Global Automotive Collision Repair Market Report, Size, Share and Forecast 2026–2033

Global Automotive Collision Repair Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

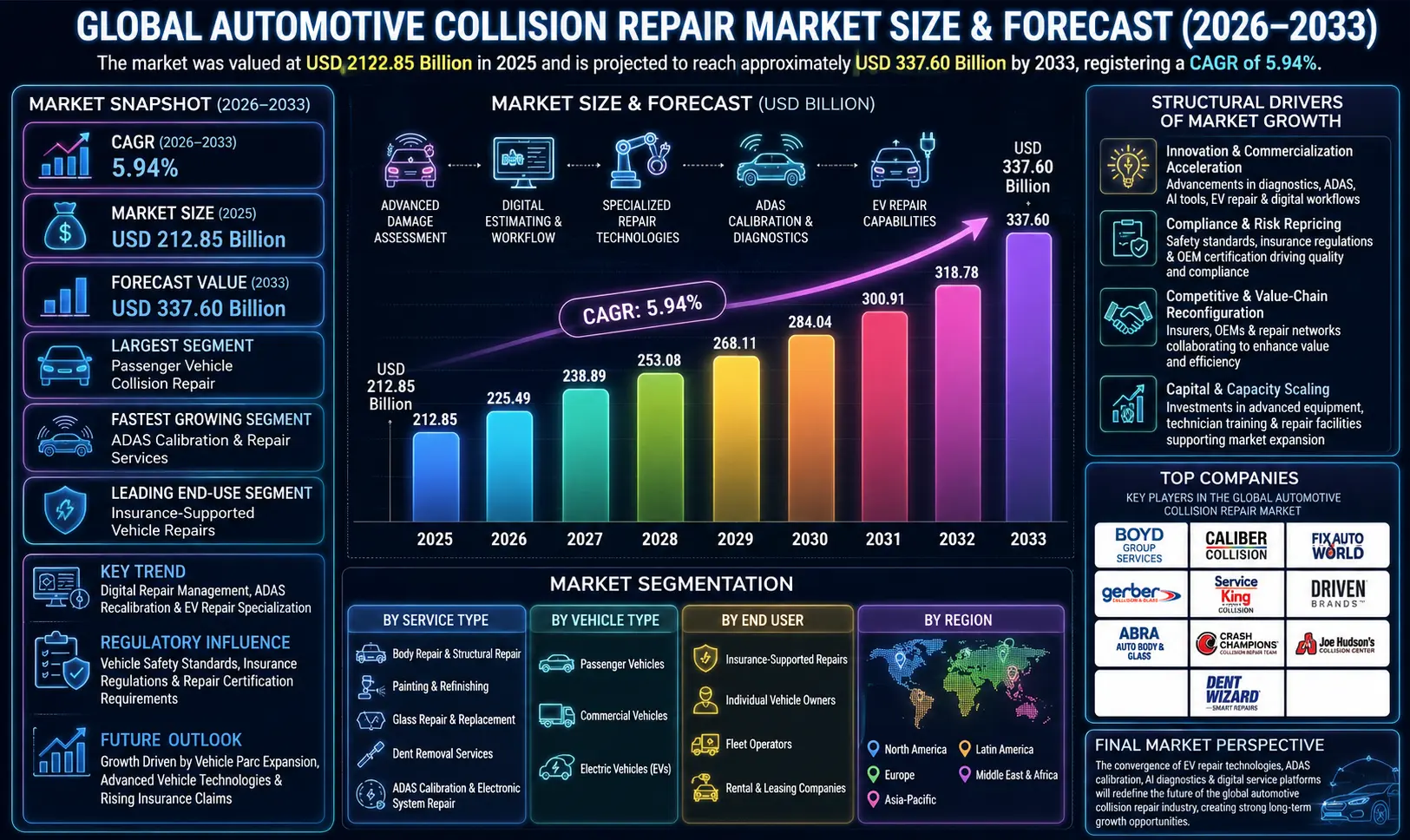

| Market Size (2025) | USD 212.85 Billion |

| Market Size (2033) | USD 337.60 Billion |

| CAGR (2026???2033) | 5.94% |

| Largest Segment | Passenger Vehicle Collision Repair |

| Fastest Growing Segment | Advanced Driver Assistance System (ADAS) Calibration & Repair Services |

| Leading End-Use Segment | Insurance-Supported Vehicle Repairs |

| Key Trend | Digital Repair Management, ADAS Recalibration & EV Repair Specialization |

| Regulatory Influence | Vehicle Safety Standards, Insurance Regulations & Repair Certification Requirements |

| Future Outlook | Growth Driven by Vehicle Parc Expansion, Advanced Vehicle Technologies & Rising Insurance Claims |

Global Automotive Collision Repair Market Size & Forecast

The Global Automotive Collision Repair Market is expected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at USD 212.85 billion in 2025 and is projected to reach approximately USD 337.60 billion by 2033, registering a CAGR of 5.94%. The market growth is primarily driven by increasing vehicle ownership, rising road traffic accidents, growing insurance penetration, and the increasing complexity of modern vehicle repair requirements. Automotive collision repair services play a critical role in restoring vehicle safety, functionality, and appearance following accidents, structural damage, and component failures. In addition, rising adoption of electric vehicles (EVs), advanced driver assistance systems (ADAS), and connected vehicle technologies is creating new opportunities for specialized repair services.Global Automotive Collision Repair Market Overview

Automotive collision repair refers to the repair, restoration, and refinishing of vehicles damaged due to accidents, collisions, environmental events, or structural impacts. The market includes body repair services, painting and refinishing, dent removal, glass replacement, frame straightening, ADAS calibration, mechanical repairs, and EV-specific collision repair solutions. Collision repair services are widely utilized by vehicle owners, insurance companies, fleet operators, rental companies, and automotive dealerships. The market is evolving toward digital repair workflows, AI-based damage assessment, automated estimating systems, and advanced repair technologies for connected and electric vehicles.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Advancements in vehicle materials, digital diagnostics, automated damage assessment tools, and ADAS technologies are transforming collision repair operations. Repair centers are increasingly adopting advanced calibration equipment, AI-powered inspection systems, and specialized EV repair capabilities.Market Implications

Companies investing in advanced repair technologies, technician training, and EV repair infrastructure are expected to strengthen market leadership.2. Compliance and Risk Repricing

Vehicle safety standards, insurance regulations, repair quality requirements, and OEM certification programs are influencing market modernization. Regulators and insurers are emphasizing repair quality, safety compliance, and proper recalibration of advanced vehicle systems.Market Implications

Firms offering certified, compliant, and technologically advanced repair services are likely to gain stronger customer trust and insurance partnerships.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as independent repair shops, dealership service centers, franchise repair networks, and OEM-certified facilities expand service offerings. Strategic collaborations among insurers, automakers, technology providers, and repair networks are reshaping value-chain economics.Market Implications

Companies focusing on service quality, digital transformation, and specialized vehicle repair capabilities may achieve stronger market positioning.4. Capital and Capacity Scaling

Rising investments in repair automation, technician certification programs, EV repair facilities, and advanced diagnostic equipment are supporting market expansion. Growing vehicle parc and increasing repair complexity continue driving industry demand.Market Implications

Organizations scaling technical expertise, repair infrastructure, and service networks are expected to capture future opportunities.Market Segmentation Analysis

By Service Type

1. Body Repair & Structural Repair

This remains the largest segment due to high demand following vehicle collisions and accident-related damage.2. Painting & Refinishing

Strong demand driven by cosmetic restoration and vehicle appearance enhancement.3. Glass Repair & Replacement

Growing adoption due to increasing windshield and sensor-integrated glass replacement needs.4. Dent Removal Services

Widely utilized for minor collision and environmental damage repairs.5. ADAS Calibration & Electronic System Repair

Fastest-growing segment due to increasing integration of advanced safety and driver assistance systems.By Vehicle Type

1. Passenger Vehicles

Largest segment due to high global vehicle ownership and accident frequency.2. Commercial Vehicles

Strong demand from logistics, transportation, and fleet management operators.3. Electric Vehicles (EVs)

Fastest-growing segment driven by expanding EV adoption and specialized repair requirements.By End User

1. Insurance-Supported Repairs

Largest segment due to widespread insurance claim settlements and repair network partnerships.2. Individual Vehicle Owners

Significant demand for out-of-pocket repair and restoration services.3. Fleet Operators

Growing adoption due to vehicle maintenance and operational continuity requirements.4. Rental & Leasing Companies

Strong utilization for vehicle refurbishment and fleet maintenance.Regional Market Dynamics

North America

North America dominates the global automotive collision repair market due to high vehicle ownership, advanced insurance infrastructure, and strong presence of organized repair networks.Europe

Europe remains a major market supported by stringent vehicle safety standards, growing EV adoption, and increasing demand for certified repair services.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rising vehicle sales, expanding automotive fleets, increasing urbanization, and growing insurance penetration.Latin America

Latin America is witnessing gradual expansion due to increasing vehicle ownership and improving automotive service infrastructure.Middle East & Africa

The region is experiencing emerging growth supported by expanding transportation networks, vehicle imports, and increasing accident repair demand.Competitive Landscape

The Global Automotive Collision Repair Market is highly competitive with independent repair shops, OEM-certified centers, franchise networks, and automotive service providers competing globally.Key Companies Operating in the Market Include:

- Boyd Group Services Inc.

- Caliber Holdings LLC

- Fix Auto World

- Gerber Collision & Glass

- Service King Collision

- Driven Brands Holdings Inc.

- ABRA Auto Body Repair

- Crash Champions

- Joe Hudson's Collision Center

- Dent Wizard International

Strategic Outlook

The future of the automotive collision repair market will be shaped by EV repair specialization, ADAS calibration services, AI-driven damage assessment, and digital repair management platforms. Predictive diagnostics, automated estimating systems, connected repair ecosystems, and OEM-certified repair standards will significantly improve operational efficiency and service quality. The rise of electric vehicles, advanced safety technologies, and insurer-repairer collaborations is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Automotive Collision Repair Market remains a vital component of the automotive aftermarket ecosystem. Rising vehicle ownership, technological advancements, and increasing demand for safe and efficient repair solutions continue driving long-term market growth. Companies capable of delivering scalable, technology-enabled, certified, and customer-centric repair services will be best positioned to capture future opportunities. The convergence of EV repair technologies, AI diagnostics, ADAS calibration, and digital service platforms is expected to redefine the future of the global automotive collision repair industry.Table of Contents

Table of Contents

- Executive Summary

- Global Automotive Collision Repair Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends & Digital Repair Transformation

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Automotive Collision Repair Services

- Scope of the Global Automotive Collision Repair Market

- Evolution of Vehicle Repair & Restoration Technologies

- Role of Collision Repair in the Automotive Aftermarket Ecosystem

- Value Chain Analysis of Automotive Collision Repair Services

- Regulatory Influence (Vehicle Safety Standards, Insurance Regulations & Repair Certification Requirements)

- Transition Toward Digital Repair Management, ADAS Calibration & EV Repair Solutions

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Innovation and Commercialization Acceleration in Vehicle Repair Technologies

- Compliance and Risk Repricing in Vehicle Safety & Insurance Markets

- Competitive and Value-Chain Reconfiguration Across Repair Networks

- Capital and Capacity Scaling in Advanced Repair Infrastructure

- Market Restraints

- High Cost of Advanced Repair Equipment & Technician Training

- Increasing Complexity of Modern Vehicle Repair Processes

- Shortage of Skilled Collision Repair Technicians

- Market Opportunities

- Expansion of EV Collision Repair Services

- Growth in ADAS Calibration & Electronic System Repairs

- Increasing Adoption of AI-Based Damage Assessment Solutions

- Development of OEM-Certified Repair Networks

- Market Challenges

- Managing Repair Costs Amid Rising Vehicle Technology Complexity

- Maintaining Compliance with Evolving Safety Standards

- Balancing Repair Quality, Turnaround Time & Profitability

- Structural Drivers of Market Growth

- Global Automotive Collision Repair Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Demand-Supply Trends

- Service Pricing Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Service Type

- Body Repair & Structural Repair (Largest Segment)

- Painting & Refinishing

- Glass Repair & Replacement

- Dent Removal Services

- ADAS Calibration & Electronic System Repair (Fastest-Growing Segment)

- By Vehicle Type

- Passenger Vehicles (Largest Segment)

- Commercial Vehicles

- Electric Vehicles (EVs) (Fastest-Growing Segment)

- By End User

- Insurance-Supported Repairs (Largest Segment)

- Individual Vehicle Owners

- Fleet Operators

- Rental & Leasing Companies

- By Service Type

- Regional Market Analysis

- North America (Largest Market)

- Europe

- Asia-Pacific (Fastest-Growing Region)

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Competitive Intensity Analysis

- Key Player Benchmarking

- Strategic Developments

- EV Repair, ADAS & Digital Service Innovation Strategies

- Partnerships, Expansion & Insurance Network Collaboration Trends

- Company Profiles

- Boyd Group Services Inc.

- Caliber Holdings LLC

- Fix Auto World

- Gerber Collision & Glass

- Service King Collision

- Driven Brands Holdings Inc.

- ABRA Auto Body Repair

- Crash Champions

- Joe Hudson’s Collision Center

- Dent Wizard International

- Strategic Outlook

- Future of EV Repair & Specialized Collision Services

- AI-Driven Damage Assessment & Repair Automation

- Expansion of ADAS Calibration & Connected Vehicle Repair Solutions

- Growth of Digital Repair Management Platforms

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Automotive Collision Repair Market Competitive Intensity & Market Structure Overview

The Global Automotive Collision Repair Market is highly competitive and fragmented, consisting of independent repair shops, multi-location collision repair chains, OEM-certified service centers, dealership repair facilities, and specialized vehicle restoration providers. Competitive intensity is primarily driven by repair quality, turnaround time, insurance partnerships, technological capabilities, certification standards, and customer service excellence.

Companies compete across body repair, structural restoration, painting and refinishing, glass replacement, dent repair, ADAS recalibration, and electric vehicle repair services. Increasing vehicle complexity, advanced safety systems, and rising customer expectations for high-quality repairs are intensifying competition across global markets.

The market structure is evolving from traditional repair operations toward digitally connected repair ecosystems that integrate AI-based damage assessment, automated estimating systems, OEM-certified repair procedures, and advanced vehicle diagnostics. Strategic partnerships among insurers, automakers, repair networks, and technology providers are reshaping industry dynamics.

Global Automotive Collision Repair Market Competitive Intensity & Market Structure Current Scenario

Leading Global Automotive Collision Repair Companies

Boyd Group Services Inc.: One of the largest collision repair operators in North America, offering comprehensive repair services through an extensive network of repair centers.

Caliber Holdings LLC: A leading automotive collision repair company recognized for its large repair network, insurance partnerships, and advanced repair capabilities.

Fix Auto World: An international collision repair franchise network providing standardized repair services and customer-focused vehicle restoration solutions.

Gerber Collision & Glass: A major provider of collision repair and automotive glass replacement services with a strong presence across North America.

Service King Collision: A well-established collision repair operator specializing in accident repair, paint refinishing, and insurance-supported repair services.

Driven Brands Holdings Inc.: A diversified automotive services company with collision repair operations supported by advanced repair technologies and franchise networks.

ABRA Auto Body Repair: A recognized provider of collision repair services offering structural repair, painting, and vehicle restoration solutions.

Crash Champions: A rapidly expanding collision repair network focused on certified repair services, customer satisfaction, and operational excellence.

Joe Hudson’s Collision Center: A prominent collision repair organization providing accident repair, refinishing, and insurance claim support services.

Dent Wizard International: A leading provider of paintless dent repair, cosmetic restoration, and vehicle appearance enhancement services.

Key Competitive Intensity & Market Structure Drivers

The increasing complexity of modern vehicles, including ADAS technologies, connected systems, and electric powertrains, is intensifying competition among repair providers seeking specialized expertise.

Growing demand for OEM-certified repairs, vehicle safety compliance, and high-quality restoration services is driving investment in technician training and advanced repair equipment.

Insurance company partnerships and direct repair programs remain critical competitive factors influencing repair volume, customer acquisition, and revenue stability.

The adoption of digital estimating platforms, AI-driven damage assessment tools, and automated workflow management systems is reshaping operational efficiency and service delivery.

Rising electric vehicle adoption is creating new opportunities for differentiation through specialized EV repair facilities, battery handling expertise, and advanced diagnostic capabilities.

Strategic Implications of Competitive Intensity & Market Structure

Companies with strong repair networks, OEM certifications, insurance relationships, and advanced technological capabilities are expected to maintain significant competitive advantages.

Investment in ADAS calibration systems, EV repair infrastructure, digital repair management platforms, and technician certification programs is becoming a key factor for long-term market differentiation.

Repair providers focusing on customer experience, operational efficiency, and safety-focused repair standards are likely to strengthen their market positioning.

Strategic expansion through acquisitions, franchise development, and regional service network growth is enabling organizations to increase market share and geographic reach.

Organizations capable of combining technical expertise, service quality, regulatory compliance, affordability, and digital innovation will be better positioned to compete effectively across diverse customer segments.

Global Automotive Collision Repair Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global automotive collision repair market is expected to become increasingly technology-driven as vehicle electrification, connected mobility, and advanced safety systems gain wider adoption worldwide.

Future competition will be shaped by advancements in AI-powered damage assessment, automated repair workflows, EV-specific repair technologies, ADAS recalibration services, and predictive vehicle diagnostics.

Repair providers are expected to increase investments in digital transformation, advanced equipment, workforce training, and OEM certification programs to strengthen competitive positioning.

Over the forecast period, companies that successfully balance technological innovation, repair quality, operational efficiency, customer satisfaction, and regulatory compliance will be best positioned to lead the evolving global automotive collision repair market.

Value Chain

Global Automotive Collision Repair Market Value Chain & Supply Chain Evolution Overview

The Global Automotive Collision Repair Market is undergoing significant transformation driven by increasing vehicle ownership, rising accident frequency, growing insurance penetration, and the rapid integration of advanced vehicle technologies such as electric vehicles (EVs), Advanced Driver Assistance Systems (ADAS), connected vehicles, and lightweight structural materials. The market???s value chain encompasses vehicle damage assessment, parts sourcing, repair operations, refinishing services, calibration procedures, insurance coordination, and post-repair quality assurance.

A defining characteristic of this value chain is the growing convergence of automotive engineering, digital diagnostics, insurance management, repair automation, and vehicle safety compliance. Collision repair providers are increasingly investing in AI-powered damage assessment systems, advanced calibration equipment, digital repair workflow platforms, and technician certification programs to support modern vehicle repair requirements.

Supply chain complexity continues to increase due to the growing use of specialized vehicle components, sensor-integrated systems, EV battery technologies, OEM-certified parts requirements, and stringent safety regulations. Market participants must coordinate across automakers, parts suppliers, insurance providers, technology vendors, repair networks, and calibration specialists while maintaining repair quality, operational efficiency, and regulatory compliance.

Companies are increasingly investing in EV repair infrastructure, ADAS recalibration technologies, predictive diagnostics, automated estimating systems, and digital repair management platforms to address evolving customer expectations and vehicle complexity. The value chain is evolving into a highly technology-driven, safety-focused, and service-oriented ecosystem supporting the global automotive aftermarket industry.

Global Automotive Collision Repair Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Vehicle Damage Assessment & Claims Processing: Accident inspection, digital damage assessment, insurance claim verification, repair estimation, and repair authorization.

- Parts Manufacturing & Supply: Production and distribution of OEM components, aftermarket parts, body panels, glass systems, electronic modules, sensors, batteries, and structural materials.

- Collision Repair Operations: Body repair, frame straightening, dent removal, structural restoration, mechanical repairs, and component replacement services.

- Painting, Refinishing & Restoration: Surface preparation, paint matching, refinishing, coating applications, and cosmetic restoration procedures.

- ADAS Calibration & Electronic System Repair: Sensor calibration, camera alignment, radar adjustments, software updates, and advanced vehicle system verification.

- Quality Assurance & Vehicle Delivery: Safety inspections, performance testing, compliance verification, customer handover, and warranty support.

Company-to-Stage Mapping

- Vehicle Damage Assessment & Claims Processing: Insurance companies, digital estimating solution providers, fleet operators, and collision management platforms.

- Parts Manufacturing & Supply: Automotive OEMs, aftermarket parts manufacturers, glass suppliers, battery suppliers, and electronic component providers.

- Collision Repair Operations: Boyd Group Services Inc., Caliber Holdings LLC, Gerber Collision & Glass, Crash Champions, and Service King Collision.

- Painting, Refinishing & Restoration: Specialized refinishing service providers, paint manufacturers, and collision repair centers.

- ADAS Calibration & Electronic System Repair: OEM-certified repair facilities, calibration technology providers, and advanced diagnostic equipment suppliers.

- Quality Assurance & Vehicle Delivery: Repair networks, certified inspection teams, insurance-approved facilities, and customer service organizations.

Key Value Chain & Supply Chain Evolution Signals in Global Automotive Collision Repair Market

Expansion of ADAS Calibration Services

Increasing integration of cameras, radar systems, sensors, and driver assistance technologies is driving demand for specialized calibration and electronic repair capabilities.

Growth of Electric Vehicle Repair Infrastructure

Rapid EV adoption is creating demand for battery diagnostics, high-voltage system repair expertise, and dedicated EV collision repair facilities.

Digitalization of Repair Workflows

AI-powered damage assessment, digital estimating platforms, repair management software, and automated workflow systems are improving operational efficiency and repair accuracy.

Strengthening OEM Certification Programs

Automakers are expanding certified repair networks to ensure repair quality, vehicle safety compliance, and proper restoration of advanced vehicle technologies.

Increasing Insurance-Repairer Collaboration

Strategic partnerships between insurers and repair networks are improving claims processing, reducing repair cycle times, and enhancing customer experience.

Supply Chain Optimization for Specialized Components

Repair providers are strengthening relationships with OEMs and parts suppliers to improve availability of sensors, electronics, structural components, and EV-related systems.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Advanced Repair Technologies

Companies investing in digital diagnostics, AI-powered estimating, calibration systems, and automated repair equipment can strengthen competitive positioning.

Expansion of EV & ADAS Repair Capabilities

Developing specialized technician expertise and infrastructure for EVs and advanced safety systems can unlock significant future growth opportunities.

Strengthening OEM & Insurance Partnerships

Collaborations with automakers and insurance providers can improve repair volumes, customer trust, and long-term business stability.

Enhancing Supply Chain Resilience

Diversified sourcing strategies, strategic inventory management, and supplier partnerships can reduce parts shortages and repair delays.

Digital Transformation of Service Operations

Integrated repair management platforms, customer communication tools, and predictive analytics can improve efficiency and customer satisfaction.

Focus on Technician Training & Certification

Continuous workforce development and certification programs are essential for maintaining repair quality and adapting to evolving vehicle technologies.

Global Automotive Collision Repair Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the value chain is expected to evolve into a highly connected, digitally enabled, and technology-intensive ecosystem focused on vehicle safety, operational efficiency, and customer-centric service delivery.

Key Future Developments Include:

- Expansion of EV-specific repair centers and battery servicing capabilities.

- Increased adoption of AI-powered damage assessment and automated repair estimation systems.

- Growing demand for ADAS calibration, sensor alignment, and connected vehicle repair services.

- Strengthening of OEM-certified repair networks and standardized repair procedures.

- Expansion of digital repair management platforms and real-time customer engagement solutions.

- Greater focus on supply chain resilience, parts availability, and repair process optimization.

As the market evolves, competitive advantage will increasingly depend on the ability to combine advanced repair expertise, digital technologies, certified repair standards, and efficient supply chain management within an integrated automotive service ecosystem.

Companies that successfully integrate EV repair specialization, ADAS calibration capabilities, digital workflow automation, and strategic industry partnerships will achieve stronger market positioning, operational excellence, and long-term growth in the Global Automotive Collision Repair Market.

Investment Activity

Global Automotive Collision Repair Market Investment & Funding Dynamics Overview

The Global Automotive Collision Repair Market is witnessing significant investment activity driven by increasing vehicle ownership, rising insurance-supported repairs, growing adoption of electric vehicles (EVs), and the increasing complexity of modern vehicle technologies. Collision repair operators, automotive service providers, insurance companies, private equity firms, OEMs, and technology vendors are actively investing in advanced repair facilities, ADAS calibration systems, EV repair infrastructure, digital repair management platforms, and technician training programs.

Investment momentum is accelerating as repair networks modernize operations to address evolving vehicle architectures, connected vehicle technologies, and stricter safety requirements. Capital allocation is increasingly focused on AI-powered damage assessment tools, automated estimating systems, advanced diagnostics equipment, OEM-certified repair centers, and smart workshop technologies.

Additionally, growing investments in ADAS recalibration services, EV battery repair capabilities, digital customer engagement platforms, and repair process automation are creating substantial long-term opportunities across the global automotive collision repair ecosystem.

Global Automotive Collision Repair Market Investment & Funding Dynamics Current Scenario

Currently, the market is experiencing robust capital deployment as repair operators expand service capabilities to accommodate increasingly sophisticated vehicle systems. Industry participants are investing heavily in advanced repair equipment, calibration technologies, vehicle scanning systems, and specialized EV repair facilities.

The market is benefiting from strategic investments by insurance providers, OEMs, and large repair networks seeking to improve repair quality, operational efficiency, and customer experience. Significant funding is being directed toward network expansion, digital workflow solutions, technician certification programs, and repair automation technologies.

Furthermore, strategic partnerships among automakers, insurers, repair chains, software providers, and equipment manufacturers are reshaping investment flows and accelerating the adoption of advanced repair solutions throughout the value chain.

Key Investment & Funding Dynamics Signals in Global Automotive Collision Repair Market

- Growing demand for ADAS calibration and electronic system repair services is driving investments in specialized equipment and technician training.

- Expansion of the global electric vehicle fleet is increasing capital deployment toward EV-specific repair infrastructure and battery handling capabilities.

- Rising adoption of AI-based damage assessment and automated estimating platforms is supporting technology-focused funding.

- Insurance-backed repair programs and direct repair network partnerships are strengthening investment confidence across organized repair operators.

- Strategic investments in OEM-certified repair facilities and advanced diagnostics technologies are creating competitive differentiation opportunities.

- Growing focus on repair process automation, workflow optimization, and digital customer engagement is improving operational efficiency.

- Increasing utilization of connected vehicle diagnostics and predictive repair technologies is attracting innovation-led capital.

Strategic Implications of Investment & Funding Dynamics in Global Automotive Collision Repair Market

- Continuous investment in advanced diagnostics, calibration technologies, and repair automation is essential for maintaining competitive leadership.

- Capital allocation toward EV repair facilities, battery safety systems, and technician certification programs will strengthen market positioning.

- Companies developing technology-enabled collision repair ecosystems are expected to secure stronger long-term growth opportunities.

- Strategic partnerships between insurers, OEMs, repair operators, and technology providers will accelerate service innovation and network expansion.

- Investments in digital repair management platforms, customer experience solutions, and AI-driven workflows will remain key growth priorities.

- Compliance with vehicle safety standards, insurance regulations, OEM repair requirements, and repair certification programs will continue influencing investment decisions.

- Organizations building integrated capabilities across vehicle diagnostics, structural repair, ADAS calibration, and EV servicing are expected to capture substantial future value.

Global Automotive Collision Repair Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Automotive Collision Repair Market is expected to maintain strong investment momentum driven by vehicle parc expansion, increasing repair complexity, growing EV adoption, and rising demand for certified repair services.

Future capital deployment will increasingly focus on ADAS calibration infrastructure, AI-powered repair management systems, EV repair technologies, connected vehicle diagnostics, and automated workshop solutions.

As automakers, insurers, and repair providers continue prioritizing vehicle safety, operational efficiency, and customer satisfaction, investment activity is expected to expand across advanced repair facilities, technician development programs, digital service platforms, and next-generation repair technologies.

In conclusion, the Global Automotive Collision Repair Market represents a strategically important automotive aftermarket investment landscape where EV repair specialization, ADAS recalibration, AI-driven diagnostics, digital workflow management, and OEM-certified repair excellence will define future funding priorities, competitive differentiation, and long-term industry growth.

Technology & Innovation

Global Automotive Collision Repair Market Technology & Innovation Landscape Overview

The Global Automotive Collision Repair Market is undergoing a major technological transformation driven by advancements in artificial intelligence (AI), advanced vehicle diagnostics, ADAS calibration technologies, electric vehicle (EV) repair systems, digital repair management platforms, and automated damage assessment solutions. The market demonstrates a high innovation intensity level as repair providers adapt to increasingly complex vehicle architectures, connected technologies, and evolving safety standards.

At the center of this transformation is the shift from conventional repair processes toward digitally connected, data-driven, and OEM-compliant repair ecosystems designed to improve repair accuracy, operational efficiency, and vehicle safety restoration.

A major innovation area is AI-powered damage assessment, where computer vision technologies, machine learning algorithms, and automated estimating systems are accelerating repair planning, insurance claim processing, and repair cost estimation.

The market is also witnessing rapid advancements in ADAS calibration technologies as modern vehicles increasingly rely on cameras, radar sensors, lidar systems, and electronic safety components that require precise recalibration following repairs.

Repair centers are investing heavily in EV-specific repair infrastructure, including high-voltage battery diagnostics, battery enclosure repair systems, thermal management inspection tools, and technician certification programs to address growing electric vehicle adoption.

Product and service innovation further includes digital repair workflow platforms, cloud-based repair management systems, 3D vehicle scanning technologies, robotic paint application systems, and automated frame measurement solutions.

Additionally, connected vehicle diagnostics and OEM-integrated repair software are improving repair precision, reducing turnaround times, and enhancing compliance with manufacturer repair procedures.

The convergence of AI diagnostics, digital repair ecosystems, EV repair technologies, ADAS calibration systems, and connected vehicle data is redefining the future technology landscape of the global automotive collision repair market.

Global Automotive Collision Repair Market Technology & Innovation Landscape Current Scenario

Currently, the Global Automotive Collision Repair Market is experiencing increasing adoption of advanced diagnostic technologies, automated repair workflows, and specialized vehicle repair capabilities to address evolving automotive technologies.

1. AI-Based Damage Assessment Systems

Artificial intelligence and computer vision technologies are enabling faster vehicle inspections, automated repair estimates, and improved insurance claim processing.

2. ADAS Calibration Technologies

Advanced calibration equipment is ensuring accurate restoration of cameras, radar sensors, and driver assistance systems following collision repairs.

3. EV Repair & Battery Diagnostics

Specialized repair facilities are adopting high-voltage safety systems, battery health assessment tools, and EV-specific repair procedures.

4. Digital Repair Management Platforms

Cloud-based software solutions are streamlining workflow management, repair tracking, customer communication, and operational efficiency.

5. 3D Scanning & Structural Measurement Systems

Advanced scanning technologies are improving damage detection accuracy and supporting precision structural repairs.

6. Automated Paint & Refinishing Technologies

Modern paint-matching systems and robotic refinishing equipment are enhancing quality consistency and reducing material waste.

Key Technology & Innovation Landscape Signals in Global Automotive Collision Repair Market

Several innovation trends are shaping the future development of the market:

1. Rapid Growth of Electric Vehicle Repair Demand

Increasing EV adoption is driving investment in specialized repair equipment, battery diagnostics, and technician training.

2. Expansion of ADAS-Equipped Vehicles

The growing presence of advanced safety technologies is accelerating demand for calibration and electronic repair services.

3. Increasing Adoption of AI & Automation

Artificial intelligence is improving repair estimation, damage detection, workflow optimization, and insurance processing.

4. Rise of Connected Vehicle Data Integration

Repair centers are increasingly leveraging vehicle-generated data to improve diagnostics and repair accuracy.

5. Growing OEM Certification Requirements

Manufacturers are strengthening repair standards to ensure safety, performance, and warranty compliance.

6. Digitalization of Repair Operations

Repair businesses are adopting cloud-based platforms and digital communication tools to improve efficiency and customer experience.

7. Advanced Material Repair Technologies

Increasing use of aluminum, carbon fiber, and mixed-material vehicle structures is driving demand for specialized repair solutions.

Strategic Implications of Technology & Innovation Landscape in Global Automotive Collision Repair Market

The evolving innovation landscape is reshaping competition throughout the automotive collision repair industry. Repair providers are increasingly competing through technical expertise, digital capabilities, OEM certifications, and advanced vehicle repair specialization.

Organizations investing in AI-powered diagnostics, ADAS calibration systems, EV repair infrastructure, technician certification programs, and digital workflow management platforms are expected to strengthen long-term market positioning.

Strategic collaborations among repair networks, insurance companies, automotive manufacturers, technology providers, and equipment suppliers are accelerating innovation and improving service quality.

The growing convergence of connected vehicles, predictive diagnostics, digital repair ecosystems, and advanced vehicle technologies is creating substantial differentiation opportunities across the market.

Additionally, compliance with vehicle safety standards, repair certification requirements, insurance regulations, and OEM repair procedures is driving continuous technological modernization throughout the industry.

Global Automotive Collision Repair Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026???2033, the Global Automotive Collision Repair Market is expected to evolve toward highly automated, digitally connected, and data-driven repair ecosystems supported by AI, advanced diagnostics, and next-generation vehicle technologies.

Future technological developments are likely to include:

1. AI-Powered Predictive Damage Analytics

Advanced artificial intelligence systems will improve repair planning, cost estimation, and insurance claim automation.

2. Fully Integrated ADAS Calibration Ecosystems

Automated calibration technologies will ensure faster and more accurate restoration of advanced safety systems.

3. Next-Generation EV Repair Technologies

Advanced battery diagnostics, automated repair procedures, and specialized EV service platforms will become industry standards.

4. Connected Vehicle Repair Intelligence Platforms

Real-time vehicle data integration will enhance diagnostics, repair accuracy, and predictive maintenance capabilities.

5. Robotic Repair & Refinishing Systems

Automation technologies will improve consistency, productivity, and repair quality across collision repair operations.

6. Digital Twin & 3D Repair Modeling Solutions

Virtual vehicle models will support highly accurate damage analysis, repair simulation, and quality assurance processes.

7. Smart Insurance & Repair Ecosystems

Integrated insurer-repairer platforms will streamline claims processing, approvals, repair tracking, and customer communication.

In conclusion, companies capable of combining AI-driven diagnostics, EV repair expertise, ADAS calibration capabilities, connected vehicle technologies, and digital repair management systems will be best positioned to lead the future evolution of the Global Automotive Collision Repair Market.

Market Risk

Global Automotive Collision Repair Market Risk Factors & Disruption Threats Overview

The Global Automotive Collision Repair Market operates within a rapidly evolving automotive aftermarket ecosystem where repair centers, insurers, OEMs, dealerships, technology providers, and fleet operators collaborate to restore vehicle safety and functionality following accidents and damage events. While the market benefits from growing vehicle ownership, increasing insurance penetration, and rising repair complexity, it faces significant structural risks related to vehicle safety technology evolution, labor shortages, insurance cost pressures, and changing mobility trends.

A major structural risk is the increasing complexity of modern vehicles. The widespread adoption of advanced driver assistance systems (ADAS), connected vehicle technologies, lightweight materials, and electric vehicle architectures requires specialized repair procedures, advanced diagnostic equipment, and highly trained technicians, increasing repair costs and operational challenges.

Another significant disruption factor is the industry’s dependence on insurance claim volumes and reimbursement structures. Changes in insurance policies, claims management practices, deductible structures, or accident frequency can directly impact repair demand and profitability.

The market also faces growing workforce constraints. A shortage of certified collision repair technicians, EV specialists, refinishing professionals, and ADAS calibration experts is increasing labor costs and creating capacity limitations across many regions.

Additionally, the expansion of vehicle safety technologies designed to reduce accidents may gradually lower collision frequency over the long term, creating potential demand shifts within traditional repair segments.

Global Automotive Collision Repair Market Risk Factors & Disruption Threats Current Scenario

The current market is characterized by rising repair complexity as modern vehicles integrate advanced electronics, sensor systems, cameras, radar technologies, and sophisticated structural materials.

Electric vehicle adoption is accelerating demand for specialized repair capabilities, including battery diagnostics, high-voltage system handling, and EV-specific structural repair procedures.

Insurance companies continue to play a central role in repair authorization, cost control, and repair network management, influencing service provider operations and pricing strategies.

At the same time, repair centers are investing in digital estimating platforms, AI-powered damage assessment tools, technician certification programs, and advanced calibration equipment to meet evolving market requirements.

OEM-certified repair networks are expanding globally as automakers seek greater control over repair quality, safety compliance, and customer experience.

Key Risk Factors & Disruption Threats Signals in Global Automotive Collision Repair Market

A major disruption signal is the rapid growth of ADAS calibration services, reflecting the increasing integration of cameras, sensors, radar systems, and automated safety technologies into modern vehicles.

Another important signal is the continued expansion of electric vehicle fleets, creating demand for specialized repair infrastructure, battery handling expertise, and high-voltage technician certifications.

The adoption of AI-driven damage assessment, digital repair management systems, and automated estimating platforms is transforming operational workflows and improving repair efficiency.

Vehicle manufacturers are increasingly promoting OEM-certified repair programs, influencing repair standards, technician training requirements, and aftermarket service ecosystems.

The long-term advancement of autonomous driving technologies and accident avoidance systems may gradually alter accident frequency patterns, potentially reshaping future repair demand dynamics.

Strategic Implications of Risk Factors & Disruption Threats in Global Automotive Collision Repair Market

Repair organizations must continuously invest in technician training, certification programs, and advanced diagnostic capabilities to address increasing vehicle technology complexity.

Investment in EV repair facilities, battery safety infrastructure, ADAS calibration systems, and digital repair platforms will be essential for maintaining competitiveness and capturing emerging opportunities.

Companies should strengthen relationships with insurers, OEMs, fleet operators, and leasing companies to secure stable repair volumes and long-term service partnerships.

Workforce development initiatives, recruitment programs, and skills enhancement strategies will become increasingly important in addressing industry-wide labor shortages.

Organizations that successfully integrate AI-based damage assessment, workflow automation, and customer engagement technologies are likely to improve operational efficiency and profitability.

Global Automotive Collision Repair Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Automotive Collision Repair Market is expected to become increasingly technology-intensive as electric vehicles, connected cars, and advanced safety systems reshape repair requirements.

ADAS calibration, electronic diagnostics, software-related repairs, and EV-specific collision services are expected to represent some of the fastest-growing segments within the industry.

Regulatory requirements surrounding vehicle safety, repair quality, technician certification, and battery handling standards are expected to become increasingly rigorous across major markets.

Artificial intelligence, predictive diagnostics, digital repair ecosystems, and automated claims processing will significantly improve repair efficiency, transparency, and customer experience.

Overall, the market will remain resilient but increasingly specialized, with long-term success determined by technical expertise, digital transformation, workforce capabilities, insurer and OEM partnerships, and the ability to safely repair next-generation vehicles within an increasingly advanced automotive ecosystem.

Regulatory Landscape

Global Automotive Collision Repair Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Automotive Collision Repair Market is becoming increasingly complex as governments, transportation authorities, insurance regulators, vehicle manufacturers, and safety organizations focus on improving vehicle safety, repair quality, environmental compliance, and consumer protection. Regulatory frameworks play a critical role in ensuring that repaired vehicles meet safety standards and are restored to proper operating condition following collisions and accident-related damage.

Collision repair facilities, OEM-certified service centers, independent repair shops, insurance companies, parts suppliers, and calibration service providers must comply with a wide range of regulations covering vehicle safety standards, repair procedures, technician certifications, environmental requirements, insurance claims management, and quality assurance protocols. The growing adoption of advanced vehicle technologies is further expanding regulatory oversight into areas such as ADAS calibration, electric vehicle repair safety, and digital repair documentation.

As modern vehicles incorporate increasingly sophisticated electronic systems, sensors, cameras, and connected technologies, policymakers and industry stakeholders are strengthening standards to ensure proper repair, recalibration, and post-repair vehicle performance.

Global Automotive Collision Repair Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by increasing emphasis on vehicle safety compliance and repair quality assurance. Transportation authorities and automotive safety agencies continue implementing regulations that require damaged vehicles to be repaired according to approved procedures and safety standards.

Vehicle safety regulations are influencing repair practices by establishing requirements for structural integrity restoration, airbag system functionality, crashworthiness performance, and proper recalibration of advanced safety systems. Repair facilities are increasingly required to follow manufacturer-recommended procedures and utilize certified repair techniques.

Insurance regulations remain a major factor shaping market dynamics. Regulatory frameworks governing insurance claims, repair estimates, policyholder rights, and repair network operations influence relationships between insurers, repair providers, and vehicle owners.

Environmental regulations are also impacting collision repair operations by establishing standards related to paint emissions, hazardous material handling, waste disposal, recycling practices, and sustainable repair processes. Compliance with environmental requirements is becoming an important component of operational management.

At the same time, the increasing adoption of electric vehicles and ADAS-equipped vehicles is driving greater regulatory attention toward technician certification, high-voltage system safety, sensor calibration accuracy, and specialized repair equipment requirements.

Key Regulatory & Policy Environment Signals in Global Automotive Collision Repair Market

- Vehicle Safety Standards: Regulations governing structural repairs, crashworthiness restoration, airbag functionality, occupant protection systems, and post-collision vehicle safety.

- Repair Certification & Technician Qualification Requirements: Standards requiring technician training, repair certifications, OEM-approved repair procedures, and specialized technical competencies.

- Insurance Claims & Repair Regulations: Frameworks governing claims processing, repair estimates, insurer-repairer relationships, consumer rights, and reimbursement practices.

- ADAS Calibration & Electronic System Compliance: Emerging requirements related to calibration accuracy, sensor functionality, advanced safety systems, and electronic repair validation.

- Environmental & Emissions Regulations: Standards addressing paint shop emissions, hazardous waste handling, chemical management, recycling initiatives, and sustainable repair operations.

- Electric Vehicle Repair Safety Requirements: Regulations governing battery handling, high-voltage system repairs, technician safety procedures, and EV-specific repair protocols.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging collision repair businesses to invest in technician training, repair certifications, advanced diagnostic tools, and quality assurance systems. Regulatory compliance is increasingly becoming a competitive differentiator within the industry.

Vehicle safety standards are driving demand for OEM-certified repair facilities, advanced calibration equipment, and standardized repair procedures. Repair providers capable of delivering compliant and high-quality services are expected to strengthen customer trust and insurer partnerships.

Insurance regulations are encouraging greater transparency in repair processes, digital claims management, and operational efficiency. Organizations that effectively align with insurer requirements may gain access to larger repair volumes and preferred network opportunities.

The expansion of electric vehicles and advanced driver assistance systems is creating new opportunities for repair centers that invest in specialized equipment, workforce development, and technical certifications required to meet emerging regulatory expectations.

Environmental compliance requirements are also encouraging adoption of sustainable repair practices, waste reduction initiatives, and eco-friendly materials that support broader automotive sustainability objectives.

Global Automotive Collision Repair Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global automotive collision repair market is expected to become more stringent as vehicle technologies continue to evolve and safety expectations increase. Governments and industry regulators are likely to introduce enhanced standards for repair quality, technician competency, and post-repair vehicle verification.

ADAS calibration requirements are expected to become increasingly standardized, with greater emphasis on documentation, validation procedures, and safety performance testing following collision repairs.

Electric vehicle regulations will likely expand to address battery safety, thermal event prevention, technician certification programs, and specialized repair facility requirements as EV adoption accelerates globally.

Environmental regulations may place greater focus on carbon reduction, resource efficiency, sustainable materials, recycling practices, and environmentally responsible repair operations throughout the collision repair value chain.

Overall, the future regulatory landscape will be shaped by the convergence of vehicle safety standards, repair certification requirements, insurance regulations, environmental compliance measures, ADAS calibration frameworks, and electric vehicle safety protocols. Companies capable of delivering compliant, technology-enabled, certified, and high-quality repair services will be best positioned to capitalize on long-term opportunities within the evolving global automotive collision repair market.