Global Cigarette Filters Market Report, Size, Share and Forecast 2026–2033

Global Cigarette Filters Market Forecast Snapshot (2026???2033)

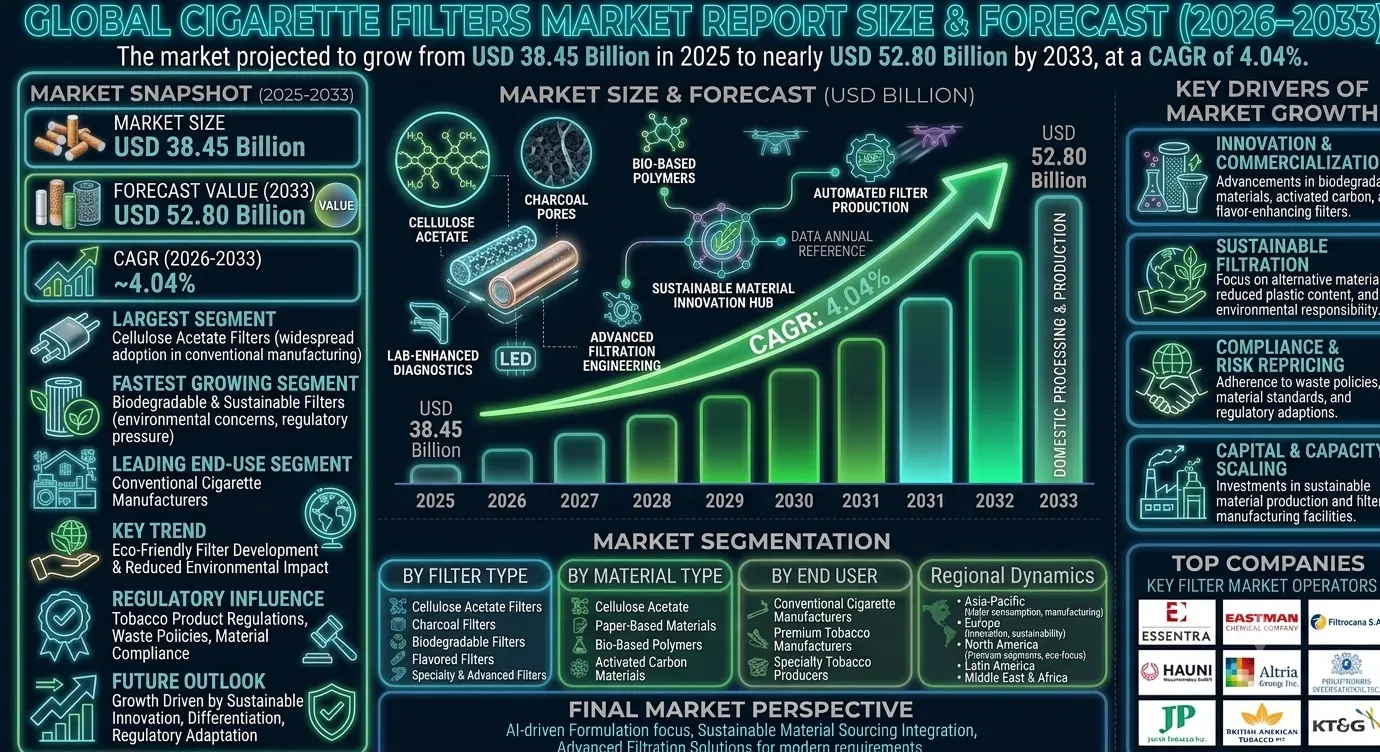

| Metric | Value |

|---|---|

| Market Size (2025) | USD 38.45 Billion |

| Market Size (2033) | USD 52.80 Billion |

| CAGR (2026???2033) | 4.04% |

| Largest Segment | Cellulose Acetate Filters |

| Fastest Growing Segment | Biodegradable & Sustainable Filters |

| Leading End-Use Segment | Conventional Cigarette Manufacturers |

| Key Trend | Eco-Friendly Filter Development & Reduced Environmental Impact Solutions |

| Regulatory Influence | Tobacco Product Regulations, Environmental Waste Policies & Filter Material Compliance Standards |

| Future Outlook | Growth Driven by Sustainable Filter Innovation, Product Differentiation & Regulatory Adaptation |

Global Cigarette Filters Market Size & Forecast

The Global Cigarette Filters Market is expected to witness moderate growth during the forecast period from 2026 to 2033. The market was valued at USD 38.45 billion in 2025 and is projected to reach approximately USD 52.80 billion by 2033, registering a CAGR of 4.04%. The market growth is primarily driven by sustained global cigarette production, increasing demand for filtered tobacco products, ongoing product innovation, and the development of environmentally sustainable filter materials. Cigarette filters remain a critical component of modern cigarette manufacturing, helping regulate smoke flow, filtration efficiency, and consumer smoking experience. In addition, growing industry focus on biodegradable materials and environmental compliance is supporting market transformation and long-term innovation.

Global Cigarette Filters Market Overview

Cigarette filters are specialized components attached to cigarettes to reduce the inhalation of particulate matter and modify smoking characteristics. The market includes cellulose acetate filters, charcoal filters, biodegradable filters, flavoured filters, recessed filters, and specialty filtration technologies. Cigarette filters are primarily utilized by tobacco manufacturers for conventional cigarettes, premium cigarettes, and specialty tobacco products. The industry is increasingly shifting toward sustainable materials, enhanced filtration technologies, and environmentally responsible product development.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Advancements in biodegradable materials, activated carbon filtration technologies, flavor-enhancing filters, and next-generation filter designs are supporting market innovation. Manufacturers are investing in sustainable alternatives to conventional cellulose acetate filters to address environmental concerns.Market Implications

Companies investing in eco-friendly filter technologies and product differentiation are expected to strengthen market competitiveness.2. Compliance and Risk Repricing

Tobacco regulations, environmental waste management policies, product labeling requirements, and material compliance standards are influencing market dynamics. Governments and environmental agencies are increasingly scrutinizing cigarette filter waste and its environmental impact.Market Implications

Firms developing sustainable and compliant filter solutions are likely to gain stronger market acceptance.3. Competitive and Value-Chain Reconfiguration

The market remains competitive with filter manufacturers, material suppliers, tobacco companies, and specialty filtration technology providers participating across the value chain. Strategic partnerships between tobacco producers and sustainable material innovators are reshaping industry development.Market Implications

Organizations focusing on advanced filtration performance and environmental sustainability may achieve stronger long-term positioning.4. Capital and Capacity Scaling

Investments in sustainable material production, filter manufacturing technologies, and product innovation facilities are supporting market growth. Modernization of cigarette manufacturing operations continues to drive demand for advanced filter solutions.Market Implications

Manufacturers expanding sustainable production capabilities are expected to capture future opportunities.Market Segmentation Analysis

By Filter Type

1. Cellulose Acetate Filters

This remains the largest segment due to widespread adoption across conventional cigarette manufacturing.2. Charcoal Filters

Growing demand driven by enhanced filtration performance and consumer preference in selected markets.3. Biodegradable Filters

Fastest-growing segment due to increasing environmental concerns and regulatory pressure.4. Flavored Filters

Utilized in specialty tobacco products where permitted by regulations.5. Specialty & Advanced Filters

Increasing adoption for premium product differentiation and customized smoking experiences.By Material Type

1. Cellulose Acetate

Largest segment owing to established manufacturing infrastructure and cost efficiency.2. Paper-Based Materials

Growing demand for sustainable and biodegradable alternatives.3. Bio-Based Polymers

Fast-growing category supported by environmental sustainability initiatives.4. Activated Carbon Materials

Widely utilized for enhanced smoke filtration applications.By End User

1. Conventional Cigarette Manufacturers

Largest segment due to significant global cigarette production volumes.2. Premium Tobacco Product Manufacturers

Strong demand for differentiated and specialty filter technologies.3. Specialty Tobacco Producers

Growing adoption of customized filtration solutions and innovative filter designs.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global cigarette filters market due to large-scale tobacco production, significant consumer base, and extensive cigarette manufacturing activities in countries such as China, Indonesia, and Japan.Europe

Europe remains a major market supported by product innovation, sustainability initiatives, and regulatory-driven filter development.North America

North America is witnessing steady demand driven by premium product segments and increasing focus on environmentally sustainable filter solutions.Latin America

Latin America continues to show moderate growth due to established tobacco industries and evolving product portfolios.Middle East & Africa

The region is experiencing gradual market expansion supported by tobacco consumption and manufacturing activities.Competitive Landscape

The Global Cigarette Filters Market is moderately consolidated with specialized filter manufacturers and tobacco industry suppliers competing across global markets.Key Companies Operating in the Market Include:

- Essentra plc

- Eastman Chemical Company

- Filtrocana S.A.

- Targard Filter Systems Inc.

- Hauni Maschinenbau GmbH

- Altria Group, Inc.

- Philip Morris International Inc.

- Japan Tobacco Inc.

- British American Tobacco plc

- KT&G Corporation

Strategic Outlook

The future of the cigarette filters market will be shaped by biodegradable filter technologies, sustainable materials innovation, enhanced filtration performance, and environmental compliance initiatives. Research into alternative materials, reduced plastic content, and advanced filter engineering will significantly influence product development strategies. The increasing emphasis on environmental responsibility and sustainable manufacturing practices is expected to create long-term innovation opportunities across the industry.Final Market Perspective

The Global Cigarette Filters Market remains an important component of the tobacco products value chain. Product innovation, sustainability initiatives, and evolving regulatory requirements continue shaping market development. Companies capable of delivering compliant, environmentally responsible, and technologically advanced filter solutions will be best positioned to capture future opportunities. The convergence of sustainability, material innovation, and filtration performance is expected to redefine the future of the global cigarette filters industry.Table of Contents

Table of Contents

- Executive Summary

- Global Cigarette Filters Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends & Sustainability Transformation

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Cigarette Filters

- Scope of the Global Cigarette Filters Market

- Evolution of Cigarette Filtration Technologies

- Role of Filters in Tobacco Product Manufacturing

- Value Chain Analysis of Cigarette Filter Production

- Regulatory Influence (Tobacco Product Regulations, Environmental Waste Policies & Filter Material Compliance Standards)

- Transition Toward Sustainable & Environmentally Responsible Filter Solutions

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Innovation and Commercialization Acceleration in Filter Technologies

- Compliance and Risk Repricing in Tobacco & Environmental Regulations

- Competitive and Value-Chain Reconfiguration

- Capital and Capacity Scaling in Filter Manufacturing

- Market Restraints

- Increasing Regulatory Pressure on Tobacco Products

- Environmental Concerns Related to Filter Waste

- Declining Smoking Rates in Certain Developed Markets

- Market Opportunities

- Expansion of Biodegradable & Sustainable Filter Solutions

- Growth in Advanced Filtration Technologies

- Development of Premium & Specialty Filter Products

- Strategic Partnerships for Sustainable Material Innovation

- Market Challenges

- Balancing Filtration Performance with Sustainability Goals

- Compliance with Evolving Global Regulations

- Raw Material Supply & Cost Volatility

- Structural Drivers of Market Growth

- Global Cigarette Filters Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Demand-Supply Trends

- Pricing Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Filter Type

- Cellulose Acetate Filters (Largest Segment)

- Charcoal Filters

- Biodegradable Filters (Fastest-Growing Segment)

- Flavored Filters

- Specialty & Advanced Filters

- By Material Type

- Cellulose Acetate (Largest Segment)

- Paper-Based Materials

- Bio-Based Polymers (Fastest-Growing Segment)

- Activated Carbon Materials

- By End User

- Conventional Cigarette Manufacturers (Largest Segment)

- Premium Tobacco Product Manufacturers

- Specialty Tobacco Producers

- By Filter Type

- Regional Market Analysis

- Asia-Pacific (Largest Market)

- Europe

- North America

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Consolidation Analysis

- Key Player Benchmarking

- Strategic Developments

- Sustainable Filter Innovation Strategies

- Partnerships, Expansion & Supply Chain Trends

- Company Profiles

- Essentra plc

- Eastman Chemical Company

- Filtrocana S.A.

- Targard Filter Systems Inc.

- Hauni Maschinenbau GmbH

- Altria Group, Inc.

- Philip Morris International Inc.

- Japan Tobacco Inc.

- British American Tobacco plc

- KT&G Corporation

- Strategic Outlook

- Future of Biodegradable Filter Technologies

- Sustainable Material Innovation & Product Differentiation

- Expansion of Environmentally Responsible Manufacturing Practices

- Advanced Filtration Performance Enhancement Strategies

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Cigarette Filters Market Competitive Intensity & Market Structure Overview

The Global Cigarette Filters Market is moderately consolidated, with competition concentrated among specialized filter manufacturers, filtration technology providers, raw material suppliers, and vertically integrated tobacco companies. Competitive intensity is primarily driven by filtration performance, product innovation, manufacturing efficiency, sustainability initiatives, regulatory compliance, and long-term supply agreements with cigarette manufacturers.

Companies compete by offering a wide range of filter solutions, including cellulose acetate filters, charcoal filters, biodegradable filters, flavored filters, and advanced filtration technologies. Increasing environmental concerns and growing regulatory scrutiny regarding cigarette filter waste are accelerating competition in sustainable filter development.

The market structure is gradually evolving from conventional cellulose acetate-based products toward eco-friendly, biodegradable, and bio-based filtration solutions. Strategic collaborations between filter manufacturers, material innovators, and tobacco companies are reshaping industry dynamics and accelerating technological advancement.

Global Cigarette Filters Market Competitive Intensity & Market Structure Current Scenario

Leading Global Cigarette Filters Companies

Essentra plc: One of the world’s leading cigarette filter manufacturers, offering a broad portfolio of conventional, specialty, and sustainable filter solutions for global tobacco companies.

Eastman Chemical Company: A major supplier of cellulose acetate tow and advanced material solutions widely utilized in cigarette filter production worldwide.

Filtrocana S.A.: A specialized cigarette filter manufacturer known for customized filtration solutions and long-standing relationships with tobacco producers.

Targard Filter Systems Inc.: A filtration technology company focused on innovative cigarette filter systems and advanced smoke filtration performance.

Hauni Maschinenbau GmbH: A leading provider of cigarette manufacturing and filter production technologies supporting global tobacco industry operations.

Altria Group, Inc.: A major tobacco company investing in product innovation, filtration technologies, and regulatory-compliant cigarette products.

Philip Morris International Inc.: One of the largest global tobacco manufacturers utilizing advanced filter technologies and sustainability-focused product development initiatives.

Japan Tobacco Inc.: A leading international tobacco company engaged in cigarette innovation, product differentiation, and advanced filtration solutions.

British American Tobacco plc: A global tobacco leader investing in sustainable materials, product innovation, and next-generation tobacco product technologies.

KT&G Corporation: A prominent tobacco manufacturer focused on product quality enhancement, specialty filters, and international market expansion.

Key Competitive Intensity & Market Structure Drivers

Growing regulatory focus on cigarette waste management and environmental sustainability is intensifying competition among manufacturers developing biodegradable and eco-friendly filter alternatives.

Advancements in filtration efficiency, activated carbon technologies, and specialty filter designs are creating opportunities for product differentiation and premium market positioning.

Long-term supply agreements with major tobacco manufacturers remain a critical competitive factor influencing market share and revenue stability.

Increasing investments in sustainable materials, bio-based polymers, and reduced-plastic filter technologies are reshaping industry innovation strategies.

The need to comply with evolving tobacco product regulations, environmental policies, and material safety standards is encouraging continuous research and development across the value chain.

Strategic Implications of Competitive Intensity & Market Structure

Companies with strong manufacturing capabilities, advanced filtration technologies, and established relationships with global tobacco producers are expected to maintain significant competitive advantages.

Investment in biodegradable filter materials, sustainable production processes, and environmentally responsible product development is becoming a critical factor for long-term market differentiation.

Manufacturers focusing on innovation, regulatory compliance, and enhanced filtration performance are likely to strengthen their market position amid increasing environmental scrutiny.

Strategic partnerships between material suppliers, filter manufacturers, and tobacco companies are enabling faster commercialization of next-generation filter technologies.

Organizations capable of balancing performance, sustainability, cost efficiency, and regulatory requirements will be better positioned to compete effectively in evolving global markets.

Global Cigarette Filters Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global cigarette filters market is expected to become increasingly innovation-driven as environmental regulations, sustainability initiatives, and material science advancements gain momentum worldwide.

Future competition will be shaped by biodegradable filtration technologies, bio-based materials, advanced smoke filtration systems, and reduced environmental impact solutions.

Manufacturers are expected to increase investments in research and development, sustainable raw materials, and next-generation filtration technologies to strengthen competitive positioning.

Over the forecast period, companies that successfully balance innovation, sustainability, manufacturing efficiency, regulatory compliance, and global customer relationships will be best positioned to lead the evolving global cigarette filters market.

Value Chain

Global Cigarette Filters Market Value Chain & Supply Chain Evolution Overview

The Global Cigarette Filters Market operates through a highly specialized value chain that encompasses raw material sourcing, filter material production, filtration technology development, filter manufacturing, cigarette assembly, distribution, and end-user consumption. The market is evolving as manufacturers balance filtration performance, production efficiency, regulatory compliance, and environmental sustainability requirements.

A defining characteristic of the value chain is the growing transition from traditional cellulose acetate-based filters toward biodegradable, paper-based, and bio-derived filtration materials. Environmental concerns associated with cigarette filter waste are prompting manufacturers, regulators, and tobacco companies to invest in sustainable alternatives and circular economy initiatives.

Supply chain operations involve coordination among chemical suppliers, cellulose producers, specialty material manufacturers, filter technology developers, cigarette manufacturers, and distribution partners. The increasing complexity of environmental regulations and sustainability expectations is accelerating innovation across the entire supply chain ecosystem.

As the market evolves, companies are investing in advanced filtration technologies, sustainable material sourcing, production automation, and environmentally responsible manufacturing processes to strengthen competitiveness and maintain regulatory compliance.

Global Cigarette Filters Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Material Sourcing: Procurement of cellulose acetate, paper fibers, activated carbon, bio-based polymers, flavor additives, and specialty filtration materials.

- Material Processing & Component Manufacturing: Production of filter tow, activated carbon components, biodegradable materials, specialty filter inserts, and filtration media.

- Filter Design & Technology Development: Research and development focused on filtration efficiency, smoke flow optimization, flavor enhancement, and environmentally sustainable filter solutions.

- Filter Manufacturing & Assembly: Production of cellulose acetate filters, charcoal filters, biodegradable filters, flavored filters, and specialty cigarette filtration systems.

- Cigarette Production Integration: Incorporation of filters into conventional, premium, and specialty tobacco products through automated cigarette manufacturing operations.

- Distribution & Commercialization: Supply of finished filtered cigarette products through wholesalers, distributors, retailers, and international tobacco supply networks.

- End User Consumption: Consumption of filtered tobacco products across global consumer markets and tobacco product categories.

Company-to-Stage Mapping

- Raw Material Sourcing: Eastman Chemical Company, cellulose producers, activated carbon suppliers, paper manufacturers, and bio-based material providers.

- Material Processing & Component Manufacturing: Specialized filter tow manufacturers, activated carbon processors, and sustainable material suppliers.

- Filter Design & Technology Development: Essentra plc, Targard Filter Systems Inc., Filtrocana S.A., and specialty filtration technology developers.

- Filter Manufacturing & Assembly: Essentra plc, Hauni Maschinenbau GmbH, and global cigarette filter manufacturing organizations.

- Cigarette Production Integration: Philip Morris International Inc., British American Tobacco plc, Japan Tobacco Inc., KT&G Corporation, and Altria Group, Inc.

- Distribution & Commercialization: Tobacco distributors, wholesalers, retail networks, and international supply chain operators.

- End User Consumption: Adult tobacco consumers across conventional, premium, and specialty cigarette segments.

Key Value Chain & Supply Chain Evolution Signals in Global Cigarette Filters Market

Growing Adoption of Biodegradable Filters

Environmental concerns surrounding cigarette butt waste are accelerating development and commercialization of biodegradable filter technologies and sustainable material alternatives.

Expansion of Sustainable Material Innovation

Manufacturers are investing in paper-based materials, bio-derived polymers, and alternative filtration media to reduce environmental impact while maintaining product performance.

Advancements in Filtration Technology

Research into enhanced filtration efficiency, activated carbon technologies, and customized filter designs is supporting product differentiation across tobacco categories.

Increasing Regulatory Scrutiny

Environmental regulations, tobacco product standards, and waste management policies are influencing material selection, manufacturing processes, and product development strategies.

Strategic Collaboration Across the Value Chain

Partnerships between tobacco companies, material innovators, and filtration technology providers are supporting commercialization of next-generation filter solutions.

Manufacturing Modernization and Automation

Advanced production technologies and automated filter manufacturing systems are improving production efficiency, consistency, and scalability.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Sustainable Filter Technologies

Companies developing biodegradable and environmentally responsible filtration solutions can strengthen regulatory compliance and future market positioning.

Diversification of Material Supply Sources

Expanding supplier networks and adopting alternative raw materials can improve supply chain resilience and reduce dependency on conventional materials.

Strengthening Research and Development Capabilities

Continuous innovation in filter design, material science, and filtration performance can support product differentiation and long-term competitiveness.

Alignment with Environmental Regulations

Organizations proactively adapting to waste reduction policies and sustainability requirements are likely to gain stronger acceptance from regulators and stakeholders.

Expansion of Premium and Specialty Filter Solutions

Advanced filter technologies and customized smoking experiences can create opportunities in premium tobacco product categories.

Optimization of Manufacturing Efficiency

Investments in automated production systems and process optimization can enhance operational performance and cost competitiveness.

Global Cigarette Filters Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the value chain is expected to evolve toward a more sustainable, technology-driven, and compliance-focused ecosystem as environmental responsibility becomes a central industry priority.

Key Future Developments Include:

- Expansion of biodegradable and compostable cigarette filter technologies.

- Increased adoption of bio-based materials and sustainable filtration media.

- Growth in advanced activated carbon and specialty filtration systems.

- Strengthening of environmental compliance and waste reduction initiatives.

- Expansion of strategic partnerships between tobacco companies and material innovators.

- Greater investment in automated manufacturing and production efficiency technologies.

As the market evolves, competitive advantage will increasingly depend on the ability to combine filtration performance, sustainability innovation, regulatory compliance, and efficient supply chain management within an integrated manufacturing ecosystem.

Companies that successfully integrate advanced filter technologies, environmentally responsible materials, scalable production capabilities, and resilient supply chain strategies will achieve stronger market positioning and long-term growth in the Global Cigarette Filters Market.

Investment Activity

Global Cigarette Filters Market Investment & Funding Dynamics Overview

The Global Cigarette Filters Market is witnessing evolving investment activity driven by ongoing cigarette production, increasing focus on sustainable filter technologies, regulatory pressure regarding cigarette waste, and growing demand for environmentally responsible tobacco product components. Filter manufacturers, tobacco companies, material science firms, institutional investors, and sustainability-focused innovation partners are directing capital toward biodegradable filter materials, advanced filtration technologies, sustainable manufacturing processes, and next-generation cigarette filter solutions.

Investment momentum is increasingly shifting from conventional filter production toward environmentally friendly alternatives as governments and environmental organizations intensify scrutiny of cigarette butt pollution. Capital allocation is expanding across bio-based polymers, paper-based filters, activated carbon technologies, recyclable materials, and eco-friendly product development initiatives.

Additionally, growing investments in research and development, sustainable raw material sourcing, manufacturing modernization, and filtration performance enhancement technologies are creating new opportunities across the global cigarette filters value chain.

Global Cigarette Filters Market Investment & Funding Dynamics Current Scenario

Currently, the market is experiencing targeted investment activity as manufacturers adapt to changing regulatory requirements and increasing environmental expectations. Industry participants are investing in sustainable filter production facilities, biodegradable material technologies, advanced manufacturing systems, and product innovation programs.

The market is benefiting from strategic collaborations between tobacco companies, material developers, and filtration technology providers focused on reducing environmental impact while maintaining product performance. Significant capital is being directed toward alternative filter materials, compliance-driven product development, and manufacturing efficiency improvements.

Furthermore, partnerships between filter manufacturers, research institutions, raw material suppliers, and tobacco companies are accelerating commercialization efforts and supporting the transition toward more sustainable filtration solutions.

Key Investment & Funding Dynamics Signals in Global Cigarette Filters Market

- Growing demand for biodegradable and sustainable cigarette filters is driving investments in alternative material technologies.

- Increasing environmental concerns regarding cigarette butt waste and plastic pollution are influencing capital allocation decisions.

- Expansion of advanced filtration and activated carbon technologies is supporting product innovation funding.

- Regulatory pressure surrounding environmental compliance and waste management is accelerating investment in sustainable solutions.

- Strategic investments in bio-based polymers and paper-based filter materials are creating long-term growth opportunities.

- Modernization of filter manufacturing facilities and automation systems is improving production efficiency and competitiveness.

- Collaborative research programs focused on next-generation filtration performance and sustainability objectives are strengthening innovation pipelines.

Strategic Implications of Investment & Funding Dynamics in Global Cigarette Filters Market

- Continuous investment in sustainable filter technologies and material innovation will be essential for long-term market relevance.

- Capital allocation toward biodegradable materials, production modernization, and environmental compliance initiatives will strengthen competitive positioning.

- Companies developing eco-friendly and performance-enhancing filter solutions are expected to secure stronger future growth opportunities.

- Strategic partnerships with material science companies and research institutions will accelerate commercialization of innovative filter technologies.

- Investments in automation, manufacturing efficiency, and sustainable sourcing programs will support operational optimization.

- Compliance with tobacco product regulations, environmental waste policies, and material compliance standards will continue shaping investment strategies.

- Organizations building integrated capabilities across material development, filter manufacturing, and sustainability management are expected to capture greater long-term value.

Global Cigarette Filters Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Cigarette Filters Market is expected to maintain steady investment activity as manufacturers prioritize environmental responsibility, product differentiation, and regulatory adaptation. Sustainable filter innovation is anticipated to remain the primary focus of future capital deployment.

Future investments are likely to concentrate on biodegradable filter technologies, advanced filtration materials, reduced-plastic solutions, sustainable manufacturing systems, and environmentally compliant product portfolios.

As regulatory expectations and environmental awareness continue to increase globally, investment activity is expected to expand across material innovation, circular economy initiatives, manufacturing modernization, and sustainability-focused research and development programs.

In conclusion, the Global Cigarette Filters Market represents a strategically evolving investment landscape where sustainable materials, advanced filtration technologies, environmental compliance, manufacturing innovation, and product differentiation will define future funding priorities, competitive dynamics, and long-term industry growth.

Technology & Innovation

Global Cigarette Filters Market Technology & Innovation Landscape Overview

The Global Cigarette Filters Market is experiencing a gradual but significant technological transformation driven by advancements in sustainable materials, filtration efficiency engineering, biodegradable filter technologies, activated carbon integration, and environmentally responsible manufacturing processes. Innovation within the market is increasingly focused on balancing filtration performance, regulatory compliance, consumer preferences, and environmental sustainability.

At the center of this evolution is the transition from conventional cellulose acetate-based filters toward eco-friendly alternatives designed to reduce environmental waste while maintaining product functionality and manufacturing compatibility.

A major area of innovation involves the development of biodegradable and compostable filter materials, including paper-based fibers, bio-based polymers, and plant-derived filtration components that address growing concerns regarding cigarette butt pollution.

The market is also witnessing advancements in filtration science, including activated carbon technologies, multi-segment filter designs, recessed filter structures, and specialty filtration systems that enhance smoke filtration performance and product differentiation.

Manufacturers are increasingly investing in sustainable production technologies, material optimization processes, and waste-reduction initiatives to improve environmental performance throughout the filter manufacturing value chain.

Product innovation further includes flavor-enhancing filters, premium customized filter designs, and advanced structural engineering solutions that improve smoking characteristics while meeting evolving market demands.

Additionally, digital manufacturing technologies, automated quality control systems, and precision material processing are improving production efficiency and product consistency.

The convergence of sustainable materials, advanced filtration technologies, precision manufacturing, and environmental compliance is redefining the future technology landscape of the global cigarette filters market.

Global Cigarette Filters Market Technology & Innovation Landscape Current Scenario

Currently, the Global Cigarette Filters Market demonstrates increasing innovation activity focused on biodegradable materials, filtration enhancement, and environmentally sustainable product development.

1. Biodegradable Filter Technologies

Manufacturers are developing filter materials that decompose more rapidly than conventional cellulose acetate filters, helping reduce environmental waste.

2. Activated Carbon Filtration Systems

Activated carbon technologies are being integrated into filters to enhance smoke filtration performance and support premium product positioning.

3. Advanced Multi-Segment Filter Designs

Multi-component filters are improving filtration efficiency while enabling product differentiation across tobacco brands.

4. Sustainable Material Innovation

Research into plant-based fibers, paper materials, and bio-derived polymers is accelerating the commercialization of environmentally friendly filter alternatives.

5. Precision Manufacturing & Automation

Modern production systems are improving filter consistency, production speed, and material utilization efficiency.

6. Specialty & Customized Filters

Manufacturers are introducing innovative filter formats designed to enhance smoking characteristics and support premium tobacco products.

Key Technology & Innovation Landscape Signals in Global Cigarette Filters Market

Several innovation trends are shaping the future development of the market:

1. Growing Focus on Environmental Sustainability

Increasing awareness of cigarette butt pollution is accelerating investment in biodegradable and eco-friendly filter solutions.

2. Expansion of Bio-Based Material Research

Manufacturers are exploring renewable raw materials to reduce dependence on traditional synthetic filter components.

3. Increasing Regulatory Scrutiny

Environmental regulations and waste management policies are encouraging continuous product innovation.

4. Demand for Enhanced Filtration Performance

Advanced filter technologies are being developed to improve filtration efficiency and support product differentiation.

5. Modernization of Manufacturing Facilities

Automation and digital production technologies are improving operational efficiency and quality control.

6. Strategic Collaboration Across the Value Chain

Partnerships between tobacco companies, material suppliers, and technology developers are accelerating innovation efforts.

7. Development of Circular Economy Solutions

Manufacturers are evaluating recyclable materials and sustainable production models to reduce environmental impact.

Strategic Implications of Technology & Innovation Landscape in Global Cigarette Filters Market

The evolving innovation landscape is reshaping competition throughout the cigarette filters industry. Companies are increasingly competing through sustainable material innovation, filtration effectiveness, regulatory compliance, and manufacturing efficiency.

Manufacturers investing in biodegradable filter technologies, advanced material science, automated production systems, and environmentally responsible solutions are expected to strengthen long-term market positioning.

Strategic partnerships among tobacco producers, specialty material companies, filtration technology developers, and sustainability-focused organizations are supporting faster commercialization of next-generation filter products.

The growing convergence of environmental responsibility, filtration performance, and product differentiation is creating significant opportunities for technological leadership.

Additionally, increasing regulatory pressure related to environmental waste management and product sustainability is encouraging continuous investment in research, development, and manufacturing modernization.

Global Cigarette Filters Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026???2033, the Global Cigarette Filters Market is expected to undergo accelerated innovation centered on sustainable materials, advanced filtration technologies, and environmentally responsible manufacturing systems.

Future technological developments are likely to include:

1. Fully Biodegradable Filter Platforms

Next-generation filter solutions will utilize renewable and compostable materials capable of significantly reducing environmental waste.

2. Advanced Bio-Based Material Engineering

Innovative plant-derived materials will improve filter functionality while supporting sustainability objectives.

3. High-Performance Multi-Layer Filtration Systems

Enhanced filter architectures will provide improved filtration efficiency and customized smoking experiences.

4. Smart Manufacturing Technologies

Digital production systems and AI-driven quality control will optimize manufacturing efficiency and product consistency.

5. Circular Economy Production Models

Sustainable resource utilization and waste-reduction strategies will become increasingly important across filter manufacturing operations.

6. Low-Impact Environmental Filter Solutions

Future products will be specifically designed to minimize ecological impact throughout their lifecycle.

7. Sustainable Material Traceability Systems

Digital traceability platforms will improve transparency regarding material sourcing and environmental compliance.

In conclusion, companies capable of combining sustainable material innovation, advanced filtration engineering, precision manufacturing technologies, and regulatory compliance capabilities will be best positioned to lead the future evolution of the Global Cigarette Filters Market.

Market Risk

Global Cigarette Filters Market Risk Factors & Disruption Threats Overview

The Global Cigarette Filters Market operates within a highly regulated tobacco industry where demand is influenced by smoking prevalence, tobacco control policies, environmental regulations, and evolving consumer preferences. While the market benefits from continued cigarette production in several regions and ongoing filter innovation, it faces substantial structural risks associated with declining smoking rates in developed markets, regulatory intervention, environmental scrutiny, and the emergence of alternative nicotine delivery products.

A major structural risk is the increasing intensity of global tobacco control measures. Governments and public health organizations continue to implement stricter regulations on tobacco products, including taxation, packaging restrictions, marketing limitations, and smoking reduction initiatives, which may negatively impact cigarette consumption and filter demand.

Another significant disruption factor is growing environmental concern surrounding cigarette filter waste. Conventional cellulose acetate filters are among the most common forms of litter globally, prompting regulators and environmental groups to advocate for restrictions, waste management obligations, and sustainable material alternatives.

The market also faces disruption from alternative nicotine products such as e-cigarettes, heated tobacco products, nicotine pouches, and other smoke-free alternatives that reduce reliance on traditional combustible cigarettes.

Additionally, raw material price volatility, sustainability compliance requirements, and changing consumer attitudes toward tobacco consumption continue to create uncertainty across the cigarette filter value chain.

Global Cigarette Filters Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by ongoing innovation in filter technology, with manufacturers focusing on biodegradable materials, reduced plastic content, and enhanced filtration performance.

Environmental sustainability has become a central industry priority as governments and regulatory bodies increase scrutiny of cigarette-related waste and single-use plastic components.

While cigarette consumption remains significant across parts of Asia-Pacific, the Middle East, and selected emerging economies, several mature markets continue to experience declining smoking rates due to public health campaigns and regulatory pressures.

Manufacturers are increasingly investing in sustainable filter development to address environmental concerns while maintaining product performance and manufacturing efficiency.

Competition remains active among filter suppliers, tobacco companies, material innovators, and specialty filtration technology providers seeking to adapt to changing regulatory and consumer landscapes.

Key Risk Factors & Disruption Threats Signals in Global Cigarette Filters Market

A major disruption signal is the growing adoption of environmental policies targeting cigarette filter waste, litter reduction, and extended producer responsibility requirements.

Another important signal is the accelerating shift toward biodegradable and bio-based filter materials as manufacturers respond to sustainability expectations and regulatory developments.

The expansion of smoke-free nicotine alternatives continues to alter long-term tobacco consumption patterns and may reduce future demand for traditional cigarette filters.

Increasing research into the environmental impact and public health implications of cigarette filters could influence future policy decisions regarding filter design, composition, and usage.

Consumer demand for premium and differentiated tobacco products is driving innovation in specialty filters, advanced filtration technologies, and customized smoking experiences in selected market segments.

Strategic Implications of Risk Factors & Disruption Threats in Global Cigarette Filters Market

Companies must prioritize sustainable material innovation and environmentally responsible manufacturing practices to address growing regulatory and public concerns regarding cigarette waste.

Investment in biodegradable filters, alternative fiber technologies, and recyclable material solutions will become increasingly important for maintaining long-term market relevance.

Manufacturers should diversify sourcing strategies and strengthen supply chain resilience to mitigate raw material price fluctuations and procurement risks.

Strategic collaboration with tobacco manufacturers, environmental technology providers, and research institutions will support product development and regulatory adaptation efforts.

Organizations capable of balancing filtration performance, sustainability objectives, cost efficiency, and regulatory compliance will be better positioned to compete in an evolving market environment.

Global Cigarette Filters Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Cigarette Filters Market is expected to undergo continued transformation as sustainability requirements, environmental regulations, and tobacco consumption trends reshape industry priorities.

Biodegradable filters, bio-based materials, and reduced-plastic product designs are expected to become increasingly important components of future product development strategies.

Regulatory scrutiny of cigarette waste and environmental impact is likely to intensify, encouraging greater innovation in sustainable filter technologies and waste reduction initiatives.

Alternative nicotine products will continue influencing tobacco market dynamics, requiring traditional filter manufacturers to adapt to changing consumption patterns and industry structures.

Overall, the market is expected to remain stable but increasingly regulated, with long-term success defined by environmental compliance, sustainable innovation, technological advancement, and the ability to respond effectively to evolving tobacco industry requirements.

Regulatory Landscape

Global Cigarette Filters Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Cigarette Filters Market is becoming increasingly complex as public health authorities, environmental agencies, and tobacco regulators intensify oversight of tobacco products and their environmental impact. Cigarette filters are subject to regulations covering tobacco product manufacturing, material composition, consumer safety, product labeling, waste management, and environmental sustainability.

Filter manufacturers, material suppliers, and tobacco companies must comply with a broad range of regulatory requirements related to product standards, ingredient disclosures, environmental protection measures, and tobacco control frameworks. As concerns regarding cigarette butt pollution and plastic waste continue to grow, regulatory attention is increasingly extending beyond product performance to encompass the entire lifecycle of cigarette filters.

The growing emphasis on environmental responsibility, public health protection, and sustainable manufacturing practices is encouraging policymakers worldwide to introduce stricter regulations governing filter materials, waste reduction initiatives, and producer accountability obligations.

Global Cigarette Filters Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by strong oversight of tobacco products, including regulations governing manufacturing practices, product composition, packaging requirements, and marketing restrictions. Cigarette filters must comply with applicable standards established by national tobacco control authorities and public health agencies.

Environmental regulations are becoming increasingly significant due to growing concerns regarding cigarette butt litter and the accumulation of non-biodegradable filter waste in terrestrial and marine ecosystems. Governments and environmental organizations are evaluating measures to reduce the environmental footprint of conventional cellulose acetate filters.

Material compliance standards are also influencing product development, with manufacturers increasingly assessing alternative materials that satisfy performance, safety, and sustainability requirements. Regulatory scrutiny of plastic-containing filter materials is encouraging research into biodegradable and bio-based alternatives.

Product labeling and consumer information requirements continue to evolve in several markets, with regulators focusing on transparency, health communication, and restrictions on potentially misleading product features or claims.

At the same time, extended producer responsibility (EPR) initiatives and waste management policies are gaining momentum, encouraging tobacco companies and filter manufacturers to participate in environmental mitigation programs and responsible waste handling strategies.

Key Regulatory & Policy Environment Signals in Global Cigarette Filters Market

- Tobacco Product Regulations: Comprehensive rules governing tobacco manufacturing, product standards, packaging, labeling, and market authorization requirements.

- Environmental Waste Policies: Regulations addressing cigarette butt pollution, waste reduction targets, litter prevention programs, and environmental protection objectives.

- Filter Material Compliance Standards: Requirements governing the safety, composition, performance, and environmental characteristics of cigarette filter materials.

- Extended Producer Responsibility (EPR) Frameworks: Policies requiring manufacturers and tobacco companies to contribute to waste management and environmental remediation efforts.

- Product Labeling & Consumer Information Requirements: Standards regulating health warnings, product disclosures, and permissible product-related claims.

- Sustainability & Circular Economy Initiatives: Government-led efforts encouraging biodegradable materials, reduced plastic usage, and environmentally responsible product development.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging manufacturers to accelerate investments in sustainable filter technologies, biodegradable materials, and environmentally responsible production processes. Compliance capabilities are increasingly becoming a competitive differentiator across the industry.

Environmental regulations are driving innovation in bio-based polymers, paper-based filtration materials, and biodegradable filter designs that can reduce the ecological impact of discarded cigarette filters. Companies capable of commercializing scalable sustainable alternatives may benefit from favorable market positioning.

Material compliance requirements are influencing research and development priorities, encouraging manufacturers to balance filtration performance, cost efficiency, regulatory compliance, and environmental sustainability objectives.

Extended producer responsibility programs are increasing pressure on industry participants to develop waste collection, recycling, and environmental stewardship initiatives. These requirements may influence operational costs, product design strategies, and long-term sustainability planning.

The growing focus on environmental accountability is also encouraging closer collaboration among tobacco manufacturers, filter suppliers, material science companies, and regulatory bodies to develop compliant and future-ready solutions.

Global Cigarette Filters Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global cigarette filters market is expected to become increasingly stringent as governments continue strengthening tobacco control measures and environmental protection policies. Greater regulatory scrutiny of filter waste and plastic pollution is likely to accelerate the transition toward sustainable filter materials.

Environmental regulations are expected to encourage wider adoption of biodegradable, compostable, and bio-based filter technologies. Several jurisdictions may introduce stricter requirements related to filter disposal, waste reduction, and material sustainability performance.

Extended producer responsibility frameworks are likely to expand, increasing accountability for tobacco companies and filter manufacturers regarding post-consumer waste management and environmental impact mitigation.

Material compliance standards may become more comprehensive, requiring enhanced testing, certification, traceability, and environmental performance verification for next-generation filter materials.

Overall, the future regulatory landscape will be shaped by the convergence of tobacco control policies, environmental sustainability objectives, waste management regulations, and material innovation standards. Companies capable of delivering compliant, environmentally responsible, scalable, and high-performance filter solutions will be best positioned to capitalize on long-term opportunities within the evolving global cigarette filters market.