Global Cellulose Market Report, Size, Share and Forecast 2026–2033

Global Cellulose Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

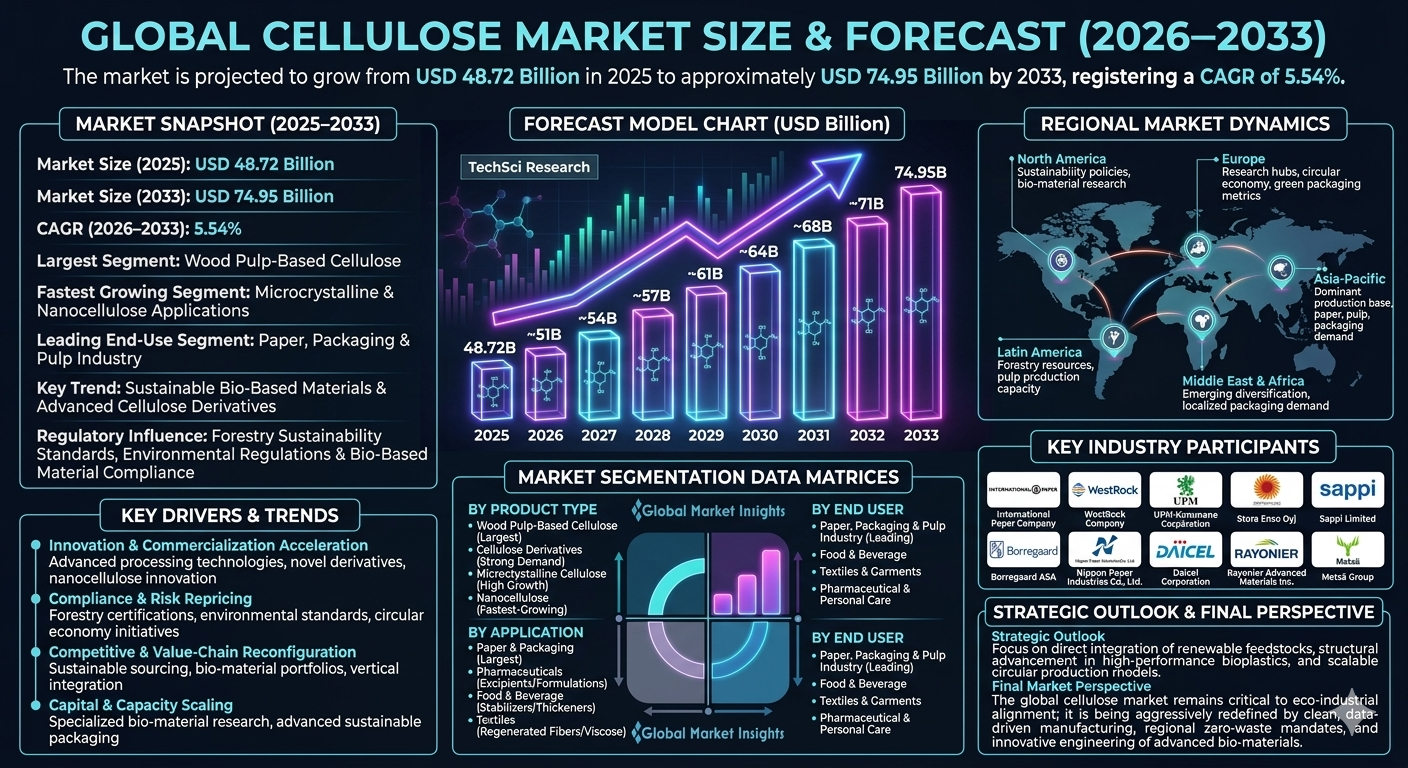

| Market Size (2025) | USD 48.72 Billion |

| Market Size (2033) | USD 74.95 Billion |

| CAGR (2026???2033) | 5.54% |

| Largest Segment | Wood Pulp-Based Cellulose |

| Fastest Growing Segment | Microcrystalline & Nanocellulose Applications |

| Leading End-Use Segment | Paper, Packaging & Pulp Industry |

| Key Trend | Sustainable Bio-Based Materials & Advanced Cellulose Derivatives |

| Regulatory Influence | Forestry Sustainability Standards, Environmental Regulations & Bio-Based Material Compliance |

| Future Outlook | Growth Driven by Sustainable Packaging, Bioplastics & High-Performance Cellulose Applications |

Global Cellulose Market size & Forecast

The Global Cellulose Market is expected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at USD 48.72 billion in 2025 and is projected to reach approximately USD 74.95 billion by 2033, registering a CAGR of 5.54%. The market growth is primarily driven by increasing demand for sustainable packaging materials, rising consumption of paper and tissue products, expanding pharmaceutical applications, and growing adoption of bio-based materials across industries. Cellulose remains one of the most abundant renewable biopolymers used in paper manufacturing, textiles, food ingredients, pharmaceuticals, construction materials, and specialty chemicals. Growing environmental awareness and sustainability initiatives are accelerating market expansion. In addition, innovations in nanocellulose, cellulose derivatives, and biodegradable materials are supporting long-term market development.Global Cellulose Market Overview

Cellulose is a natural polysaccharide found in plant cell walls and serves as a critical raw material for numerous industrial and commercial applications. The market includes wood pulp cellulose, cotton cellulose, regenerated cellulose, cellulose ethers, cellulose acetate, microcrystalline cellulose, and nanocellulose products. Cellulose-based materials are widely utilized across paper manufacturing, packaging, pharmaceuticals, food processing, textiles, construction, and personal care industries. The market is shifting toward advanced cellulose technologies, sustainable sourcing practices, and high-performance bio-based material solutions.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in nanocellulose production, biodegradable packaging materials, cellulose composites, and specialty cellulose derivatives is expanding commercial applications. Advanced processing technologies are improving material performance, functionality, and sustainability.Market Implications

Companies investing in advanced cellulose technologies and sustainable product innovation are expected to strengthen market leadership.2. Compliance and Risk Repricing

Forestry management regulations, sustainability certifications, environmental compliance standards, and circular economy initiatives are influencing industry practices. Governments and organizations are increasingly promoting renewable and biodegradable material adoption.Market Implications

Firms offering certified sustainable sourcing and environmentally responsible cellulose products are likely to gain stronger market acceptance.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as pulp producers, specialty chemical manufacturers, packaging companies, and biomaterial developers expand cellulose-based product portfolios. Vertical integration and sustainable supply chain strategies are reshaping value-chain economics.Market Implications

Companies focusing on value-added cellulose derivatives and advanced biomaterial solutions may gain stronger margins.4. Capital and Capacity Scaling

Rising investment in pulp manufacturing, sustainable packaging facilities, nanocellulose production plants, and biomaterial research is supporting market growth. Growing demand for renewable materials across multiple industries is increasing production capacity requirements.Market Implications

Manufacturers scaling sustainable and technologically advanced cellulose production capabilities are expected to capture future opportunities.Market Segmentation Analysis

By Product Type

1. Wood Pulp-Based Cellulose

This remains the largest segment due to widespread availability and extensive industrial utilization.2. Cellulose Derivatives

Strong demand across pharmaceuticals, food processing, and specialty chemicals.3. Cellulose Acetate

Widely used in textiles, filtration products, and consumer goods.4. Microcrystalline Cellulose

Growing adoption in pharmaceutical and food applications.5. Nanocellulose

Fastest-growing segment due to high-strength, lightweight, and sustainable material properties.By Application

1. Paper & Packaging

Largest segment driven by packaging and printing industry demand.2. Pharmaceuticals

Strong demand for excipients and drug formulation applications.3. Food & Beverage

Used as stabilizers, thickeners, and dietary fiber ingredients.4. Textiles

Widely utilized in regenerated fiber manufacturing.5. Construction & Industrial Applications

Growing use in composites and specialty building materials.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global cellulose market due to large-scale paper production, packaging demand, and expanding industrial manufacturing activities.North America

North America remains a major market supported by advanced biomaterial research and sustainable packaging initiatives.Europe

Europe is witnessing strong growth driven by circular economy policies and bio-based material adoption.Latin America

Latin America is gradually expanding due to forestry resources and growing pulp production investments.Middle East & Africa

The region is witnessing emerging demand driven by packaging growth and industrial diversification efforts.Competitive Landscape

The Global Cellulose Market is highly competitive with pulp manufacturers, specialty chemical producers, and biomaterial companies operating globally.Key Companies Operating in the Market Include:

- International Paper Company

- WestRock Company

- UPM-Kymmene Corporation

- Stora Enso Oyj

- Sappi Limited

- Borregaard ASA

- Nippon Paper Industries Co., Ltd.

- Daicel Corporation

- Rayonier Advanced Materials Inc.

- Mets?? Group

Strategic Outlook

The future of the cellulose market will be shaped by nanocellulose innovation, biodegradable packaging solutions, advanced biomaterials, and sustainable manufacturing technologies. Integration of renewable feedstocks, circular production models, and high-performance cellulose composites will significantly improve commercial opportunities. The rise of sustainable packaging, green materials, and bio-based industrial products is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Cellulose Market remains a critical segment within renewable materials, packaging, pharmaceuticals, and industrial manufacturing ecosystems. Rising demand for sustainable and biodegradable materials continues driving long-term market growth. Companies capable of delivering innovative, sustainable, and high-performance cellulose solutions will be best positioned to capture future opportunities. The convergence of biomaterial innovation, circular economy initiatives, and advanced cellulose technologies is expected to redefine the future of the global cellulose industry.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Cellulose Market Snapshot (2026???2033)

- 1.2 Market Size & Growth Overview

- 1.3 Key Market Highlights

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Performance Summary

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Market Introduction & Overview

- 2.1 Definition of Cellulose

- 2.2 Scope of the Global Cellulose Market

- 2.3 Evolution of Cellulose-Based Materials

- 2.4 Cellulose Value Chain Analysis

- 2.5 Regulatory & Sustainability Framework

- 2.6 Emerging Trends in Bio-Based Materials

- 2.7 Circular Economy & Renewable Resource Integration

- 3. Research Methodology

- 3.1 Primary Research Approach

- 3.2 Secondary Research Sources

- 3.3 Market Size Estimation Methodology

- 3.4 Forecasting Assumptions (2026???2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Market Drivers

- 4.1.1 Rising Demand for Sustainable Packaging Solutions

- 4.1.2 Growing Adoption of Bio-Based Materials

- 4.1.3 Expansion of Pharmaceutical Applications

- 4.1.4 Increasing Consumption of Paper & Tissue Products

- 4.1.5 Technological Advances in Nanocellulose

- 4.2 Market Restraints

- 4.2.1 Volatility in Raw Material Availability

- 4.2.2 Environmental Concerns Related to Pulp Processing

- 4.2.3 High Capital Requirements for Advanced Cellulose Production

- 4.3 Market Opportunities

- 4.3.1 Bioplastics & Sustainable Packaging Development

- 4.3.2 Growth of High-Performance Cellulose Composites

- 4.3.3 Expansion of Pharmaceutical Excipient Applications

- 4.3.4 Advanced Nanocellulose Commercialization

- 4.4 Market Challenges

- 4.4.1 Cost Competitiveness Against Synthetic Materials

- 4.4.2 Sustainable Forestry Management Requirements

- 4.4.3 Scaling Commercial Nanocellulose Production

- 4.1 Market Drivers

- 5. Global Cellulose Market Size & Forecast (USD Billion), 2026???2033

- 5.1 Market Revenue Analysis

- 5.2 CAGR Analysis

- 5.3 Demand-Supply Trends

- 5.4 Pricing Analysis

- 5.5 Investment Trends

- 5.6 Future Market Outlook

- 6. Market Segmentation Analysis (USD Billion), 2026???2033

- 6.1 By Product Type

- 6.1.1 Wood Pulp-Based Cellulose (Largest Segment)

- 6.1.2 Cellulose Derivatives

- 6.1.3 Cellulose Acetate

- 6.1.4 Microcrystalline Cellulose

- 6.1.5 Nanocellulose (Fastest-Growing Segment)

- 6.2 By Application

- 6.2.1 Paper & Packaging (Largest Segment)

- 6.2.2 Pharmaceuticals

- 6.2.3 Food & Beverage

- 6.2.4 Textiles

- 6.2.5 Construction & Industrial Applications

- 6.1 By Product Type

- 7. Regional Market Analysis

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Competitive Benchmarking

- 8.3 Strategic Developments

- 8.4 Sustainability & Innovation Strategies

- 8.5 Capacity Expansion & Investment Analysis

- 9. Company Profiles

- 9.1 International Paper Company

- 9.2 WestRock Company

- 9.3 UPM-Kymmene Corporation

- 9.4 Stora Enso Oyj

- 9.5 Sappi Limited

- 9.6 Borregaard ASA

- 9.7 Nippon Paper Industries Co., Ltd.

- 9.8 Daicel Corporation

- 9.9 Rayonier Advanced Materials Inc.

- 9.10 Mets?? Group

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Cellulose Demand Forecast Model

- 10.2 Sustainable Packaging Opportunity Analysis

- 10.3 Bio-Based Materials Adoption Tracker

- 10.4 Nanocellulose Commercialization Assessment

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Sustainable Packaging Solutions

- 11.2 Investment in Advanced Cellulose Technologies

- 11.3 Growth Opportunities in Nanocellulose

- 11.4 Circular Economy Integration Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Market Research

- 14. Disclaimer

Competitive Landscape

Global Cellulose Market Competitive Intensity & Market Structure Overview

The global cellulose market is highly competitive and moderately fragmented, characterized by strong competition among pulp producers, specialty chemical manufacturers, paper and packaging companies, and advanced biomaterial developers. Competitive intensity is driven by sustainable raw material sourcing, production scale, product diversification, cellulose derivative innovation, cost efficiency, and compliance with environmental and forestry sustainability standards.

The market structure consists of large integrated forestry and pulp companies with extensive production capabilities alongside specialty cellulose manufacturers focused on high-value applications such as pharmaceuticals, food ingredients, textiles, and advanced biomaterials. Competition is increasingly shaped by investments in nanocellulose technologies, biodegradable materials, and circular economy-driven production systems.

Growing demand for sustainable packaging, renewable materials, bio-based chemicals, and advanced cellulose applications is significantly intensifying competition across the global cellulose market.

Global Cellulose Market Competitive Intensity & Market Structure Current Scenario

Leading Global Cellulose Companies

International Paper Company: Leading global pulp and paper producer with extensive cellulose manufacturing capabilities and broad industrial reach.

WestRock Company: Major packaging and paper solutions provider leveraging integrated cellulose supply chains.

UPM-Kymmene Corporation: Strong market participant focused on sustainable forestry management and advanced bio-based material development.

Stora Enso Oyj: Global leader in renewable materials with significant investments in sustainable cellulose and biomaterial innovation.

Sappi Limited: Major producer of dissolving wood pulp and specialty cellulose products serving multiple industrial sectors.

Borregaard ASA: Recognized innovator specializing in advanced biochemicals, cellulose derivatives, and sustainable biomaterials.

Nippon Paper Industries Co., Ltd.: Leading cellulose and paper manufacturer with diversified product applications across Asia and global markets.

Daicel Corporation: Major supplier of cellulose derivatives and specialty chemical solutions for industrial and pharmaceutical applications.

Rayonier Advanced Materials Inc.: Key producer of high-purity cellulose specialties serving pharmaceutical, food, and industrial markets.

Mets?? Group: Integrated forestry and biomaterials company focused on sustainable cellulose production and renewable material solutions.

Key Competitive Intensity & Market Structure Drivers

Growing adoption of sustainable packaging solutions is intensifying competition around renewable and biodegradable cellulose materials.

Rapid development of nanocellulose and advanced cellulose composites is accelerating innovation-driven market differentiation.

Forestry sustainability certifications and environmental regulations are strengthening competition around responsible sourcing practices.

Expansion of pharmaceutical, food, and specialty chemical applications is increasing demand for high-purity cellulose derivatives.

Circular economy initiatives are driving investments in resource-efficient production technologies and value-added biomaterial solutions.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are increasingly investing in advanced cellulose processing technologies, nanocellulose production facilities, and sustainable product innovation.

Strategic vertical integration across forestry resources, pulp production, and specialty material manufacturing is strengthening competitive positioning.

Product portfolio diversification into pharmaceuticals, food ingredients, and advanced biomaterials is enhancing revenue opportunities.

Sustainability-focused branding and certified sourcing programs are becoming critical differentiators in global markets.

Research partnerships focused on biodegradable materials, cellulose composites, and next-generation bio-based products are accelerating commercialization opportunities.

Global Cellulose Market Competitive Intensity & Market Structure Forward Outlook

The global cellulose market is expected to remain highly competitive as demand for renewable materials, sustainable packaging, and advanced bio-based products continues expanding across industries.

Future competition will increasingly focus on nanocellulose innovation, biodegradable material development, advanced cellulose derivatives, and circular production ecosystems.

Asia-Pacific will remain the dominant competitive region due to large-scale manufacturing and packaging demand, while North America and Europe will continue leading innovation in advanced biomaterials and sustainable cellulose technologies.

Advancements in high-performance cellulose composites, renewable feedstock optimization, and environmentally efficient manufacturing systems are expected to significantly reshape market dynamics.

Overall, companies that successfully combine sustainable sourcing, technological innovation, scalable production infrastructure, and value-added cellulose applications will remain strongly positioned in the evolving global cellulose market.

Value Chain

Global Cellulose Market Value Chain & Supply Chain Evolution Overview

The Global Cellulose Market is undergoing significant transformation driven by increasing demand for sustainable bio-based materials, biodegradable packaging solutions, advanced cellulose derivatives, and circular economy initiatives. The market???s value chain is characterized by a highly integrated ecosystem linking forestry operations, pulp production facilities, cellulose processors, specialty chemical manufacturers, packaging companies, distributors, and end-use industries. This interconnected structure is reshaping sourcing strategies, production technologies, and competitive dynamics across the global cellulose industry.

A defining feature of the value chain is the growing transition toward sustainable forestry management, renewable raw material utilization, and high-value cellulose applications. While traditional wood pulp-based cellulose remains the dominant source of supply, rapid advancements in microcrystalline cellulose, cellulose derivatives, regenerated cellulose, and nanocellulose technologies are expanding the market into high-performance industrial, pharmaceutical, packaging, and specialty material applications.

Supply chain complexity is increasing as manufacturers balance sustainable forestry practices, raw material availability, environmental compliance requirements, advanced processing technologies, and evolving customer expectations. Companies must coordinate efficiently across forestry management, pulp production, cellulose refinement, specialty chemical conversion, packaging integration, and global distribution networks while maintaining cost competitiveness and sustainability performance.

Industry participants are increasingly investing in sustainable forestry certification, advanced cellulose processing technologies, nanocellulose production facilities, and circular production systems to improve operational efficiency and environmental performance. The value chain is evolving into a more sustainable, technology-driven, and innovation-focused ecosystem centered on renewable materials and long-term resource efficiency.

Global Cellulose Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Material Sourcing: Wood fiber, forestry resources, cotton linters, agricultural biomass, recycled fiber, and renewable plant-based feedstocks.

- Pulp Production & Cellulose Extraction: Mechanical pulping, chemical pulping, cellulose extraction, fiber processing, bleaching, and purification operations.

- Cellulose Processing & Product Development: Production of cellulose derivatives, cellulose acetate, microcrystalline cellulose, regenerated cellulose, nanocellulose, and specialty cellulose materials.

- Regulatory & Sustainability Compliance: Forestry certification programs, environmental regulations, sustainable sourcing standards, emissions management, and bio-based material compliance requirements.

- Distribution & Logistics: Bulk material transportation, industrial distributors, packaging supply chains, specialty chemical networks, and international trade channels.

- End-Use Utilization: Paper and packaging manufacturers, pharmaceutical companies, food processors, textile producers, construction material manufacturers, and industrial product developers.

Company-to-Stage Mapping

- Raw Material Sourcing: Forestry operators, timber suppliers, agricultural biomass producers, sustainable fiber sourcing companies.

- Pulp Production & Cellulose Extraction: International Paper Company, UPM-Kymmene Corporation, Stora Enso Oyj, Nippon Paper Industries Co., Ltd., Mets?? Group.

- Cellulose Processing & Product Development: Borregaard ASA, Daicel Corporation, Rayonier Advanced Materials Inc., Sappi Limited, specialty cellulose manufacturers.

- Regulatory & Sustainability Compliance: Forest Stewardship Council (FSC), Programme for the Endorsement of Forest Certification (PEFC), environmental regulatory agencies, sustainability certification organizations.

- Distribution & Logistics: Industrial distributors, packaging suppliers, specialty chemical distributors, logistics service providers, export-import operators.

- End-Use Utilization: Packaging companies, pharmaceutical manufacturers, food ingredient producers, textile companies, construction material suppliers, consumer goods manufacturers.

Key Value Chain & Supply Chain Evolution Signals in Global Cellulose Market

- Expansion of Sustainable Forestry Practices:

Increasing adoption of certified forestry programs and responsible resource management is strengthening long-term raw material availability and environmental performance. - Rapid Growth of Nanocellulose Technologies:

Advanced nanocellulose materials are enabling new applications across lightweight composites, packaging, electronics, healthcare, and specialty industrial products. - Rising Demand for Sustainable Packaging Solutions:

Growing replacement of conventional plastics with renewable and biodegradable cellulose-based packaging materials is accelerating market expansion. - Increasing Adoption of Cellulose Derivatives:

Pharmaceutical, food, personal care, and specialty chemical industries are expanding the use of value-added cellulose products. - Strengthening Circular Economy Integration:

Recycling initiatives, renewable feedstocks, and waste reduction strategies are becoming critical components of cellulose supply chain management. - Advancement of High-Performance Bio-Based Materials:

Ongoing innovation is improving the strength, functionality, and versatility of cellulose-based products across industrial sectors.

Strategic Implications of Value Chain & Supply Chain Evolution

- Investment in Advanced Cellulose Technologies:

Development of nanocellulose, specialty cellulose derivatives, and high-performance biomaterials will create significant competitive advantages. - Strengthening Sustainable Sourcing Strategies:

Certified forestry operations and renewable feedstock integration are becoming essential for long-term supply chain resilience and regulatory compliance. - Expansion of Value-Added Product Portfolios:

Specialty cellulose products provide opportunities for higher margins and diversification into fast-growing end-use industries. - Enhancing Environmental Compliance Infrastructure:

Sustainability certifications and environmental performance management are increasingly important for customer acquisition and market access. - Development of Circular Production Models:

Resource efficiency, recycling integration, and waste minimization strategies improve operational sustainability and profitability. - Regional Manufacturing & Supply Chain Localization:

Expanding localized production capabilities helps reduce transportation costs, improve responsiveness, and strengthen supply security.

Global Cellulose Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the value chain is expected to evolve into a highly sustainable, innovation-driven, and circular-economy-focused ecosystem supported by advanced biomaterials, renewable resource management, and next-generation cellulose technologies.

Key Future Developments Include:

- Expansion of nanocellulose and advanced cellulose composite production capacities.

- Increased adoption of biodegradable packaging and renewable biomaterial solutions.

- Growth of pharmaceutical and specialty chemical applications for cellulose derivatives.

- Integration of circular economy practices across cellulose manufacturing value chains.

- Expansion of sustainable forestry certification and renewable resource management programs.

- Advancement of high-performance cellulose materials for industrial and consumer applications.

As the market evolves, competitive advantage will increasingly depend on the ability to combine sustainable sourcing, technological innovation, production efficiency, and regulatory compliance. Companies capable of delivering high-performance and environmentally responsible cellulose solutions will be best positioned to capture future growth opportunities.

Organizations that successfully integrate advanced cellulose technologies, sustainable forestry practices, renewable feedstock utilization, and scalable global distribution networks will achieve stronger market positioning, enhanced operational resilience, and long-term success in the Global Cellulose Market.

Investment Activity

Global Cellulose Market Investment & Funding Dynamics Overview

The Global Cellulose Market is witnessing growing investment activity driven by rising demand for sustainable packaging materials, bio-based industrial inputs, advanced cellulose derivatives, and environmentally friendly alternatives to petroleum-based products. Investors, pulp manufacturers, specialty chemical companies, packaging producers, and biomaterial innovators are increasingly allocating capital toward nanocellulose development, sustainable pulp production, biodegradable materials, and circular manufacturing technologies.

The market is benefiting from the global transition toward renewable resources and low-carbon industrial systems. Growing demand for sustainable packaging, pharmaceutical excipients, food additives, regenerated fibers, and high-performance biomaterials is encouraging both private and public sector investments across the cellulose value chain.

Additionally, increasing regulatory support for renewable materials, coupled with corporate sustainability commitments, is accelerating funding for advanced cellulose processing technologies, forestry sustainability programs, and next-generation cellulose applications.

Global Cellulose Market Investment & Funding Dynamics Current Scenario

Current investment trends in the cellulose market are centered on capacity expansion, biomaterial innovation, sustainable sourcing initiatives, and advanced cellulose derivative production. Major industry participants are investing heavily in nanocellulose facilities, specialty cellulose manufacturing plants, biodegradable packaging solutions, and renewable feedstock optimization.

Funding activity is increasing across companies developing microcrystalline cellulose, cellulose composites, cellulose ethers, cellulose acetate products, and bio-based packaging materials. Venture capital and strategic investors are also targeting emerging technologies that enhance cellulose functionality and expand application possibilities.

The industry is witnessing active mergers, acquisitions, and strategic collaborations focused on strengthening supply chains, securing sustainable forestry resources, and accelerating commercialization of advanced cellulose products.

Key Investment & Funding Dynamics Signals in Global Cellulose Market

- Increasing investments in nanocellulose production technologies to support high-performance material applications.

- Growing capital allocation toward biodegradable packaging and sustainable biomaterials.

- Expansion of sustainably certified forestry operations and renewable raw material sourcing.

- Rising funding for specialty cellulose derivatives used in pharmaceuticals, food, and personal care products.

- Strategic partnerships between pulp manufacturers, packaging companies, and biomaterial developers to accelerate innovation.

- Increased investments in circular economy initiatives and low-carbon manufacturing infrastructure.

- Government incentives supporting renewable materials and bio-based industrial development are improving investor confidence.

Strategic Implications of Investment & Funding Dynamics in Global Cellulose Market

- Companies investing in advanced cellulose technologies and sustainable production systems are expected to gain long-term competitive advantages.

- Capital deployment toward nanocellulose, specialty cellulose derivatives, and biodegradable materials will drive future revenue growth.

- Vertical integration across forestry resources, pulp production, and downstream cellulose applications can improve profitability and supply chain resilience.

- Investment in sustainable sourcing certifications and environmental compliance programs will strengthen market acceptance.

- Expansion into high-value pharmaceutical, food, and industrial applications can enhance margin opportunities.

- Strategic collaboration between biomaterial innovators and industrial manufacturers will accelerate commercialization of next-generation cellulose products.

- Organizations focused on circular economy principles and renewable material ecosystems are likely to attract stronger investor interest.

Global Cellulose Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Cellulose Market is expected to experience sustained investment growth driven by increasing demand for bio-based materials, sustainable packaging, renewable industrial inputs, and advanced cellulose technologies.

Future investments will increasingly focus on nanocellulose commercialization, cellulose-based bioplastics, advanced composites, carbon-efficient production technologies, and circular manufacturing ecosystems. Emerging applications across packaging, pharmaceuticals, textiles, construction materials, and specialty chemicals will continue to expand investment opportunities.

The convergence of sustainability goals, regulatory support, biomaterial innovation, and renewable resource utilization is expected to create a favorable environment for long-term capital deployment throughout the cellulose value chain.

In conclusion, the Global Cellulose Market presents a resilient and strategically important investment landscape where sustainable manufacturing, advanced biomaterials, circular economy integration, and high-value cellulose applications will shape future funding priorities and growth opportunities.

Technology & Innovation

Global Cellulose Market Technology & Innovation Landscape Overview

The global cellulose market is experiencing significant technological advancement driven by innovations in nanocellulose engineering, advanced cellulose derivatives, bio-based material processing, sustainable pulp manufacturing, and circular production technologies. Industry participants are increasingly focusing on developing high-performance cellulose materials that offer enhanced functionality, biodegradability, and environmental sustainability across packaging, pharmaceutical, textile, and industrial applications.

Modern cellulose manufacturing systems are integrating advanced fiber processing technologies, enzymatic treatment methods, precision chemical modification techniques, and automated production platforms to improve product quality, operational efficiency, and resource utilization. These innovations are enabling manufacturers to produce specialty cellulose products with improved strength, barrier properties, and application-specific performance characteristics.

The market is also witnessing growing adoption of nanocellulose production technologies, biodegradable composite materials, renewable feedstock optimization systems, and low-emission manufacturing processes that are expanding the commercial potential of cellulose-based products across multiple industries.

Global Cellulose Market Technology & Innovation Current Scenario

Current innovation within the cellulose market is centered on the development of advanced bio-based materials and sustainable production ecosystems. Traditional cellulose applications are evolving toward high-value specialty materials designed to meet growing environmental and performance requirements.

Nanocellulose technologies are gaining significant traction due to their exceptional strength, lightweight characteristics, and potential applications in packaging, electronics, construction materials, and biomedical products.

Advanced cellulose derivatives are increasingly being utilized in pharmaceuticals, food processing, personal care products, and specialty chemical formulations to enhance product functionality and stability.

Manufacturers are investing in closed-loop production systems and sustainable forestry management technologies to improve resource efficiency and support circular economy objectives.

Digital process monitoring and automation technologies are further improving production consistency, quality control, and operational productivity across cellulose manufacturing facilities.

Key Technology & Innovation Trends in Global Cellulose Market

- Nanocellulose Development: Enabling lightweight, high-strength, and sustainable material applications.

- Advanced Cellulose Derivatives: Expanding functionality across pharmaceutical, food, and industrial sectors.

- Biodegradable Packaging Technologies: Supporting the replacement of conventional plastic materials.

- Sustainable Pulp Processing Systems: Improving production efficiency while reducing environmental impact.

- Bio-Based Composite Materials: Enhancing performance in construction, automotive, and consumer products.

- Enzymatic Processing Technologies: Increasing cellulose extraction efficiency and product quality.

- Circular Manufacturing Models: Promoting recycling, waste reduction, and resource optimization.

- Digital Production Automation: Improving operational control and manufacturing consistency.

- Renewable Feedstock Optimization: Strengthening sustainable raw material sourcing strategies.

- High-Performance Functional Cellulose Materials: Creating new opportunities in advanced industrial applications.

Strategic Implications of Technology & Innovation

Technological innovation is reshaping competitive dynamics within the cellulose market by shifting industry focus from conventional pulp products toward high-value, sustainable, and performance-driven cellulose solutions.

Companies investing in nanocellulose research, advanced material engineering, and sustainable manufacturing technologies are strengthening their competitive positioning through product differentiation and expanded application opportunities.

The growing demand for renewable and biodegradable materials is accelerating commercialization of innovative cellulose products across packaging, healthcare, consumer goods, and industrial sectors.

Advanced production technologies are helping manufacturers improve resource efficiency, reduce emissions, and comply with increasingly stringent environmental regulations.

However, high production costs for specialty cellulose products, scalability challenges, and technological complexity remain key barriers for widespread commercialization in certain applications.

Global Cellulose Market Technology & Innovation Forward Outlook

The future of the cellulose market is expected to evolve toward next-generation biomaterials, fully sustainable production ecosystems, and advanced cellulose-based functional products capable of replacing conventional synthetic materials in numerous applications.

Emerging innovations include ultra-high-strength nanocellulose composites, smart biodegradable packaging materials, advanced cellulose-based medical products, and multifunctional bio-derived industrial materials.

Artificial intelligence-driven process optimization, automated manufacturing systems, and precision material engineering are expected to further improve production efficiency and product performance.

The integration of circular economy principles, renewable feedstocks, and low-carbon manufacturing technologies will continue strengthening the environmental value proposition of cellulose-based products.

Overall, the global cellulose market is advancing toward a highly sustainable and innovation-driven ecosystem where advanced cellulose technologies, renewable material solutions, and circular manufacturing models play a central role in shaping future industry growth.

Market Risk

Cellulose Market Risk Factors & Disruption Threats Overview

The global cellulose market operates within a moderately high-risk environment shaped by raw material availability, environmental regulations, evolving sustainability requirements, supply chain dependencies, and technological shifts. While cellulose benefits from strong long-term demand due to its renewable nature and broad industrial applications, market participants face ongoing challenges related to forestry management, energy costs, production economics, and regulatory compliance.

Cellulose production remains heavily dependent on wood pulp and agricultural feedstocks, making the industry vulnerable to fluctuations in forestry resources, climate-related disruptions, and changing land-use policies. Increasing environmental scrutiny regarding deforestation, biodiversity protection, and carbon emissions is also influencing sourcing practices and operational costs.

In addition, the rapid emergence of advanced biomaterials, alternative bio-based polymers, and recycling technologies is reshaping competitive dynamics. Companies must continuously invest in innovation to maintain competitiveness and address evolving customer expectations regarding sustainability and performance.

Although demand fundamentals remain strong across packaging, pharmaceuticals, food processing, and industrial applications, the market faces disruption risks associated with economic volatility, energy price fluctuations, geopolitical uncertainties, and tightening environmental regulations.

Cellulose Market Risk Factors & Disruption Threats Current Scenario

The current cellulose market landscape is characterized by growing demand for sustainable materials alongside increasing regulatory and operational complexities. Global sustainability initiatives continue to support demand for renewable cellulose-based products; however, manufacturers face rising pressure to demonstrate responsible sourcing and environmental stewardship.

Volatility in wood pulp prices remains one of the most significant market risks. Changes in forestry output, transportation costs, labor availability, and weather conditions can directly impact raw material procurement and production economics. Since wood pulp-based cellulose represents the largest market segment, fluctuations in pulp availability can affect supply stability across multiple downstream industries.

Rising energy costs present another challenge, as cellulose manufacturing processes require substantial energy and water consumption. Inflationary pressures and utility cost increases can reduce profitability and force manufacturers to reassess production strategies and capital investment plans.

Regulatory compliance requirements continue to expand globally. Forestry certification programs, carbon reduction initiatives, waste management regulations, and sustainable packaging mandates are increasing operational complexity while creating additional compliance costs for manufacturers.

Furthermore, geopolitical tensions and international trade disruptions continue to influence global supply chains. Export restrictions, transportation bottlenecks, and trade policy changes may affect the movement of pulp, specialty chemicals, and finished cellulose products across international markets.

Key Risk Factors & Disruption Threats Signals in the Cellulose Market

- Raw Material Supply Risk: Dependence on forestry resources and agricultural feedstocks exposes manufacturers to supply shortages, climate-related disruptions, and resource availability challenges.

- Environmental and Sustainability Regulations: Increasing compliance requirements related to forestry management, carbon emissions, biodiversity protection, and waste reduction can raise operational costs.

- Energy Cost Volatility: Cellulose production requires significant energy inputs, making manufacturers vulnerable to electricity, fuel, and utility price fluctuations.

- Supply Chain Disruptions: Global logistics constraints, transportation bottlenecks, geopolitical tensions, and trade restrictions may affect production continuity and delivery schedules.

- Substitution Threats: Competition from recycled materials, alternative biomaterials, synthetic polymers, and emerging sustainable materials could impact demand in specific applications.

- Technological Disruption: Rapid innovation in advanced biomaterials and next-generation sustainable materials may require continuous investment in product development and manufacturing upgrades.

- Pricing Pressure: Competitive market conditions and fluctuations in raw material costs can affect profitability and limit pricing flexibility.

- Climate and Environmental Events: Wildfires, droughts, storms, and other climate-related events may disrupt forestry operations and reduce raw material availability.

Strategic Implications of Risk Factors & Disruption Threats in the Cellulose Market

The evolving risk landscape is reshaping strategic priorities across the cellulose value chain. Manufacturers are increasingly investing in sustainable sourcing programs, certified forestry operations, and circular economy initiatives to strengthen supply security and meet regulatory expectations.

Product innovation has become a critical competitive differentiator. Companies are expanding investments in nanocellulose, microcrystalline cellulose, specialty derivatives, and biodegradable material technologies to create higher-value applications and reduce exposure to commodity market volatility.

Supply chain diversification is also gaining importance as organizations seek to minimize geopolitical and logistics-related disruptions. Strategic partnerships with forestry operators, chemical suppliers, packaging companies, and research institutions are helping improve operational resilience and innovation capabilities.

Capital investment decisions are increasingly influenced by sustainability objectives. Manufacturers are modernizing production facilities, improving energy efficiency, reducing water consumption, and implementing lower-emission manufacturing processes to enhance long-term competitiveness.

Cellulose Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead, sustainability trends are expected to remain the primary growth driver while simultaneously serving as a major source of regulatory and operational complexity. Companies that successfully align production practices with evolving environmental standards will likely achieve stronger market positioning.

Continued expansion of sustainable packaging, bio-based chemicals, pharmaceutical excipients, and advanced cellulose materials is expected to create substantial growth opportunities. However, securing reliable feedstock supplies and managing production costs will remain essential for long-term success.

Emerging technologies such as nanocellulose, cellulose composites, and advanced biomaterials are likely to introduce new competitive dynamics. Companies that invest in research, commercialization capabilities, and intellectual property development may gain significant advantages in high-growth application segments.

Climate-related risks and resource sustainability concerns will increasingly influence investment decisions, regulatory frameworks, and corporate procurement strategies. As a result, supply chain transparency and certified sustainable sourcing are expected to become critical competitive requirements across the industry.

Overall, the global cellulose market is expected to maintain steady growth despite a moderately high-risk operating environment. Organizations that prioritize innovation, sustainability, operational efficiency, and supply chain resilience will be best positioned to navigate future disruption risks and capitalize on emerging opportunities.

Regulatory Landscape

Global Cellulose Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global cellulose market is shaped by forestry sustainability standards, environmental protection regulations, bio-based material compliance frameworks, waste reduction policies, and circular economy initiatives. As cellulose is a renewable and biodegradable material derived primarily from plant-based sources, regulatory authorities increasingly recognize its strategic role in supporting sustainable manufacturing, reducing dependence on fossil-based materials, and advancing environmental objectives across multiple industries.

Cellulose manufacturers, pulp producers, packaging companies, and downstream industrial users must comply with a broad range of regulations covering sustainable forest management, responsible raw material sourcing, emissions control, wastewater treatment, product safety standards, and environmental reporting requirements. These regulations significantly influence sourcing strategies, production processes, and market access across global regions.

The growing adoption of biodegradable packaging, bio-based chemicals, advanced cellulose derivatives, and nanocellulose technologies is further driving the development of regulatory frameworks that encourage renewable material innovation while ensuring environmental sustainability and supply chain transparency.

Global Cellulose Market Regulatory & Policy Environment Current Scenario

The current regulatory framework for the cellulose market combines forestry governance policies, environmental compliance requirements, industrial sustainability mandates, and product certification standards governing renewable material production and utilization.

In North America and Europe, stringent forestry certification programs such as FSC (Forest Stewardship Council) and PEFC (Programme for the Endorsement of Forest Certification) play a critical role in ensuring sustainable sourcing of wood pulp and cellulose feedstocks. Compliance with these standards is increasingly becoming a prerequisite for participation in global supply chains.

Environmental regulations governing air emissions, wastewater discharge, chemical processing, and energy consumption are encouraging cellulose manufacturers to adopt cleaner production technologies and resource-efficient manufacturing systems. Regulatory agencies are also promoting reduced carbon footprints and improved environmental performance throughout the pulp and cellulose value chain.

Asia-Pacific markets, including China, India, Japan, and Southeast Asian countries, are strengthening environmental oversight while simultaneously supporting industrial expansion and bio-based material development. Governments are encouraging investments in sustainable pulp production, advanced cellulose processing, and circular manufacturing models to balance economic growth with environmental protection.

In addition, packaging and consumer goods industries increasingly face regulations aimed at reducing plastic waste, creating favorable conditions for cellulose-based alternatives and biodegradable packaging solutions.

Key Regulatory & Policy Environment Signals in Global Cellulose Market

- Forestry Sustainability Standards: Certified forest management practices are becoming essential for responsible cellulose feedstock sourcing.

- Environmental Compliance Regulations: Emission controls, wastewater management, and resource efficiency requirements are shaping production strategies.

- Bio-Based Material Policies: Governments are promoting renewable and biodegradable material adoption across industrial sectors.

- Circular Economy Initiatives: Regulatory frameworks encourage recycling, waste reduction, and sustainable material utilization.

- Packaging Sustainability Mandates: Restrictions on single-use plastics are accelerating demand for cellulose-based alternatives.

- Product Certification Requirements: Compliance with environmental labeling and sustainability certifications supports market access and consumer trust.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging cellulose producers to invest heavily in sustainable forestry partnerships, advanced processing technologies, low-emission manufacturing systems, and environmentally responsible supply chain management practices. Companies with strong sustainability credentials are increasingly positioned to secure long-term customer relationships and premium market opportunities.

Environmental regulations are accelerating adoption of energy-efficient pulp processing systems, water recycling technologies, biomass energy integration, and carbon reduction initiatives. These investments are helping manufacturers improve operational efficiency while meeting stricter environmental performance requirements.

Growing regulatory support for bio-based materials is driving innovation in cellulose derivatives, nanocellulose products, biodegradable packaging materials, and advanced biomaterial applications. This is expanding the commercial potential of cellulose across high-growth sectors including pharmaceuticals, food ingredients, personal care products, and sustainable construction materials.

Circular economy policies are also encouraging greater collaboration across the value chain to improve material recovery, recycling infrastructure, and resource optimization. As a result, manufacturers are increasingly integrating sustainability objectives into product development and business strategy.

Companies capable of demonstrating sustainable sourcing, regulatory compliance, and environmental stewardship are expected to gain competitive advantages as sustainability requirements become increasingly important across global markets.

Global Cellulose Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global cellulose market is expected to become increasingly focused on climate objectives, sustainable resource management, and bioeconomy development. Governments worldwide are likely to strengthen environmental performance requirements while expanding support for renewable and biodegradable materials.

Stricter carbon reduction targets, enhanced forest conservation policies, and broader circular economy regulations are expected to influence both upstream raw material sourcing and downstream product applications. Sustainable cellulose production will increasingly become a strategic priority within industrial decarbonization efforts.

Packaging regulations aimed at reducing plastic waste are likely to accelerate the adoption of cellulose-based alternatives across consumer goods, food packaging, and e-commerce sectors. Advanced cellulose materials such as nanocellulose may also benefit from growing policy support for innovative sustainable technologies.

International harmonization of sustainability certifications, environmental reporting frameworks, and responsible sourcing standards is expected to improve transparency and facilitate global trade in cellulose-based products.

Overall, regulatory and policy developments will remain a key growth catalyst for the cellulose market, with companies investing in sustainable sourcing, advanced biomaterial innovation, environmental compliance, and circular production systems expected to maintain long-term competitive advantage.