulations are influencing product development priorities and competitive positioning across global markets.

Strategic Implications of Competitive Intensity & Market Structure

Companies investing in AI-powered devices, proprietary operating systems, and integrated service ecosystems are expected to gain long-term competitive advantages through stronger customer retention and recurring revenue streams.

Vertical integration across hardware, software, semiconductor development, and digital services is becoming an increasingly valuable strategy for improving performance optimization and ecosystem control.

Strong research and development capabilities are essential for maintaining leadership in rapidly evolving product categories such as wearables, smart homes, augmented reality devices, and AI-enabled consumer technologies.

Manufacturers focusing on sustainability initiatives, energy-efficient products, and environmentally responsible supply chains are expected to strengthen brand reputation and regulatory compliance.

Strategic partnerships among device manufacturers, software developers, telecommunications providers, and cloud service companies are accelerating innovation and ecosystem expansion.

Global Consumer Electronics Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global consumer electronics market is expected to become increasingly ecosystem-driven as artificial intelligence, IoT integration, cloud connectivity, and immersive digital technologies continue to transform consumer experiences. Future competition will focus on delivering intelligent, personalized, and seamlessly connected technology environments.

Manufacturers are expected to increase investments in AI-powered assistants, smart home interoperability, advanced wearable technologies, augmented reality applications, and next-generation computing platforms to strengthen market positioning.

Asia-Pacific is expected to remain the dominant manufacturing and consumption hub due to its strong electronics production infrastructure and growing consumer base, while North America and Europe will continue to drive innovation in premium consumer technologies and digital services.

Over the forecast period, companies that successfully combine technological innovation, ecosystem integration, cybersecurity, sustainability, and superior customer experiences will be best positioned to strengthen their leadership within the evolving global consumer electronics market.

Value Chain

Global Consumer Electronics Market Value Chain & Supply Chain Evolution Overview

The Global Consumer Electronics Market is undergoing continuous transformation driven by rapid technological innovation, increasing digital connectivity, expanding smart device adoption, and the emergence of AI-powered consumer ecosystems. The market???s value chain is characterized by a globally interconnected network of semiconductor suppliers, component manufacturers, device assemblers, software developers, logistics providers, retailers, and digital service platforms. This integrated ecosystem is reshaping how consumer electronics are designed, manufactured, distributed, and experienced worldwide.

A defining feature of the value chain is the convergence of hardware, software, artificial intelligence, cloud computing, and Internet of Things (IoT) technologies. Modern consumer electronics are increasingly evolving from standalone devices into connected ecosystems that enable seamless interoperability across smartphones, wearables, smart home products, entertainment systems, and cloud-based digital services.

Supply chain complexity remains high due to global sourcing of semiconductors, displays, sensors, batteries, electronic components, software integration requirements, and evolving regulatory standards. Manufacturers must coordinate across component suppliers, contract manufacturers, logistics networks, technology partners, and retail channels while maintaining product quality, innovation speed, and operational efficiency.

Industry participants are investing heavily in semiconductor innovation, AI integration, advanced manufacturing automation, cloud connectivity, and sustainable production practices to strengthen competitiveness. The value chain is evolving into a highly connected, data-driven, and consumer-centric ecosystem focused on intelligent experiences, ecosystem integration, and digital lifestyle enablement.

Global Consumer Electronics Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Materials & Electronic Components: Semiconductors, processors, memory chips, displays, sensors, batteries, camera modules, connectivity components, and electronic materials.

- Device Design & Product Development: Industrial design, hardware engineering, software development, operating systems, AI integration, and user experience optimization.

- Manufacturing & Assembly: Component fabrication, electronics assembly, quality assurance testing, contract manufacturing, and production automation.

- Software & Ecosystem Integration: Cloud services, IoT connectivity, AI-powered applications, digital content ecosystems, cybersecurity solutions, and device interoperability platforms.

- Distribution & Retail Channels: Offline retail stores, e-commerce platforms, telecom operators, distributors, wholesalers, and brand-owned stores.

- End-User Consumption: Residential consumers, educational institutions, SMEs, enterprises, digital content users, and smart home adopters.

Company-to-Stage Mapping

- Raw Materials & Electronic Components: Semiconductor manufacturers, battery suppliers, display manufacturers, sensor producers, and electronic component providers.

- Device Design & Product Development: Apple Inc., Samsung Electronics Co., Ltd., Sony Group Corporation, Huawei Technologies Co., Ltd., Xiaomi Corporation.

- Manufacturing & Assembly: Samsung Electronics Co., Ltd., LG Electronics Inc., Lenovo Group Limited, HP Inc., Dell Technologies Inc., global electronics manufacturing partners.

- Software & Ecosystem Integration: Apple Inc., Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., cloud platform providers, AI technology developers, and software ecosystem partners.

- Distribution & Retail Channels: E-commerce platforms, consumer electronics retailers, telecom operators, distributors, and company-owned retail stores.

- End-User Consumption: Consumers, businesses, educational institutions, smart home users, gamers, and digital content subscribers.

Key Value Chain & Supply Chain Evolution Signals in Global Consumer Electronics Market

- Expansion of AI-Powered Consumer Devices:

Artificial intelligence is enhancing personalization, automation, voice interaction, productivity, and user experience across multiple device categories. - Growth of Smart Home & Connected Ecosystems:

Increasing interoperability among connected devices is driving ecosystem-based product strategies. - Advancement of Semiconductor Technologies:

Next-generation processors and chip architectures are improving device performance, energy efficiency, and AI capabilities. - Rise of Cloud-Connected Consumer Experiences:

Cloud services are enabling seamless synchronization, digital content access, and cross-device functionality. - Increasing Focus on Sustainable Electronics Manufacturing:

Manufacturers are adopting recyclable materials, energy-efficient production methods, and circular economy initiatives. - Expansion of Direct-to-Consumer & Digital Retail Models:

Online platforms and omnichannel retail strategies are enhancing customer engagement and market reach.

Strategic Implications of Value Chain & Supply Chain Evolution

- Investment in AI & Ecosystem Integration:

Connected ecosystems and intelligent device experiences are becoming major competitive differentiators. - Strengthening Semiconductor Supply Chain Resilience:

Diversified sourcing and advanced chip development capabilities are critical for long-term growth. - Expansion of Smart Home & IoT Platforms:

Integrated consumer ecosystems create opportunities for recurring services and enhanced customer loyalty. - Optimization of Global Manufacturing Networks:

Flexible production models improve responsiveness to market demand and supply chain disruptions. - Enhancement of Sustainability & Circular Economy Programs:

Recycling initiatives and energy-efficient products support regulatory compliance and brand reputation. - Development of Omnichannel Retail Strategies:

Combining physical and digital channels improves customer experience and sales performance.

Global Consumer Electronics Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the consumer electronics value chain is expected to evolve into a highly intelligent, interconnected, and service-oriented ecosystem powered by AI, IoT, cloud computing, and next-generation connectivity technologies.

Key Future Developments Include:

- Expansion of AI-powered personal devices and intelligent digital assistants.

- Increased adoption of smart home ecosystems and connected consumer environments.

- Growth of cloud-based digital services integrated with consumer devices.

- Advancement of wearable health monitoring and fitness technologies.

- Expansion of sustainable manufacturing and circular electronics initiatives.

- Strengthening of next-generation semiconductor innovation and edge computing capabilities.

As the market evolves, competitive advantage will increasingly depend on the ability to combine technological innovation, ecosystem connectivity, product reliability, cybersecurity, and consumer-centric design. Organizations capable of delivering seamless, intelligent, and connected experiences will be best positioned to capture future growth opportunities.

Companies that successfully integrate AI capabilities, cloud ecosystems, IoT connectivity, advanced semiconductor technologies, and sustainable manufacturing practices will achieve stronger customer engagement, operational scalability, and long-term leadership in the Global Consumer Electronics Market.

Investment Activity

Global Consumer Electronics Market Investment & Funding Dynamics Overview

The Global Consumer Electronics Market is witnessing substantial investment activity driven by accelerating digital transformation, rising consumer demand for connected devices, rapid advancements in artificial intelligence, and the growing adoption of smart home ecosystems. Technology companies, electronics manufacturers, semiconductor suppliers, software developers, and private investors are actively investing in AI-powered devices, smart home platforms, advanced semiconductor technologies, connected consumer ecosystems, and next-generation product innovation.

Investment momentum is increasing as consumers seek enhanced digital experiences across communication, entertainment, productivity, health monitoring, and home automation applications. Market participants are allocating capital toward 5G-enabled devices, wearable technologies, intelligent personal assistants, cloud-connected electronics, and immersive digital experience platforms.

Additionally, growing investments in advanced chip manufacturing, IoT infrastructure, augmented reality technologies, sustainable electronics production, and energy-efficient device development are strengthening long-term growth opportunities across the global consumer electronics ecosystem.

Global Consumer Electronics Market Investment & Funding Dynamics Current Scenario

Currently, the consumer electronics market is experiencing strong capital deployment as manufacturers expand product portfolios and strengthen innovation capabilities. Leading industry participants are investing heavily in AI-driven consumer devices, smart home integration technologies, wearable health monitoring systems, premium smartphone development, and connected entertainment platforms.

The market is attracting significant funding into consumer technology startups, semiconductor companies, smart device innovators, wearable technology developers, and IoT solution providers. Venture capital firms, corporate investors, and strategic technology funds are increasingly supporting innovations that enhance connectivity, personalization, and user engagement.

Furthermore, the industry is witnessing active mergers, acquisitions, strategic partnerships, and ecosystem collaborations as technology companies seek to expand capabilities, improve interoperability, and strengthen market positioning.

Key Investment & Funding Dynamics Signals in Global Consumer Electronics Market

- Growing demand for AI-powered smart devices and intelligent consumer experiences is accelerating technology-focused investments.

- Expansion of smart home ecosystems and connected living environments is increasing capital deployment across IoT technologies.

- Rising adoption of wearable electronics and digital health monitoring devices is supporting product innovation investments.

- Strategic investments in advanced semiconductor manufacturing and next-generation connectivity solutions are strengthening supply chain resilience.

- Increasing consumer demand for premium devices and immersive entertainment experiences is driving R&D spending.

- Partnerships between electronics manufacturers, software developers, cloud service providers, and semiconductor companies are improving ecosystem integration.

- Growing emphasis on energy efficiency, sustainability, and environmentally responsible electronics production is influencing long-term investment strategies.

Strategic Implications of Investment & Funding Dynamics in Global Consumer Electronics Market

- Continuous investment in artificial intelligence, IoT integration, and smart device innovation is essential for maintaining market competitiveness.

- Capital allocation toward semiconductor development, cloud connectivity, and advanced consumer experiences will strengthen long-term growth potential.

- Companies offering connected, secure, and user-centric consumer electronics ecosystems are expected to achieve stronger market share.

- Strategic acquisitions and partnerships will accelerate technology convergence, ecosystem expansion, and product diversification.

- Investments in wearable technologies, smart home automation, and AI-enabled consumer platforms will remain major growth priorities.

- Compliance with electronic safety standards, energy efficiency regulations, and data privacy requirements will continue shaping investment decisions.

- Organizations developing integrated digital ecosystems and intelligent connected devices are expected to capture substantial future opportunities.

Global Consumer Electronics Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Consumer Electronics Market is expected to maintain strong investment growth driven by increasing smart device adoption, expanding IoT ecosystems, advances in AI technologies, and rising demand for premium digital experiences.

Future capital deployment will increasingly focus on AI-powered consumer assistants, next-generation wearable devices, immersive AR/VR technologies, advanced smart home platforms, sustainable electronics manufacturing, and cloud-connected digital ecosystems.

As consumers continue embracing connected lifestyles and intelligent technologies, investment activity is expected to expand across semiconductor innovation, device interoperability, digital health technologies, and next-generation consumer experience platforms.

In conclusion, the Global Consumer Electronics Market represents a large-scale technology investment landscape where artificial intelligence, IoT connectivity, semiconductor innovation, smart ecosystems, and sustainable product development will define future funding priorities, competitive strategies, and long-term industry growth.

Technology & Innovation

Global Consumer Electronics Market Technology & Innovation Landscape Overview

The global consumer electronics market is undergoing rapid technological transformation driven by advancements in artificial intelligence (AI), Internet of Things (IoT), 5G connectivity, advanced semiconductor technologies, cloud computing, augmented reality (AR), virtual reality (VR), and smart device ecosystems. These innovations are fundamentally reshaping how consumers interact with technology across communication, entertainment, productivity, health, and home automation applications.

Modern consumer electronics increasingly integrate AI-powered processors, edge computing capabilities, voice-enabled assistants, connected device ecosystems, biometric authentication systems, and intelligent automation features to deliver seamless, personalized, and highly connected user experiences. These advancements are enabling the transition from standalone devices toward fully integrated digital lifestyles.

The market is also witnessing strong adoption of smart home platforms, wearable health technologies, immersive entertainment systems, cloud-connected devices, and energy-efficient electronic designs, which are enhancing convenience, functionality, and sustainability across consumer applications.

Global Consumer Electronics Market Technology & Innovation Current Scenario

Current innovation in the consumer electronics market is primarily centered around AI-driven user experiences, smart connectivity, and ecosystem integration. Manufacturers are increasingly focusing on creating interconnected product portfolios that enhance convenience, productivity, and digital engagement.

Artificial intelligence technologies are being widely incorporated into smartphones, wearables, smart televisions, and home appliances to enable predictive functionality, personalized recommendations, voice interaction, and automated decision-making.

5G-enabled devices and connectivity solutions are accelerating real-time communication, cloud gaming, video streaming, and connected device performance across multiple consumer environments.

Smart home ecosystems are expanding rapidly through the integration of connected appliances, intelligent security systems, voice-controlled assistants, and automated energy management platforms.

Wearable electronics are evolving beyond fitness tracking to support advanced health monitoring, biometric sensing, sleep analysis, and preventive healthcare applications.

Additionally, manufacturers are investing heavily in sustainable materials, energy-efficient components, recyclable product designs, and environmentally responsible manufacturing processes to align with global sustainability goals.

Key Technology & Innovation Trends in Global Consumer Electronics Market

- AI-Powered Consumer Devices: Intelligent personalization, voice assistants, and predictive user experiences.

- IoT-Connected Ecosystems: Seamless communication between smartphones, wearables, home devices, and appliances.

- 5G Connectivity Integration: Enhanced speed, low-latency communication, and real-time digital experiences.

- Smart Home Automation: Connected lighting, security systems, appliances, and energy management platforms.

- Wearable Health Technologies: Advanced biometric monitoring, fitness tracking, and digital healthcare integration.

- AR & VR Experiences: Immersive gaming, entertainment, education, and virtual collaboration applications.

- Advanced Semiconductor Innovation: High-performance processors supporting AI, graphics, and energy efficiency.

- Cloud-Connected Devices: Real-time synchronization, storage, and cross-device functionality.

- Biometric Security Technologies: Facial recognition, fingerprint authentication, and secure digital access systems.

- Sustainable Electronics Design: Energy-efficient products, recyclable materials, and eco-friendly manufacturing practices.

Strategic Implications of Technology & Innovation

Technological advancements are transforming the consumer electronics industry into a highly connected, intelligent, and experience-driven ecosystem where interoperability and personalization are becoming key competitive differentiators.

Companies investing in AI-enabled devices, smart ecosystem development, and next-generation connectivity technologies are gaining stronger market positioning through enhanced customer engagement and long-term brand loyalty.

The convergence of AI, IoT, cloud computing, and advanced semiconductor technologies is enabling seamless integration between devices while creating new opportunities for subscription-based services and digital ecosystems.

Automation, predictive intelligence, and connected device management are improving user convenience while enabling manufacturers to gather insights for continuous product enhancement.

However, cybersecurity concerns, data privacy challenges, semiconductor supply chain volatility, and increasing regulatory requirements remain significant challenges for industry participants.

Global Consumer Electronics Market Technology & Innovation Forward Outlook

The future of the consumer electronics market is expected to evolve toward fully intelligent, AI-driven, and interconnected digital ecosystems supported by advanced connectivity, edge computing, and next-generation semiconductor technologies.

Emerging innovations include AI-powered personal assistants, smart ambient computing environments, advanced wearable healthcare platforms, immersive mixed reality devices, and autonomous connected home ecosystems.

Consumer demand for personalized experiences, intelligent automation, and seamless cross-device integration is expected to accelerate significantly as technology ecosystems become more sophisticated.

The integration of AI, cloud infrastructure, and IoT-enabled platforms will further enhance productivity, entertainment, health monitoring, and smart living experiences across households worldwide.

Overall, the global consumer electronics market is evolving into a highly connected, data-driven, and intelligent ecosystem where AI, IoT, 5G, cloud computing, and immersive technologies collectively redefine the future of consumer technology and digital lifestyles.

Market Risk

Global Consumer Electronics Market Risk Factors & Disruption Threats Overview

The global consumer electronics market operates within a highly competitive and rapidly evolving environment characterized by technological disruption, supply chain complexity, changing consumer preferences, and regulatory scrutiny. While demand for smartphones, smart home devices, wearable technologies, and connected consumer ecosystems continues to expand, the industry remains exposed to significant operational, financial, and geopolitical risks.

The market’s growth trajectory is heavily dependent on continuous innovation cycles, semiconductor availability, global manufacturing networks, and consumer purchasing power. As product lifecycles become shorter and technological advancements accelerate, manufacturers face increasing pressure to maintain innovation leadership while managing rising production costs and margin constraints.

Additionally, the growing integration of artificial intelligence, cloud connectivity, and IoT-enabled devices introduces new cybersecurity, data privacy, and regulatory compliance challenges. As connected devices become central to consumer lifestyles, ensuring secure and reliable digital ecosystems has become a critical strategic priority across the industry.

Global Consumer Electronics Market Risk Factors & Disruption Threats Current Scenario

The current market environment is shaped by ongoing supply chain adjustments, semiconductor availability concerns, inflationary pressures, and increasing regulatory oversight. Although demand for premium electronics, smart devices, and connected technologies remains strong, manufacturers continue to face challenges related to component sourcing, logistics costs, and inventory management.

Semiconductor dependency remains one of the industry’s most significant vulnerabilities. Advanced chips are essential for smartphones, wearables, smart home devices, gaming systems, and AI-enabled electronics. Any disruption in semiconductor production can lead to product shortages, delayed launches, and increased manufacturing costs.

The market is also experiencing heightened cybersecurity and privacy concerns. Connected devices continuously collect and process consumer data, increasing exposure to data breaches, unauthorized access, and regulatory investigations. Compliance with data protection frameworks such as GDPR, CCPA, and emerging global privacy regulations is becoming increasingly complex.

Furthermore, inflationary pressures and economic uncertainty may influence consumer spending patterns, particularly within discretionary electronics categories. Premium devices may experience slower upgrade cycles during periods of economic stress, impacting revenue growth across certain product segments.

Key Risk Factors & Disruption Threats Signals in the Consumer Electronics Market

- Semiconductor Supply Constraints: Dependence on advanced chip manufacturing creates exposure to shortages, production delays, and component cost inflation.

- Geopolitical Tensions and Trade Restrictions: Export controls, tariffs, and international trade disputes can disrupt manufacturing networks and global distribution channels.

- Cybersecurity Vulnerabilities: Connected devices face increasing risks from hacking, malware attacks, and unauthorized access to consumer data.

- Data Privacy Compliance Risks: Expanding privacy regulations increase compliance costs and legal exposure for device manufacturers and ecosystem providers.

- Rapid Technology Obsolescence: Short product lifecycles require continuous innovation and frequent investment in research and development.

- Consumer Spending Volatility: Economic downturns, inflation, and reduced discretionary income can delay device replacement cycles.

- Supply Chain Concentration: Heavy reliance on specific manufacturing hubs increases vulnerability to disruptions from natural disasters, labor shortages, and geopolitical events.

- E-Waste and Sustainability Pressures: Growing regulatory focus on recycling, repairability, and environmental responsibility may increase operational costs.

- Intense Competitive Pressure: Market saturation in mature categories such as smartphones and laptops intensifies pricing competition and margin compression.

- Counterfeit and Grey Market Products: Unauthorized products can undermine brand reputation, revenue generation, and consumer trust.

Strategic Implications of Risk Factors & Disruption Threats in the Consumer Electronics Market

Consumer electronics companies are increasingly focusing on supply chain diversification, strategic semiconductor partnerships, and localized manufacturing investments to reduce exposure to geopolitical and operational disruptions. Building resilient sourcing networks has become a critical component of long-term business continuity planning.

Cybersecurity and privacy protection are emerging as major competitive differentiators. Manufacturers are investing heavily in device-level security, encrypted communications, cloud protection frameworks, and AI-powered threat detection systems to strengthen consumer trust and regulatory compliance.

Sustainability is also becoming a strategic priority. Leading companies are implementing circular economy initiatives, increasing the use of recycled materials, extending product repairability, and reducing carbon emissions throughout manufacturing operations to meet evolving environmental requirements.

Furthermore, ecosystem-based business models are reshaping competitive dynamics. Companies are increasingly integrating hardware, software, cloud services, subscriptions, and AI capabilities into unified consumer experiences that improve customer retention and recurring revenue opportunities.

Global Consumer Electronics Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead, the consumer electronics market is expected to maintain steady growth as digital lifestyles, smart homes, AI-enabled devices, and connected ecosystems become increasingly mainstream. However, market participants will need to navigate a more complex risk environment characterized by technological, regulatory, and geopolitical uncertainties.

Artificial intelligence integration will create substantial growth opportunities while simultaneously increasing compliance and security requirements. As AI-powered consumer devices become more sophisticated, regulatory scrutiny surrounding algorithm transparency, data usage, and ethical AI deployment is expected to intensify.

Semiconductor supply resilience will remain a strategic focus for both governments and manufacturers. Ongoing investments in domestic chip production and diversified sourcing strategies are expected to reduce long-term supply vulnerabilities, although regional concentration risks may persist.

Sustainability regulations are likely to become more stringent, particularly regarding product lifecycle management, electronic waste reduction, and energy efficiency standards. Companies that proactively align with environmental objectives will be better positioned to maintain market access and strengthen brand value.

Overall, the global consumer electronics market will continue to benefit from innovation-driven demand and expanding digital connectivity. Organizations that successfully manage supply chain risks, cybersecurity threats, regulatory obligations, and sustainability expectations while maintaining strong innovation pipelines will be best positioned to achieve long-term competitive advantage and sustainable growth.

Regulatory Landscape

Global Consumer Electronics Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Consumer Electronics Market is centered on product safety, energy efficiency, cybersecurity, environmental sustainability, and consumer data protection. Governments and regulatory authorities worldwide are implementing comprehensive frameworks to ensure that consumer electronic devices meet safety requirements, reduce environmental impact, and safeguard user information in an increasingly connected digital ecosystem.

Consumer electronics manufacturers must comply with a broad range of regulations covering electrical safety certification, electromagnetic compatibility, hazardous substance restrictions, battery safety standards, wireless communication approvals, and recycling obligations. These regulatory requirements significantly influence product design, manufacturing processes, market entry strategies, and supply chain operations.

As smart devices, IoT-enabled products, and AI-powered consumer technologies become more prevalent, policymakers are also strengthening cybersecurity and privacy regulations to address emerging risks associated with connected devices and digital services.

Global Consumer Electronics Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by increasing enforcement of electronic safety standards and environmental compliance requirements. Regulatory frameworks such as RoHS (Restriction of Hazardous Substances), WEEE (Waste Electrical and Electronic Equipment), and various energy efficiency labeling programs are shaping product development and lifecycle management practices across the industry.

Manufacturers are required to obtain safety certifications and comply with national and regional standards before launching products into commercial markets. Regulatory authorities continue to monitor product quality, battery performance, wireless communication safety, and electromagnetic interference to ensure consumer protection.

Cybersecurity regulations are gaining importance due to the rapid expansion of smart home devices, connected appliances, wearable electronics, and AI-enabled consumer products. Governments are introducing requirements for secure software development, vulnerability management, and consumer data protection.

Environmental regulations are encouraging manufacturers to reduce electronic waste, improve product recyclability, utilize sustainable materials, and minimize carbon emissions throughout production and distribution processes.

Additionally, data privacy laws are influencing how consumer electronics companies collect, process, store, and manage user information, particularly in products integrated with cloud platforms, AI systems, and connected ecosystems.

Key Regulatory & Policy Environment Signals in Global Consumer Electronics Market

- Electronic Product Safety Standards: Mandatory compliance with electrical safety, performance testing, and consumer protection requirements.

- Energy Efficiency Regulations: Growing adoption of energy labeling programs and power consumption standards for electronic devices.

- RoHS & Hazardous Substance Restrictions: Regulations limiting the use of hazardous materials in electronic manufacturing.

- E-Waste & Recycling Requirements: Expanded producer responsibility and electronic waste management obligations.

- Cybersecurity & Connected Device Regulations: Increasing security standards for smart devices, IoT products, and connected ecosystems.

- Consumer Data Privacy Laws: Enhanced requirements governing personal data collection, storage, processing, and user consent.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging consumer electronics manufacturers to incorporate compliance, sustainability, and cybersecurity considerations into product development strategies from the earliest design stages. Regulatory readiness is increasingly becoming a critical factor for global market success.

Environmental compliance requirements are accelerating investments in recyclable materials, energy-efficient components, sustainable packaging, and circular economy initiatives. Companies that proactively address sustainability goals are likely to strengthen brand reputation and regulatory acceptance.

Cybersecurity and privacy regulations are driving greater investment in secure device architectures, encrypted communications, software update frameworks, and cloud security capabilities, particularly for connected consumer electronics products.

Supply chain regulations are encouraging greater transparency, responsible sourcing, and traceability programs to address environmental, ethical, and operational risks across global manufacturing networks.

Overall, regulatory compliance is influencing innovation priorities, production costs, technology investments, and international expansion strategies throughout the consumer electronics industry.

Global Consumer Electronics Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory framework for the global consumer electronics market is expected to become more comprehensive, with stronger emphasis on sustainability, cybersecurity, energy efficiency, and digital consumer protection.

Governments are likely to expand right-to-repair legislation, product durability requirements, and circular economy policies aimed at reducing electronic waste and extending product lifecycles.

Cybersecurity standards for smart devices and connected consumer products are expected to become more stringent, including mandatory security certifications, vulnerability disclosure requirements, and continuous software support obligations.

Environmental regulations will likely increase pressure on manufacturers to reduce carbon emissions, improve resource efficiency, utilize recycled materials, and disclose sustainability performance metrics across their operations.

Overall, the future regulatory environment will favor companies capable of delivering safe, secure, energy-efficient, environmentally responsible, and privacy-focused consumer electronics while maintaining compliance across increasingly complex global regulatory frameworks.