Global Isobutanol Market Report, Size, Share and Forecast 2026–2033

Global Isobutanol Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

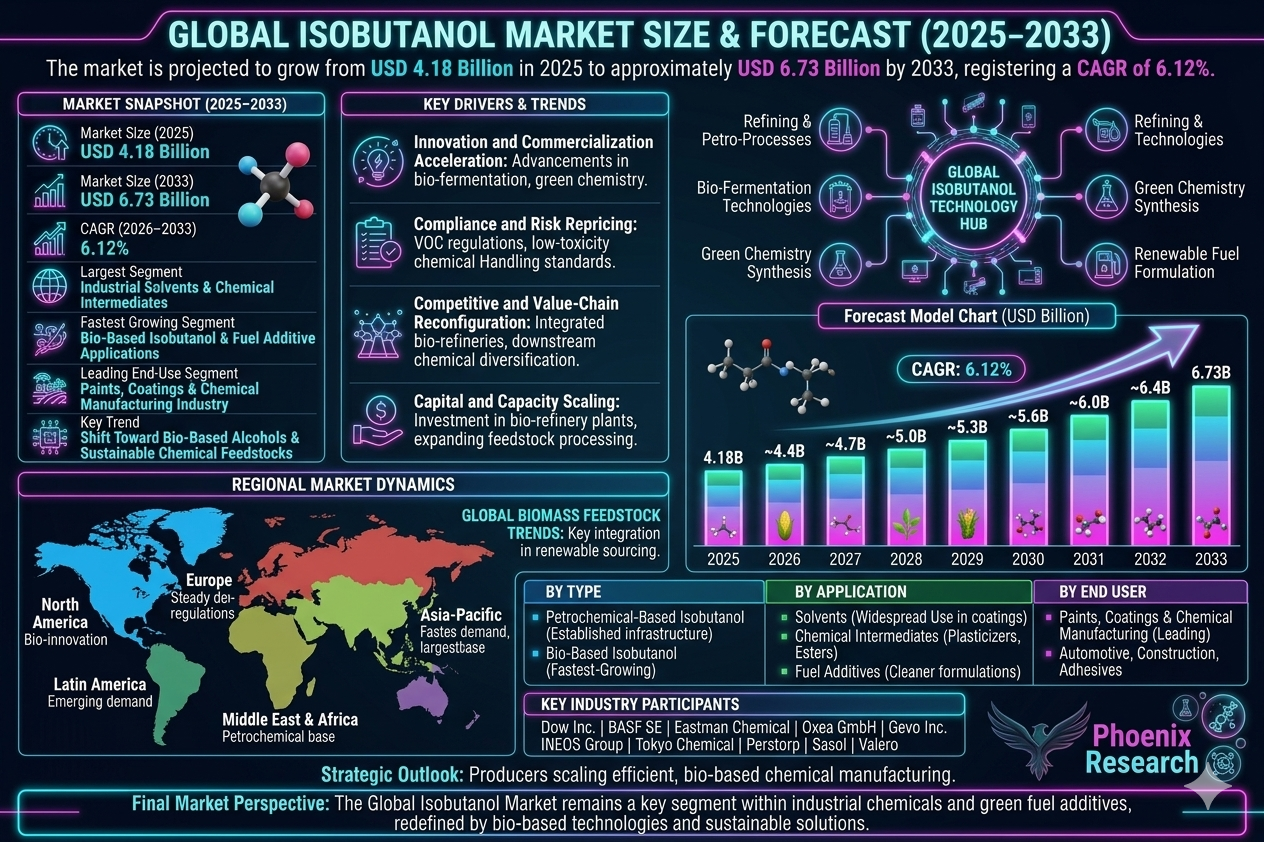

| Market Size (2025) | USD 4.18 Billion |

| Market Size (2033) | USD 6.73 Billion |

| CAGR (2026???2033) | 6.12% |

| Largest Segment | Industrial Solvents & Chemical Intermediates |

| Fastest Growing Segment | Bio-Based Isobutanol & Fuel Additive Applications |

| Leading End-Use Segment | Paints, Coatings & Chemical Manufacturing Industry |

| Key Trend | Shift Toward Bio-Based Alcohols & Sustainable Chemical Feedstocks |

| Regulatory Influence | VOC Emission Regulations, Environmental Compliance & Industrial Safety Standards |

| Future Outlook | Growth Driven by Sustainable Chemicals, Fuel Additives & Industrial Solvent Demand |

Global Isobutanol Market size & forecast

The Global Isobutanol Market is expected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at USD 4.18 billion in 2025 and is projected to reach approximately USD 6.73 billion by 2033, registering a CAGR of 6.12%. The market growth is primarily driven by increasing demand for industrial solvents, expanding use in chemical intermediates, rising adoption in fuel additives, and growing preference for bio-based chemical alternatives. Isobutanol is an important industrial alcohol used in coatings, paints, plasticizers, fuel formulations, and chemical synthesis. Its versatility as a solvent and intermediate is driving adoption across multiple industries. In addition, rising environmental regulations and the shift toward low-VOC and bio-based chemicals are supporting long-term market expansion.Global Isobutanol Market Overview

Isobutanol is a four-carbon branched alcohol widely used as a solvent, chemical intermediate, and fuel additive component. The market includes petrochemical-derived isobutanol and bio-based isobutanol, serving applications across coatings, adhesives, pharmaceuticals, plastics, and energy sectors. The product is widely utilized in paints and coatings, plasticizers, lubricants, gasoline additives, and specialty chemicals manufacturing. The market is shifting toward sustainable production methods, bio-fermentation technologies, and environmentally friendly chemical processes.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Advancements in bio-fermentation processes, catalytic production technologies, and green chemistry are enhancing production efficiency and sustainability. Improved chemical engineering processes are enabling higher purity and cost-efficient production methods.Market Implications

Companies investing in bio-based production technologies and low-emission chemical processes are expected to strengthen market competitiveness.2. Compliance and Risk Repricing

VOC emission regulations, environmental safety standards, and chemical handling policies are influencing production methods and formulation strategies. Governments are encouraging adoption of low-toxicity and sustainable chemical alternatives.Market Implications

Firms offering compliant, low-emission, and sustainable isobutanol solutions are likely to gain stronger regulatory and industrial acceptance.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as chemical manufacturers, biofuel companies, and specialty chemical producers expand production capacities. Integration of renewable feedstocks and circular chemical production models is reshaping value chains.Market Implications

Companies focusing on bio-based integration and downstream chemical diversification may gain stronger margins.4. Capital and Capacity Scaling

Rising investment in bio-refineries, chemical production plants, and sustainable feedstock processing is supporting market expansion. Expanding demand from coatings, energy, and industrial manufacturing sectors is increasing production capacity requirements.Market Implications

Producers scaling efficient and sustainable chemical manufacturing facilities are expected to capture future opportunities.Market Segmentation Analysis

By Type

1. Petrochemical-Based Isobutanol

This remains the largest segment due to established production infrastructure and cost efficiency.2. Bio-Based Isobutanol

Fastest-growing segment driven by sustainability and renewable chemical demand.By Application

1. Solvents

Largest segment due to widespread use in coatings and industrial formulations.2. Chemical Intermediates

Used in plasticizers, esters, and specialty chemical production.3. Fuel Additives

Growing demand driven by cleaner fuel formulations.4. Coatings & Paints

Strong demand due to industrial and construction activities.5. Pharmaceuticals & Others

Used in niche synthesis and specialty applications.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global isobutanol market due to strong chemical manufacturing base, industrial expansion, and rising coatings demand.North America

North America shows strong growth driven by bio-based chemical innovation and fuel additive applications.Europe

Europe is witnessing steady demand supported by environmental regulations and sustainable chemical adoption.Latin America

Latin America is gradually expanding due to industrial growth and coatings demand.Middle East & Africa

The region is emerging with growth driven by petrochemical investments and industrial diversification.Competitive Landscape

The Global Isobutanol Market is highly competitive with chemical manufacturers and bio-based production companies operating globally.Key Companies Operating in the Market Include:

- Dow Inc.

- BASF SE

- Eastman Chemical Company

- Oxea GmbH

- Gevo Inc.

- INEOS Group

- Tokyo Chemical Industry Co.

- Perstorp Holding AB

- Sasol Limited

- Valero Energy Corporation

Strategic Outlook

The future of the isobutanol market will be shaped by bio-based production technologies, sustainable chemical innovation, and expansion of green fuel additives. Advanced fermentation processes and renewable feedstock integration will significantly improve environmental performance and cost efficiency. The rise of low-VOC coatings, sustainable chemicals, and bio-refineries is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Isobutanol Market remains a key segment within industrial chemicals, coatings, and sustainable fuel ecosystems. Rising demand for solvents, green chemicals, and industrial intermediates continues driving long-term market growth. Companies capable of delivering efficient, sustainable, and innovative chemical solutions will be best positioned to capture future opportunities. The convergence of bio-based chemistry, industrial demand, and environmental regulations is expected to redefine the future of the global isobutanol industry.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Isobutanol Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Overview

- 1.3 Key Growth Segments Overview

- 1.4 Regional Highlights

- 1.5 Major Market Drivers

- 1.6 Competitive Landscape Summary

- 1.7 Strategic Outlook

- 2. Market Introduction & Overview

- 2.1 Definition of Isobutanol Market

- 2.2 Scope and Market Coverage

- 2.3 Evolution of Industrial Alcohols

- 2.4 Role of Isobutanol in Industrial Ecosystems

- 2.5 Regulatory & Environmental Framework Overview

- 2.6 Transition Toward Bio-Based Chemicals

- 3. Research Methodology

- 3.1 Data Collection Approach

- 3.2 Market Estimation Model

- 3.3 Forecasting Assumptions (2026???2033)

- 3.4 Data Validation Techniques

- 3.5 Limitations & Considerations

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Demand for Industrial Solvents

- 4.1.2 Expansion of Chemical Intermediate Applications

- 4.1.3 Growth in Fuel Additive Usage

- 4.1.4 Shift Toward Bio-Based Chemical Alternatives

- 4.1.5 Increasing Paints & Coatings Demand

- 4.2 Restraints

- 4.2.1 Volatility in Petrochemical Feedstock Prices

- 4.2.2 Environmental Compliance Costs

- 4.2.3 Competition from Alternative Alcohols

- 4.3 Opportunities

- 4.3.1 Bio-Based Isobutanol Development

- 4.3.2 Low-VOC Coatings Expansion

- 4.3.3 Renewable Feedstock Integration

- 4.3.4 Green Fuel Additive Innovation

- 4.4 Challenges

- 4.4.1 Scaling Bio-Fermentation Technologies

- 4.4.2 Regulatory Compliance Complexity

- 4.4.3 Market Competition from Established Alcohols

- 4.1 Drivers

- 5. Global Isobutanol Market Size & Forecast (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Trend Analysis

- 5.3 Demand Growth Patterns

- 5.4 Application-wise Revenue Trends

- 5.5 Future Market Outlook

- 6. Market Segmentation Analysis (USD Billion), 2026???2033

- 6.1 By Type

- 6.1.1 Petrochemical-Based Isobutanol

- 6.1.2 Bio-Based Isobutanol (Fastest Growing)

- 6.2 By Application

- 6.2.1 Solvents (Largest Segment)

- 6.2.2 Chemical Intermediates

- 6.2.3 Fuel Additives

- 6.2.4 Coatings & Paints

- 6.2.5 Pharmaceuticals & Others

- 6.1 By Type

- 7. Regional Market Analysis

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Overview

- 8.2 Key Player Strategies

- 8.3 Capacity Expansion Analysis

- 8.4 Bio-Based Investment Trends

- 9. Company Profiles

- 9.1 Dow Inc.

- 9.2 BASF SE

- 9.3 Eastman Chemical Company

- 9.4 Oxea GmbH

- 9.5 Gevo Inc.

- 9.6 INEOS Group

- 9.7 Tokyo Chemical Industry Co.

- 9.8 Perstorp Holding AB

- 9.9 Sasol Limited

- 9.10 Valero Energy Corporation

- 10. Strategic Insights

- 10.1 Bio-Based Chemical Transition Analysis

- 10.2 Low-VOC Regulatory Impact Study

- 10.3 Green Chemistry Innovation Trends

- 10.4 Supply Chain & Feedstock Optimization

- 11. Future Outlook & Recommendations

- 11.1 Expansion of Bio-Based Production

- 11.2 Investment in Sustainable Chemical Manufacturing

- 11.3 Integration of Renewable Feedstocks

- 11.4 Market Diversification Strategies

- 11.5 Long-Term Outlook (2033+)

- 12. Appendix

- 13. Disclaimer

Competitive Landscape

Global Isobutanol Market Competitive Intensity & Market Structure Overview

The global isobutanol market is moderately consolidated, with a mix of large multinational chemical companies and emerging bio-based chemical producers. Competitive intensity is shaped by feedstock availability, production efficiency, cost structures, regulatory compliance with VOC emission standards, and the ability to scale sustainable and bio-based production technologies.

The market structure is dominated by established petrochemical producers that benefit from integrated refining and large-scale manufacturing capabilities, alongside a growing cohort of green chemistry innovators focusing on bio-based isobutanol production. This dual structure is gradually reshaping competitive dynamics as sustainability transitions gain momentum.

Rising demand from coatings, paints, industrial solvents, and fuel additive applications is intensifying competition, particularly as end-users increasingly prefer low-VOC and environmentally compliant chemical solutions. This is pushing manufacturers toward process innovation and feedstock diversification.

Global Isobutanol Market Competitive Intensity & Market Structure Current Scenario

Leading Global Isobutanol Companies

Dow Inc.: Major global chemical producer with strong integration across industrial solvents and intermediates, leveraging scale and diversified downstream applications.

BASF SE: Leading diversified chemical company focused on high-performance solvents, intermediates, and sustainable chemical innovation.

Eastman Chemical Company: Key player specializing in performance chemicals and solvent applications across coatings and industrial segments.

Oxea GmbH: Major producer of oxo alcohols, including isobutanol, with strong expertise in industrial chemical manufacturing.

Gevo Inc.: Fast-growing bio-based chemical company focusing on renewable isobutanol and sustainable fuel applications.

INEOS Group: Large-scale petrochemical manufacturer with integrated production systems supporting solvent and intermediate markets.

Tokyo Chemical Industry Co.: Specialty chemical supplier with niche applications in research-grade and industrial chemicals.

Perstorp Holding AB: Strong player in specialty chemicals and sustainable solutions, including ester-based derivatives.

Sasol Limited: Integrated energy and chemical company with significant production capacity in alcohols and industrial chemicals.

Valero Energy Corporation: Energy and refining company involved in biofuel-linked chemical production and feedstock integration.

Key Competitive Intensity & Market Structure Drivers

Shift toward bio-based isobutanol is increasing competitive pressure on traditional petrochemical producers to invest in sustainable production technologies.

Stricter VOC emission regulations are driving product reformulation and accelerating demand for low-toxicity solvent alternatives.

Expansion of coatings, adhesives, and fuel additive industries is intensifying demand-side competition across global supply chains.

Technological advancements in fermentation and catalytic production are creating new entry opportunities for bio-chemical innovators.

Vertical integration across chemical feedstocks and downstream applications is becoming a key competitive advantage.

Strategic Implications of Competitive Intensity & Market Structure

Companies investing in bio-refining capabilities and green chemistry platforms are expected to gain long-term strategic advantage as regulatory pressure increases.

Cost leadership through integrated petrochemical operations remains a critical differentiator for established market players.

Strategic partnerships between traditional chemical firms and biotech innovators are accelerating commercialization of bio-based isobutanol.

Expansion into fuel additives and sustainable coatings applications is improving revenue diversification opportunities.

Digital process optimization and advanced manufacturing automation are enhancing production efficiency and reducing operational costs.

Global Isobutanol Market Competitive Intensity & Market Structure Forward Outlook

The global isobutanol market is expected to become increasingly sustainability-driven, with bio-based production gradually gaining share over petrochemical-derived supply. Competitive intensity will rise as regulatory frameworks tighten and demand shifts toward low-emission chemical solutions.

Future competition will be defined by technological leadership in bio-fermentation, carbon-efficient manufacturing, and integration of renewable feedstocks into large-scale production systems.

Asia-Pacific is expected to remain the dominant production hub, while North America and Europe will lead in bio-based innovation and regulatory-driven adoption of sustainable chemicals.

Over the forecast period, companies that successfully balance cost efficiency, regulatory compliance, and sustainable innovation will be best positioned to capture value in the evolving global isobutanol market.

Value Chain

Global Isobutanol Market Value Chain & Supply Chain Evolution Overview

The Global Isobutanol Market is undergoing significant transformation driven by growing demand for industrial solvents, sustainable chemical feedstocks, fuel additives, and environmentally compliant manufacturing processes. The market???s value chain is characterized by a highly integrated chemical production ecosystem that connects feedstock suppliers, chemical manufacturers, bio-refineries, distributors, industrial processors, and end-use industries. This interconnected structure is reshaping production economics, supply chain strategies, and competitive positioning across the global isobutanol industry.

A defining feature of the value chain is the increasing convergence of traditional petrochemical production with renewable bio-based manufacturing technologies. While petrochemical-derived isobutanol continues to dominate global supply, investments in bio-fermentation technologies, renewable feedstocks, and sustainable chemical production methods are accelerating the transition toward greener alternatives. This shift is creating new opportunities for manufacturers to address regulatory requirements and sustainability objectives.

Supply chain complexity is increasing as producers manage feedstock sourcing, chemical processing, transportation logistics, environmental compliance, and downstream industrial integration. Manufacturers must balance raw material availability, production efficiency, cost competitiveness, and sustainability targets while ensuring reliable supply to coatings, chemical intermediates, fuel additive, and specialty chemical markets.

Industry participants are increasingly investing in bio-refineries, process optimization technologies, renewable feedstock integration, and regional production expansion to improve operational efficiency and supply chain resilience. The value chain is evolving into a more sustainable, technology-driven, and vertically integrated ecosystem focused on long-term environmental and economic performance.

Global Isobutanol Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Feedstock Sourcing: Crude oil derivatives, propylene, synthesis gas, agricultural biomass, corn-based feedstocks, sugar-based feedstocks, and renewable raw materials.

- Production & Processing: Petrochemical synthesis, catalytic conversion processes, bio-fermentation technologies, purification, and chemical refining operations.

- Technology Integration: Advanced fermentation systems, process automation, catalytic optimization, carbon reduction technologies, and renewable feedstock processing.

- Regulatory & Compliance Management: VOC emission compliance, environmental regulations, chemical safety standards, transportation regulations, and sustainability certification programs.

- Distribution & Logistics: Bulk chemical transportation, storage terminals, industrial distributors, direct supply agreements, and export-import networks.

- End-Use Utilization: Paints and coatings manufacturers, chemical producers, fuel blending companies, plasticizer manufacturers, pharmaceutical companies, and industrial processing facilities.

Company-to-Stage Mapping

- Feedstock Sourcing: Oil & gas suppliers, petrochemical feedstock providers, agricultural biomass producers, renewable feedstock suppliers.

- Production & Processing: Dow Inc., BASF SE, Oxea GmbH, Eastman Chemical Company, INEOS Group.

- Technology Integration: Gevo Inc., Perstorp Holding AB, bio-refinery technology developers, industrial process engineering companies.

- Regulatory & Compliance Management: Environmental regulatory agencies, chemical safety authorities, sustainability certification organizations.

- Distribution & Logistics: Chemical distributors, bulk storage operators, industrial logistics providers, global trading companies.

- End-Use Utilization: Coatings manufacturers, specialty chemical producers, fuel additive suppliers, plastics manufacturers, pharmaceutical companies.

Key Value Chain & Supply Chain Evolution Signals in Global Isobutanol Market

- Expansion of Bio-Based Isobutanol Production:

Growing investments in renewable feedstocks and fermentation technologies are accelerating the commercialization of sustainable isobutanol production. - Rising Demand for Sustainable Chemical Feedstocks:

Industrial users are increasingly seeking low-carbon and environmentally friendly chemical alternatives to support sustainability goals. - Growth of Fuel Additive Applications:

Isobutanol adoption as a fuel blending component is increasing due to its favorable performance characteristics and compatibility with cleaner fuel initiatives. - Integration of Advanced Manufacturing Technologies:

Automation, process optimization, and catalytic innovations are improving production efficiency and reducing operating costs. - Increasing Regulatory Focus on VOC Reduction:

Environmental regulations are encouraging the use of cleaner solvents and sustainable chemical production methods across industrial sectors. - Strengthening Vertical Integration Strategies:

Chemical manufacturers are expanding feedstock control and downstream product integration to improve supply chain resilience and profitability.

Strategic Implications of Value Chain & Supply Chain Evolution

- Investment in Bio-Refinery Infrastructure:

Expansion of renewable production capacity will support long-term sustainability objectives and reduce dependence on fossil-based feedstocks. - Optimization of Feedstock Diversification:

Access to multiple feedstock sources enhances supply security and mitigates raw material price volatility. - Expansion of Sustainable Product Portfolios:

Bio-based isobutanol solutions provide opportunities to address growing demand for environmentally compliant industrial chemicals. - Strengthening Environmental Compliance Capabilities:

Regulatory compliance and sustainability certifications are becoming increasingly important for market access and customer retention. - Development of Integrated Chemical Value Chains:

Vertical integration across production and downstream applications improves operational efficiency and profit margins. - Regional Manufacturing & Supply Chain Localization:

Localized production facilities improve responsiveness, reduce transportation risks, and strengthen regional market competitiveness.

Global Isobutanol Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the value chain is expected to evolve into a highly sustainable, technology-driven, and renewable-feedstock-integrated ecosystem supported by advancements in green chemistry and industrial decarbonization initiatives.

Key Future Developments Include:

- Expansion of commercial-scale bio-based isobutanol production facilities.

- Increased integration of renewable feedstocks into chemical manufacturing processes.

- Growth of low-VOC coatings and sustainable industrial solvent applications.

- Advancement of fermentation technologies and process optimization systems.

- Expansion of fuel additive demand supporting cleaner transportation fuels.

- Greater adoption of circular economy and carbon reduction strategies across chemical value chains.

As the market evolves, competitive advantage will increasingly depend on the ability to combine production efficiency, sustainability performance, feedstock flexibility, and regulatory compliance. Companies capable of balancing cost competitiveness with environmental responsibility will be better positioned to capture future growth opportunities.

Organizations that successfully integrate bio-based production technologies, renewable feedstock sourcing, advanced manufacturing capabilities, and scalable global distribution networks will achieve stronger market positioning, operational resilience, and long-term success in the Global Isobutanol Market.

Investment Activity

Global Isobutanol Market Investment & Funding Dynamics Overview

The Global Isobutanol Market is attracting steady investment interest driven by rising demand for industrial solvents, chemical intermediates, fuel additives, and the accelerating transition toward bio-based and low-VOC chemical solutions. Chemical manufacturers, bio-refinery developers, and specialty chemical firms are increasingly allocating capital toward green chemistry innovation, production capacity expansion, and sustainable feedstock integration.

Investor focus is strengthening around bio-based isobutanol production technologies, catalytic process optimization, and renewable feedstock-based manufacturing systems. At the same time, regulatory pressure on VOC emissions and industrial safety compliance is pushing capital toward cleaner and more efficient production pathways.

The market is also experiencing growing strategic investment in fuel additive applications, coatings-grade chemical optimization, and integrated chemical value chains, particularly in regions with strong industrial and petrochemical infrastructure.

Global Isobutanol Market Investment & Funding Dynamics Current Scenario

Currently, investment activity in the isobutanol market is centered on capacity expansion, bio-based chemical innovation, and process modernization. Major chemical producers are investing in next-generation fermentation technologies, carbon-efficient production routes, and low-emission manufacturing systems.

Venture capital and corporate funding are increasingly targeting bio-based chemical startups, renewable fuel additive developers, and sustainable industrial solvent innovators. Strategic partnerships between petrochemical companies and biotechnology firms are becoming more common as the industry transitions toward hybrid production models.

In addition, mergers and acquisitions are rising as large chemical players seek to strengthen their portfolios in sustainable solvents, specialty alcohols, and green intermediates.

Key Investment & Funding Dynamics Signals in Global Isobutanol Market

- Rising investments in bio-based isobutanol production technologies driven by sustainability mandates.

- Growing capital deployment into low-VOC and environmentally compliant chemical manufacturing.

- Expansion of bio-refinery infrastructure and renewable feedstock processing systems.

- Increasing funding for fuel additive innovation and cleaner combustion solutions.

- Strategic collaborations between chemical giants and biotech firms for fermentation-based production.

- Rising M&A activity in specialty alcohols and industrial solvent segments.

- Government-supported investments in sustainable chemical manufacturing and green industrial transitions.

Strategic Implications of Investment & Funding Dynamics in Global Isobutanol Market

- Companies investing in bio-based production and low-emission technologies are expected to gain long-term competitive advantage.

- Integration of renewable feedstocks and circular chemical production models will improve cost efficiency and sustainability performance.

- Capital allocation toward fuel additives and coatings-grade chemical innovation will support diversified revenue streams.

- Firms aligned with VOC compliance and environmental regulations will achieve stronger market acceptance.

- Expansion of bio-refinery capacity and advanced fermentation systems will define future supply leadership.

- Strategic partnerships across chemical and biotechnology sectors will accelerate commercialization of green isobutanol.

Global Isobutanol Market Investment & Funding Dynamics Forward Outlook

Over the forecast period, the Global Isobutanol Market is expected to witness sustained investment growth driven by sustainability mandates, industrial demand expansion, and the transition toward bio-based chemical production systems.

Future capital deployment will increasingly focus on advanced bio-fermentation technologies, green hydrogen integration in chemical processing, carbon-efficient production systems, and scalable bio-refinery networks.

The convergence of regulatory pressure, industrial demand, and sustainable chemistry innovation will continue to reshape investment priorities across the global chemical sector.

In conclusion, the Global Isobutanol Market presents a structurally evolving investment landscape where bio-based innovation, regulatory compliance, and industrial efficiency will define long-term capital allocation and growth opportunities.

Technology & Innovation

Global Isobutanol Market Technology & Innovation Landscape Overview

The global isobutanol market is experiencing a structural technological shift driven by advancements in bio-based fermentation technologies, catalytic conversion processes, green chemistry innovations, low-VOC formulation development, and renewable feedstock integration systems. These innovations are reshaping production methods and enabling a transition toward more sustainable and environmentally compliant industrial alcohol manufacturing.

Modern isobutanol production systems are increasingly incorporating advanced bioreactor designs, high-efficiency fermentation strains, process intensification techniques, and automated chemical synthesis platforms to improve yield efficiency, reduce energy consumption, and lower production costs. These developments are particularly important for scaling bio-based isobutanol production in response to rising sustainability demand.

The market is also witnessing growing adoption of integrated bio-refinery models, AI-driven process optimization systems, continuous production technologies, and carbon-efficient chemical manufacturing platforms that are helping producers enhance operational performance while meeting strict environmental regulations.

Global Isobutanol Market Technology & Innovation Current Scenario

Currently, innovation in the isobutanol market is focused on improving production sustainability, feedstock flexibility, and emission reduction efficiency. Traditional petrochemical production remains dominant, but bio-based production technologies are rapidly gaining traction due to regulatory pressure and shifting end-user preferences.

Bio-fermentation technologies are emerging as a key innovation driver, enabling the production of renewable isobutanol using sugar-based, biomass-based, or waste-derived feedstocks. These methods are increasingly preferred for their lower carbon footprint and reduced dependency on fossil fuels.

Catalytic production advancements are also improving petrochemical-based isobutanol manufacturing by enhancing reaction efficiency, increasing selectivity, and reducing unwanted by-products. These improvements help lower production costs while improving output quality.

Additionally, digital process control systems are enabling real-time monitoring of reaction conditions, improving consistency, safety, and scalability across industrial production facilities.

Key Technology & Innovation Trends in the Global Isobutanol Market

- Bio-Fermentation Production Systems: Enabling renewable and low-carbon isobutanol manufacturing using biological feedstocks.

- Advanced Catalytic Conversion Technologies: Improving yield efficiency and reducing production waste in petrochemical processes.

- Green Chemistry Integration: Supporting low-VOC, environmentally friendly chemical formulations.

- AI-Based Process Optimization: Enhancing operational efficiency through predictive analytics and automated control systems.

- Integrated Bio-Refinery Models: Combining multiple renewable chemical production streams for improved efficiency.

- Continuous Production Systems: Increasing scalability and reducing batch-processing inefficiencies.

- Carbon Emission Reduction Technologies: Supporting compliance with environmental regulations and sustainability targets.

- Renewable Feedstock Utilization: Expanding use of biomass, agricultural waste, and sugar-based inputs.

- Digital Twin Chemical Plant Modeling: Optimizing production performance through simulation and predictive analysis.

- Automated Chemical Process Control: Improving safety, consistency, and production efficiency.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the isobutanol market by shifting production from conventional petrochemical dependency toward sustainable, bio-based, and digitally optimized chemical manufacturing systems.

Companies investing in bio-based production infrastructure, green chemistry technologies, and advanced process automation are gaining strong competitive advantages through improved regulatory compliance, lower environmental impact, and enhanced cost efficiency.

The convergence of biotechnology, chemical engineering, and digital manufacturing is enabling the development of next-generation isobutanol production systems that support both industrial demand and sustainability objectives.

However, high capital investment requirements, scalability challenges in bio-production, and feedstock supply constraints remain key barriers affecting rapid commercialization in some regions.

Global Isobutanol Market Technology & Innovation Forward Outlook

The future of the isobutanol market is expected to evolve toward fully sustainable, bio-integrated, and digitally optimized chemical production ecosystems that prioritize low emissions, high efficiency, and renewable resource utilization.

Emerging innovations are likely to include next-generation engineered microbial strains, hybrid petro-bio production systems, AI-driven autonomous chemical plants, and fully circular carbon chemical manufacturing models.

Advanced bio-refinery networks will play a key role in scaling renewable isobutanol production, while digitalization will enhance operational intelligence and reduce production variability.

Overall, the isobutanol market is transitioning toward a high-efficiency, low-carbon chemical ecosystem powered by biotechnology, process automation, green chemistry, and renewable feedstock innovation, redefining the future of global industrial alcohol production.

Market Risk

Global Isobutanol Market Risk & Disruption Analysis

The Global Isobutanol Market operates within a structurally evolving chemical and energy ecosystem shaped by regulatory tightening, feedstock volatility, sustainability transitions, and shifting downstream industrial demand. While the market benefits from growing applications in solvents, coatings, fuel additives, and chemical intermediates, it remains exposed to price fluctuations, regulatory constraints, and technology-driven substitution risks.

A core structural feature of the market is its dependence on petrochemical cycles, industrial manufacturing activity, and increasingly, renewable chemical innovation. Profitability is strongly influenced by raw material costs, production efficiency, environmental compliance requirements, and demand stability from coatings, plastics, and fuel sectors.

The industry is undergoing a gradual transition from conventional petrochemical-based production toward bio-based isobutanol and low-emission manufacturing systems, creating both long-term opportunities and short-term disruption risks related to cost, scalability, and infrastructure readiness.

Current Risk Environment

The isobutanol market is exposed to a multi-layered risk environment spanning raw material volatility, regulatory pressure, and competitive substitution dynamics.

Feedstock price volatility remains a primary risk factor, as isobutanol production is closely linked to upstream oil, gas, and chemical intermediates markets. Fluctuations in crude oil prices directly impact production economics and margin stability.

Environmental and VOC emission regulations are increasingly influencing production processes and product formulation. Compliance with strict air quality standards and chemical safety rules is raising operational costs and accelerating the shift toward cleaner production technologies.

Technological substitution risk is also emerging, as alternative bio-based solvents and next-generation green chemicals compete with isobutanol in coatings, adhesives, and fuel additive applications.

Demand cyclicality from key end-use industries such as paints, coatings, and construction further adds volatility, particularly during periods of macroeconomic slowdown or industrial contraction.

Key Risk & Disruption Factors

- Feedstock Price Volatility: Dependence on petrochemical inputs creates exposure to oil and gas market fluctuations.

- Regulatory Pressure (VOC & Emissions): Tightening environmental laws increase compliance and reformulation costs.

- Bio-Based Transition Risk: Shift toward renewable chemicals may disrupt conventional production economics.

- Industrial Demand Cyclicality: Construction, coatings, and manufacturing cycles impact consumption patterns.

- Technology Substitution: Alternative green solvents may replace isobutanol in certain applications.

- Capital Intensity Risk: Bio-based production requires significant investment and scaling capability.

- Supply Chain Sensitivity: Chemical logistics and storage constraints impact distribution efficiency.

- Margin Pressure: High competition among chemical producers limits pricing flexibility.

Strategic Implications of Market Risk & Disruption

The evolving risk environment is accelerating investment in bio-based production technologies, low-VOC chemical solutions, and integrated green chemistry platforms.

Producers are increasingly focusing on process optimization, renewable feedstock integration, and emissions reduction technologies to align with tightening regulatory frameworks.

Vertical integration across feedstock sourcing, chemical processing, and downstream applications is becoming a key strategy to stabilize margins and reduce exposure to raw material volatility.

Companies capable of scaling bio-based production efficiently while maintaining cost competitiveness are expected to gain long-term market advantage.

Global Isobutanol Market Risk & Disruption Forward Outlook

Looking ahead to 2026???2033, the isobutanol market is expected to evolve toward a more sustainable, regulated, and technology-driven structure.

- Expansion of Bio-Based Isobutanol: Renewable production will gain increasing market share.

- Stronger Environmental Regulations: VOC and emission controls will intensify globally.

- Green Chemistry Adoption: Low-toxicity and sustainable solvents will drive substitution trends.

- Fuel Additive Growth: Demand from cleaner fuel formulations will support expansion.

- Process Innovation Acceleration: Advanced fermentation and catalytic technologies will improve efficiency.

- Industrial Demand Recovery Cycles: Coatings and construction sectors will remain key demand drivers.

- Capacity Expansion in Asia-Pacific: Regional production scaling will reshape global supply dynamics.

Overall, the Global Isobutanol Market remains a moderately cyclical but strategically important chemical segment where long-term success will depend on feedstock efficiency, regulatory adaptability, bio-based innovation, and cost-competitive sustainable production.

Regulatory Landscape

Global Isobutanol Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global isobutanol market is primarily shaped by volatile organic compound (VOC) emission regulations, environmental compliance mandates, industrial chemical safety standards, and evolving sustainability frameworks promoting bio-based chemical adoption. As isobutanol is widely used in solvents, coatings, fuel additives, and chemical intermediates, regulatory oversight increasingly focuses on reducing environmental impact while ensuring safe handling, storage, and transportation of flammable chemical substances.

Manufacturers and downstream users must comply with stringent chemical classification and labeling systems, hazardous substance transportation rules, workplace exposure limits, and environmental discharge norms. These requirements directly influence production processes, formulation strategies, and end-use applications across industrial and consumer sectors.

The accelerating transition toward bio-based isobutanol and low-VOC chemical solutions is further reshaping regulatory frameworks, encouraging innovation in green chemistry, renewable feedstock utilization, and cleaner industrial production technologies.

Global Isobutanol Market Regulatory & Policy Environment Current Scenario

The current regulatory framework for the isobutanol market is built around environmental protection laws, chemical safety regulations, and industrial emission control standards that govern both production and end-use applications.

In North America and Europe, strict VOC emission limits under environmental protection agencies and chemical regulatory systems such as REACH and TSCA are driving manufacturers to reformulate products using lower-emission and bio-based alternatives. These regulations are particularly impactful in coatings, paints, and solvent-based applications where isobutanol is extensively used.

Occupational health and safety regulations require controlled handling of flammable and toxic chemicals, with mandatory exposure limits, ventilation systems, and safety monitoring protocols in industrial facilities.

In Asia-Pacific, regulatory frameworks are rapidly evolving as industrial chemical production expands. Governments are tightening environmental compliance standards while simultaneously encouraging industrial growth through modernization of chemical manufacturing infrastructure and adoption of cleaner production technologies.

Additionally, fuel additive applications of isobutanol are subject to energy and transportation fuel standards that regulate blending ratios, combustion performance, and emissions characteristics across different markets.

Key Regulatory & Policy Environment Signals in Global Isobutanol Market

- VOC Emission Regulations: Strict limits on solvent emissions are driving adoption of low-VOC and bio-based formulations.

- Chemical Safety Compliance: Handling, storage, and transport of isobutanol are governed by hazardous chemical safety frameworks.

- Environmental Protection Standards: Regulations focus on reducing industrial pollution and promoting cleaner production methods.

- Bio-Based Chemical Incentives: Policy support is increasing for renewable feedstock and sustainable chemical alternatives.

- Industrial Workplace Safety Rules: Exposure limits and safety protocols are required in manufacturing and processing facilities.

- Fuel Additive Regulations: Energy and transportation standards influence blending and usage in fuel applications.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is accelerating investments in bio-based isobutanol production, low-emission manufacturing technologies, and green chemistry innovation. Chemical producers are increasingly optimizing production processes to reduce VOC intensity while improving cost efficiency and product performance.

Environmental compliance pressures are encouraging the development of advanced catalytic processes, bio-fermentation technologies, and renewable feedstock integration to reduce reliance on petrochemical-based production routes.

Industrial safety regulations are driving adoption of automated monitoring systems, advanced containment infrastructure, and improved chemical handling protocols to minimize operational risks in production facilities.

At the same time, sustainability-focused policies are reshaping competitive dynamics by favoring manufacturers that can supply low-toxicity, environmentally compliant, and renewable chemical solutions to downstream industries.

Overall, regulatory alignment between environmental standards and industrial chemical innovation is creating a structural shift toward cleaner, safer, and more sustainable isobutanol production ecosystems.

Global Isobutanol Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global isobutanol market is expected to become more stringent and sustainability-driven, with increased emphasis on decarbonization, chemical safety transparency, and lifecycle emissions reduction across industrial value chains.

Governments are likely to strengthen VOC reduction targets, expand restrictions on petrochemical-based solvents, and provide greater policy incentives for bio-based and renewable chemical production technologies.

Fuel blending regulations may also evolve to support cleaner combustion standards, indirectly increasing demand for high-performance, low-emission oxygenates such as isobutanol in energy applications.

Digital chemical compliance systems, traceability frameworks, and automated environmental reporting mechanisms are expected to become more widely adopted across global chemical manufacturing networks.

Overall, regulatory and policy developments will remain a key structural driver of market transformation, with companies investing in sustainable production, bio-based innovation, and advanced compliance systems expected to maintain long-term competitive advantage.