Global Gifts Retailing Market Size and Share Analysis 2026-2033

Global Gifts Retailing Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

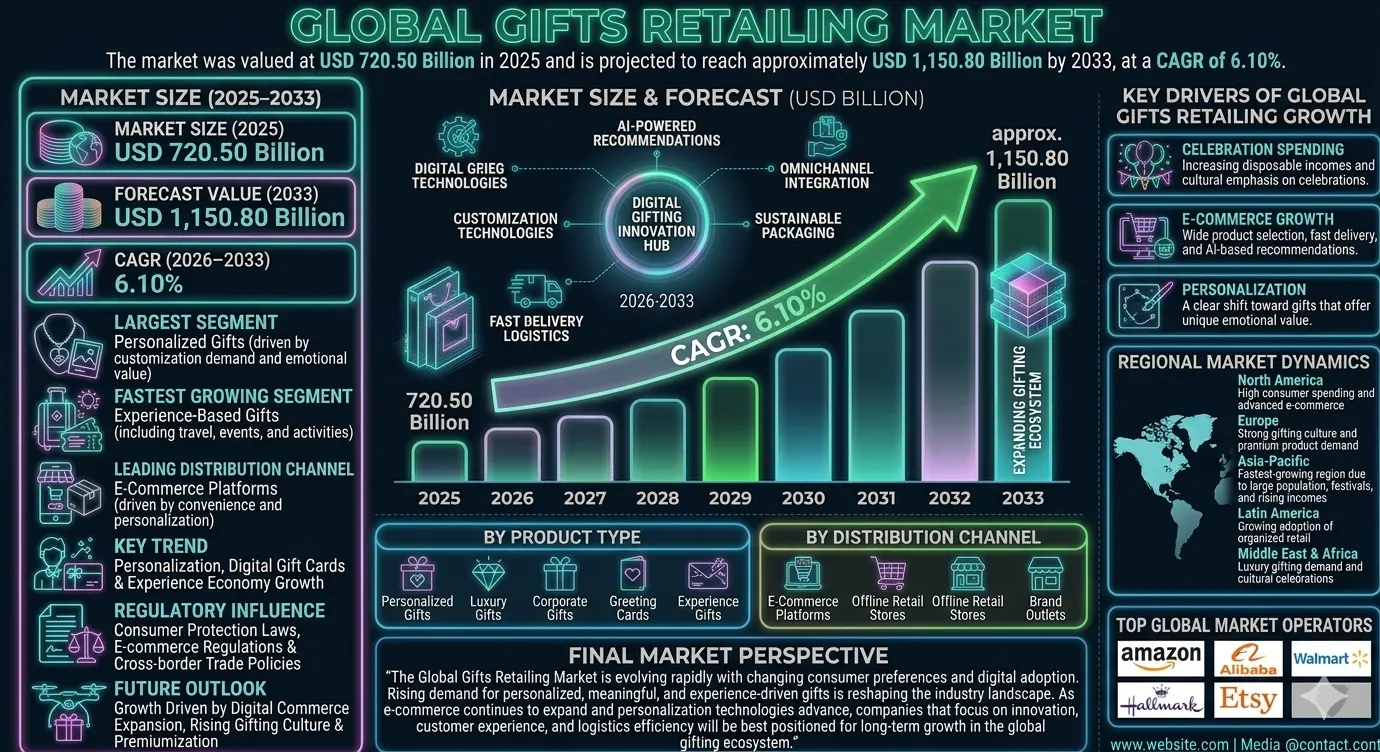

| Market Size (2025) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??USD 720.50 Billion |

| Market Size (2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 1,150.80 Billion |

| CAGR (2026???2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? 6.10% |

| Largest Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Personalized Gifts |

| Fastest Growing Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Experience-Based Gifts |

| Leading Distribution Channel | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??E-Commerce Platforms |

| Key Trend | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? Personalization, Digital Gift Cards & Experience Economy Growth |

| Regulatory Influence | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Consumer Protection Laws, E-commerce Regulations & Cross-border Trade Policies |

| Future Outlook | ?? ?? ?? ?? ?? ??Growth Driven by Digital Commerce Expansion, Rising Gifting Culture & Premiumization of Consumer Goods |

Global Gifts Retailing Market Size & Forecast

The Global Gifts Retailing Market is expected to witness steady expansion during the forecast period from 2026 to 2033. The market was valued at USD 720.50 billion in 2025 and is projected to reach approximately USD 1,150.80 billion by 2033, registering a CAGR of 6.10%. Growth is driven by increasing consumer spending on gifting occasions, rising demand for personalized products, expansion of e-commerce platforms, and growing popularity of experience-based gifting. Seasonal demand and cultural celebrations continue to play a significant role in market expansion globally.Global Gifts Retailing Market Overview

The gifts retailing market includes a wide range of products such as personalized gifts, luxury gifts, corporate gifts, greeting cards, gift hampers, and experience-based gifts. The market is highly seasonal and influenced by festivals, holidays, weddings, corporate events, and personal celebrations. Increasing digitalization and the rise of online gifting platforms have significantly transformed consumer purchasing behavior, enabling convenient and customized gifting solutions.Structural Drivers of Market Growth

1. Rising Consumer Spending on Celebrations

Increasing disposable incomes and growing cultural emphasis on celebrations are driving demand for premium and customized gifts. Market Implications: Retailers are expanding product diversity and premium offerings to capture higher consumer spending.2. Growth of E-Commerce and Online Gifting Platforms

Digital platforms are making gift purchasing more convenient through wide product selection, fast delivery, and personalization options. Market Implications: Online retailers are dominating the market with AI-based recommendation systems and customized gifting solutions.3. Increasing Demand for Personalized Gifts

Consumers are shifting toward customized gifts that offer emotional value and uniqueness. Market Implications: Companies offering personalization technologies are gaining strong competitive advantages.4. Rise of Experience-Based Gifting

Experience gifts such as travel, dining, and adventure packages are gaining popularity over traditional physical gifts. Market Implications: Service-based gifting platforms are emerging as high-growth segments in the retail ecosystem.Market Segmentation Analysis

By Product Type

- Personalized Gifts: Largest segment driven by customization demand and emotional value.

- Luxury Gifts: Premium segment including branded and high-value products.

- Corporate Gifts: Used for employee rewards, client engagement, and branding.

- Greeting Cards & Gift Wraps: Traditional gifting accessories with steady demand.

- Experience-Based Gifts: Fastest growing category including travel, events, and activities.

By Distribution Channel

- E-Commerce Platforms: Largest and fastest-growing channel driven by convenience and personalization.

- Offline Retail Stores: Traditional stores including malls and specialty gift shops.

- Brand Outlets: Premium gifting stores offering curated collections.

By End Use

- Personal Use: Largest segment driven by festivals, birthdays, and celebrations.

- Corporate Sector: Growing demand for employee engagement and business gifting.

- Event Management: Includes weddings, exhibitions, and organized gifting services.

Regional Market Dynamics

North America

Strong market driven by high consumer spending and advanced e-commerce penetration.Europe

Stable growth supported by strong gifting culture and premium product demand.Asia-Pacific

Fastest-growing region due to large population base, festivals, and rising disposable incomes.Latin America

Growing adoption of organized retail and online gifting platforms.Middle East & Africa

Emerging market supported by luxury gifting demand and cultural celebrations.Competitive Landscape

The Global Gifts Retailing Market is highly fragmented with global e-commerce platforms, specialty retailers, and luxury brands competing through personalization, pricing strategies, and delivery innovation. Key Companies Operating in the Market Include:- Amazon.com Inc.

- Alibaba Group

- Walmart Inc.

- Hallmark Cards Inc.

- Etsy Inc.

- Moonpig Group

- Ferns N Petals

- 1-800-Flowers.com

- Shutterfly Inc.

- GiftCards.com

Strategic Outlook

The future of the gifts retailing market will be shaped by digital transformation, AI-driven personalization, and increasing demand for experience-based gifting. E-commerce platforms will continue to dominate through fast delivery, customized recommendations, and global reach. Social media influence and digital marketing will further accelerate gifting trends, especially among younger consumers. Retailers are expected to invest in omnichannel strategies, integrating offline and online experiences to enhance customer engagement. Sustainability and eco-friendly packaging will also gain importance as consumers become more environmentally conscious. The expansion of corporate gifting and subscription-based gifting models will create additional growth opportunities.Final Market Perspective

The Global Gifts Retailing Market is evolving rapidly with changing consumer preferences and digital adoption. Rising demand for personalized, meaningful, and experience-driven gifts is reshaping the industry landscape. As e-commerce continues to expand and personalization technologies advance, companies that focus on innovation, customer experience, and logistics efficiency will be best positioned for long-term growth in the global gifting ecosystem.Table of Contents

Table of Contents

- Executive Summary

- Global Gifts Retailing Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading Distribution Channel Overview

- Key Market Trends in Personalized & Experience-Based Gifting

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Gifts Retailing Market

- Scope of the Global Gifts Retailing Market

- Overview of Gifting Culture and Seasonal Demand Patterns

- Role of Digitalization in Modern Gifting Ecosystem

- Value Chain Analysis of Gifts Retailing Industry

- Regulatory Influence (Consumer Protection Laws, E-commerce Regulations & Cross-border Trade Policies)

- Evolution Toward Personalized, Digital & Experience-Based Gifting

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Rising Consumer Spending on Celebrations

- Growth of E-Commerce and Online Gifting Platforms

- Increasing Demand for Personalized Gifts

- Rise of Experience-Based Gifting

- Market Restraints

- High Competition and Market Fragmentation

- Price Sensitivity in Mass Market Segments

- Logistics and Delivery Challenges During Peak Seasons

- Market Opportunities

- Expansion of Digital Gifting Platforms

- Growth of Subscription-Based Gifting Models

- Rising Demand for Corporate Gifting Solutions

- Integration of AI-Based Personalization Technologies

- Market Challenges

- Seasonality-Driven Revenue Fluctuations

- Sustainability and Packaging Waste Concerns

- Maintaining Customer Experience Across Channels

- Structural Drivers of Market Growth

- Global Gifts Retailing Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Consumer Spending Trends

- E-Commerce Penetration Analysis

- Digital Gifting Adoption Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Product Type

- Personalized Gifts (Largest Segment)

- Luxury Gifts

- Corporate Gifts

- Greeting Cards & Gift Wraps

- Experience-Based Gifts (Fastest-Growing Segment)

- By Distribution Channel

- E-Commerce Platforms (Largest & Fastest-Growing Segment)

- Offline Retail Stores

- Brand Outlets

- By End Use

- Personal Use (Largest Segment)

- Corporate Sector

- Event Management

- By Product Type

- Regional Market Analysis

- North America

- Europe

- Asia-Pacific (Fastest-Growing Region)

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Competitive Analysis

- Key Player Benchmarking

- Strategic Developments

- AI-Driven Personalization & E-commerce Strategies

- Omnichannel Expansion & Logistics Innovation

- Company Profiles

- Amazon.com Inc.

- Alibaba Group

- Walmart Inc.

- Hallmark Cards Inc.

- Etsy Inc.

- Moonpig Group

- Ferns N Petals

- 1-800-Flowers.com

- Shutterfly Inc.

- GiftCards.com

- Strategic Outlook

- Future of AI-Driven Gifting Ecosystem

- Expansion of Experience-Based Gift Models

- Growth of Omnichannel Retail Strategies

- Sustainability in Packaging and Supply Chains

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Gifts Retailing Market Competitive Intensity & Market Structure Overview

The Global Gifts Retailing Market is highly fragmented and intensely competitive, characterized by the coexistence of global e-commerce giants, specialty gifting retailers, luxury brands, and rapidly growing digital-first gifting platforms. Market competition is primarily driven by product personalization capabilities, pricing strategies, delivery speed, omnichannel retail integration, and customer experience innovation.

The competitive landscape is strongly influenced by seasonal demand cycles, including festivals, holidays, weddings, and corporate gifting events, which create periodic spikes in sales activity. This seasonality intensifies competition among retailers to capture peak demand periods through aggressive promotions, exclusive product launches, and fast fulfillment networks.

The market structure is rapidly shifting from traditional brick-and-mortar gifting stores toward digital-first ecosystems powered by e-commerce platforms, AI-based recommendation engines, and data-driven personalization tools. Experience-based gifting and digital gift cards are further reshaping value creation and increasing competition across both product and service categories.

Global Gifts Retailing Market Competitive Intensity & Market Structure Current Scenario

Leading Global Gifts Retailing Companies

- Amazon.com Inc.: The dominant global e-commerce platform offering a wide range of gifting products, fast delivery services, and AI-powered personalized recommendations across multiple categories.

- Alibaba Group: A major global marketplace player enabling cross-border gifting, extensive seller networks, and diversified product offerings across price segments.

- Walmart Inc.: A leading omnichannel retailer leveraging both offline stores and online platforms to serve mass-market gifting demand with strong logistics capabilities.

- Etsy Inc.: A key player specializing in handmade, personalized, and artisanal gifting products, strongly positioned in the customization-driven segment.

- Hallmark Cards Inc.: A traditional gifting brand with strong presence in greeting cards, seasonal gifts, and emotionally driven gifting occasions.

- 1-800-Flowers.com: A prominent online gifting platform specializing in floral arrangements, curated gift baskets, and occasion-based gifting services.

- Ferns N Petals: A leading India-based gifting platform offering flowers, personalized gifts, and same-day delivery services across multiple domestic and international markets.

- Shutterfly Inc.: A personalization-focused company offering customized photo gifts, printed merchandise, and memory-based gifting solutions.

- Moonpig Group: A digital-first greeting card and gifting platform focused on personalized cards and online gifting convenience, particularly in European markets.

- GiftCards.com: A specialized digital gift card platform enabling prepaid gifting solutions across retail, entertainment, and service categories.

Key Competitive Intensity & Market Structure Drivers

Increasing demand for personalization is a major competitive driver, pushing companies to invest in AI-powered customization tools, dynamic product recommendations, and user-specific gifting experiences.

Rapid expansion of e-commerce platforms and mobile commerce is intensifying price competition and forcing retailers to differentiate through logistics speed, user experience, and product variety.

The rise of experience-based gifting is reshaping competition by introducing service-oriented players such as travel, hospitality, and entertainment providers into the gifting ecosystem.

Seasonal demand concentration significantly increases competitive pressure during peak periods, requiring companies to scale supply chains, inventory management, and last-mile delivery capabilities efficiently.

Cross-border e-commerce expansion is increasing global competition, allowing international sellers to compete directly with domestic gifting platforms across multiple regions.

Strategic Implications of Competitive Intensity & Market Structure

Companies with strong AI-driven personalization engines, integrated omnichannel retail capabilities, and robust logistics networks are expected to maintain a competitive advantage in the evolving gifting ecosystem.

Investments in data analytics, customer behavior tracking, and predictive demand forecasting are becoming essential for optimizing seasonal sales performance and inventory planning.

Retailers focusing on premiumization, sustainability, and eco-friendly packaging solutions are likely to gain stronger consumer preference in high-value gifting segments.

Strategic partnerships between e-commerce platforms, logistics providers, and personalization technology firms are enabling faster innovation and improved customer engagement across the value chain.

Organizations capable of combining emotional value creation, digital convenience, and efficient global fulfillment will be best positioned to compete in the increasingly experience-driven global gifts retailing market.

Global Gifts Retailing Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global gifts retailing market is expected to become increasingly digitalized and AI-driven, with personalization technologies playing a central role in shaping future competition.

Growth of social commerce, influencer-driven gifting trends, and mobile-first shopping experiences will further intensify competition among digital platforms and direct-to-consumer brands.

Experience-based gifting is expected to gain stronger market share, introducing new competitive dynamics involving service providers in travel, entertainment, and lifestyle sectors.

Over the forecast period, companies that successfully integrate AI personalization, real-time logistics optimization, and omnichannel retail experiences will be best positioned to capture long-term growth opportunities in the global gifting ecosystem.

Value Chain

Global Gifts Retailing Market Value Chain & Supply Chain Evolution Overview

The Global Gifts Retailing Market operates through a diversified and consumer-driven value chain that includes product design, manufacturing, sourcing, branding, distribution, retail operations, and end-user delivery. The ecosystem is highly dynamic, with demand strongly influenced by cultural events, seasonal festivals, corporate occasions, and personal celebrations.

The value chain is increasingly shaped by digital transformation, with e-commerce platforms, personalization technologies, and AI-driven recommendation systems redefining how gifting products are designed, marketed, and delivered. The rise of experience-based gifting and customized products is also adding new layers of complexity and value creation across the supply chain.

Global Gifts Retailing Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Product Design & Concept Development: Creation of gift concepts including personalized items, luxury products, corporate gifts, and experience-based offerings aligned with consumer trends.

- Raw Material Sourcing & Manufacturing: Procurement of materials such as paper, textiles, metals, ceramics, packaging materials, and digital assets for gift cards and experience vouchers.

- Customization & Personalization: Printing, engraving, digital customization, AI-based personalization, and tailored gift packaging solutions.

- Branding & Product Assembly: Packaging design, gift bundling, branding, quality assurance, and final product preparation.

- Distribution & Logistics: Warehousing, inventory management, fulfillment centers, and last-mile delivery services ensuring timely delivery for events and occasions.

- Retail & Sales Channels: E-commerce platforms, offline retail stores, brand outlets, and specialty gifting stores facilitating consumer access.

- Customer Experience & Fulfillment: Order tracking, digital gift card delivery, subscription gifting services, and customer support systems.

- End User Consumption: Individual consumers, corporate clients, and event organizers purchasing gifts for personal, professional, and social occasions.

Company-to-Stage Mapping

- Product Design & Concept Development: Etsy sellers, Hallmark design teams, luxury gifting brands, and creative studios.

- Manufacturing: Global manufacturers of consumer goods, artisanal producers, packaging companies, and merchandise suppliers.

- Customization & Personalization: Shutterfly Inc., Etsy, Moonpig Group, Amazon Custom, and personalization service providers.

- Branding & Assembly: Hallmark Cards Inc., Ferns N Petals, 1-800-Flowers.com, and premium gifting brands.

- Distribution & Logistics: Amazon Logistics, Alibaba logistics network, DHL eCommerce, FedEx, and regional courier services.

- Retail & Sales Channels: Amazon.com Inc., Alibaba Group, Walmart Inc., Etsy Inc., and offline retail chains.

- Customer Experience & Fulfillment: Digital gifting platforms, subscription gifting services, and omnichannel retail systems.

- End User Consumption: Individual consumers, corporate buyers, event planners, and institutional gifting programs worldwide.

Key Value Chain & Supply Chain Evolution Signals

- Growth of Personalization Technologies: AI-driven customization tools are enabling highly tailored gifting experiences across digital platforms.

- Expansion of E-Commerce Dominance: Online platforms are becoming the primary channel for gifting due to convenience, variety, and fast delivery.

- Rise of Experience-Based Gifting: Non-physical gifts such as travel, dining, and entertainment experiences are reshaping demand patterns.

- Strengthening of Omnichannel Retail Models: Integration of offline and online channels is improving customer engagement and fulfillment efficiency.

- Advancement of Digital Gift Cards: Instant delivery and digital gifting solutions are gaining popularity across corporate and personal segments.

- Focus on Sustainable Packaging: Eco-friendly packaging materials are becoming an important part of gifting supply chains.

Strategic Implications of Value Chain Evolution

- Investment in AI-Based Personalization: Companies leveraging AI tools can significantly enhance customer engagement and conversion rates.

- Expansion of E-Commerce Infrastructure: Strong logistics and fulfillment capabilities are critical for timely delivery and customer satisfaction.

- Growth of Experience Gifting Platforms: Service-based gifting models are opening new high-growth revenue streams.

- Strengthening Omnichannel Presence: Integrated retail strategies improve reach across digital and physical channels.

- Adoption of Sustainable Practices: Eco-friendly packaging and responsible sourcing enhance brand value and consumer trust.

- Enhancement of Subscription-Based Gifting Models: Recurring gifting services are creating long-term customer relationships and stable revenue.

Global Gifts Retailing Market Value Chain & Supply Chain Evolution Forward Outlook

- Expansion of AI-driven hyper-personalized gifting solutions.

- Rapid growth of digital gift cards and instant gifting platforms.

- Increased dominance of e-commerce and social-commerce channels.

- Rising adoption of experience-based gifting ecosystems.

- Strengthening of global logistics networks for faster delivery.

- Growth of sustainable and eco-friendly gifting supply chains.

The gifts retailing value chain is expected to become more digital, personalized, and experience-oriented, driven by evolving consumer expectations and technological advancements. Speed, customization, and convenience will remain key competitive differentiators across the industry.

Companies that effectively combine AI-driven personalization, efficient logistics, omnichannel retail strategies, and innovative gifting experiences will be best positioned for long-term success in the Global Gifts Retailing Market.

Investment Activity

Global Gifts Retailing Market Investment & Funding Dynamics Overview (2026???2033)

The Global Gifts Retailing Market is attracting steady investment momentum driven by the rapid expansion of e-commerce platforms, rising consumer spending on celebrations, and increasing demand for personalized and experience-based gifting. Investors including private equity firms, venture capital funds, e-commerce giants, retail chains, and digital commerce startups are actively allocating capital toward personalized gifting platforms, AI-driven recommendation engines, digital gift card ecosystems, logistics automation, and omnichannel retail infrastructure.

Funding activity is increasingly concentrated in technology-enabled gifting solutions that enhance customer experience, streamline fulfillment, and enable hyper-personalization. Significant capital is flowing into e-commerce gifting marketplaces, AI-based personalization tools, subscription gifting services, and cross-border gifting platforms.

Additionally, growing investments in last-mile delivery networks, sustainable packaging solutions, cloud-based retail infrastructure, and experience-based gifting platforms are reshaping the global gifting ecosystem and strengthening long-term market scalability.

Current Investment & Funding Landscape

The current market landscape is defined by strong digital transformation across retail gifting channels, with e-commerce platforms dominating capital allocation strategies. Major online retailers are investing heavily in AI-powered personalization engines, dynamic pricing systems, and data-driven customer engagement platforms.

Specialized gifting companies and startups are attracting venture capital funding for customized gifting solutions, digital gift card platforms, and experience-based gifting services such as travel, dining, and entertainment packages.

Strategic collaborations between e-commerce platforms, logistics providers, payment gateways, and retail brands are further strengthening the gifting ecosystem and improving operational efficiency across distribution channels.

Key Investment & Funding Dynamics Signals

- Rising demand for personalized and experience-based gifting solutions is driving technology-focused investments.

- Expansion of e-commerce platforms and digital marketplaces is attracting significant venture capital and corporate funding.

- Increasing adoption of AI-driven recommendation engines and personalization tools is enhancing retail technology investments.

- Growth of digital gift cards and subscription-based gifting models is creating new revenue streams and funding opportunities.

- Rising importance of fast delivery and last-mile logistics infrastructure is boosting supply chain investments.

- Expansion of cross-border gifting and global retail platforms is increasing international capital flows.

- Growing focus on sustainable packaging and eco-friendly retail practices is influencing ESG-oriented investments.

Strategic Implications of Investment & Funding Dynamics

- Companies investing in AI-powered personalization and customer experience technologies are expected to gain strong competitive advantage.

- Capital allocation toward omnichannel retail infrastructure will strengthen market reach and customer engagement.

- Firms focusing on experience-based and subscription gifting models are likely to capture faster revenue growth.

- Strategic partnerships between e-commerce platforms, logistics companies, and payment providers will accelerate ecosystem efficiency.

- Investment in digital commerce infrastructure and automated fulfillment systems will remain a key driver of scalability.

- Compliance with consumer protection laws, e-commerce regulations, and cross-border trade policies will continue shaping investment strategies.

- Organizations integrating data analytics, personalization, and logistics optimization will capture higher long-term value.

Forward Outlook

Looking ahead, the Global Gifts Retailing Market is expected to witness stable investment growth driven by digital commerce expansion, rising gifting culture, and increasing demand for personalized and experience-driven products. Capital deployment will increasingly focus on AI-enabled personalization platforms, omnichannel retail ecosystems, digital gifting solutions, and logistics innovation.

Future funding will also be supported by growing adoption of subscription-based gifting models, cross-border e-commerce expansion, and integrated customer experience platforms across global retail networks.

As consumer behavior continues to shift toward convenience, personalization, and emotional value-based purchasing, investment activity will expand across digital marketplaces, retail technology, fulfillment infrastructure, and experience economy platforms.

In conclusion, the Global Gifts Retailing Market represents a digitally driven consumer retail investment landscape where personalization, e-commerce expansion, logistics innovation, and experience-based gifting models will define future funding priorities and long-term industry growth.

Technology & Innovation

Global Gifts Retailing Market Technology & Innovation Landscape Overview

The global gifts retailing market is experiencing rapid technological transformation driven by advancements in e-commerce personalization engines, AI-based recommendation systems, digital payment ecosystems, supply chain automation, and omnichannel retail platforms. As consumer expectations shift toward convenience and customization, retailers are increasingly adopting digital-first strategies to enhance engagement and conversion rates.

Modern gifting platforms are integrating artificial intelligence, data analytics, augmented reality (AR) visualization tools, and customer behavior tracking systems to deliver highly personalized product recommendations. These technologies are improving purchase relevance, emotional appeal, and customer retention across both physical and digital retail channels.

The market is also witnessing strong adoption of digital gift cards, mobile commerce applications, cloud-based retail management systems, and automated fulfillment and logistics solutions, which are enhancing operational efficiency, delivery speed, and global scalability of gifting platforms.

Global Gifts Retailing Market Technology & Innovation Current Scenario

Current innovation in the gifts retailing market is primarily focused on personalization technologies, digital commerce expansion, and experience-based gifting platforms. Retailers are leveraging data-driven insights to understand consumer preferences and optimize product offerings across seasonal and event-based demand cycles.

AI-powered recommendation engines are widely used across e-commerce platforms to suggest personalized gifts based on browsing history, purchase behavior, and demographic patterns.

Digital gifting ecosystems such as e-gift cards, instant delivery gifts, and subscription-based gifting models are gaining strong traction due to convenience and flexibility.

Advanced logistics and supply chain technologies, including warehouse automation, route optimization, and real-time tracking systems, are improving delivery performance and reducing fulfillment costs.

Additionally, social commerce platforms and mobile-first retail applications are playing a key role in driving impulse gifting behavior, especially among younger consumers.

Key Technology & Innovation Trends in Global Gifts Retailing Market

- AI-Driven Personalization: Smart recommendation systems for tailored gifting experiences.

- Digital Gift Cards & E-Gifting Platforms: Instant, flexible, and cashless gifting solutions.

- Experience-Based Gifting Technologies: Platforms offering travel, dining, and activity-based gift experiences.

- Omnichannel Retail Integration: Seamless blending of online and offline gifting experiences.

- Advanced E-Commerce Analytics: Behavioral insights for demand forecasting and customer targeting.

- Automation in Fulfillment & Logistics: Faster delivery and optimized supply chain operations.

- Augmented Reality (AR) Shopping Tools: Virtual visualization of personalized and luxury gifts.

- Mobile Commerce Expansion: App-based gifting platforms enabling on-the-go purchases.

- Subscription-Based Gifting Models: Recurring gifting services for corporate and personal use.

- Sustainable Packaging Innovations: Eco-friendly materials and green retail practices.

Strategic Implications of Technology & Innovation

Technological advancements are reshaping the gifts retailing market into a highly personalized, digitally connected, and experience-driven retail ecosystem. Retailers that effectively integrate AI, automation, and omnichannel strategies are gaining stronger competitive positioning.

Companies investing in data-driven personalization, digital gifting infrastructure, and logistics automation are improving customer engagement, conversion rates, and operational efficiency.

The convergence of social media influence, mobile commerce, and AI-based marketing is significantly increasing impulse buying behavior and expanding global gifting occasions.

However, challenges such as high logistics costs, cross-border regulatory complexities, data privacy concerns, and seasonal demand volatility continue to influence market strategies and operational planning.

Global Gifts Retailing Market Technology & Innovation Forward Outlook

The future of the gifts retailing market is expected to evolve toward fully digitalized, AI-powered, and experience-centric gifting ecosystems supported by advanced personalization technologies and integrated retail platforms.

Emerging innovations include hyper-personalized AI gifting assistants, immersive AR/VR shopping experiences, blockchain-based gift verification systems, and automated global fulfillment networks.

Experience-based gifting is expected to expand significantly as consumers increasingly prioritize emotional value, convenience, and unique experiences over physical products.

Overall, the global gifts retailing market is transforming into a dynamic digital commerce ecosystem where artificial intelligence, automation, and consumer-centric innovation are redefining how gifts are discovered, purchased, and delivered worldwide.

Market Risk

Global Gifts Retailing Market Risk Factors & Disruption Threats Overview

The Global Gifts Retailing Market operates within a highly seasonal and sentiment-driven consumer environment influenced by cultural events, festivals, corporate demand, and personal celebrations. While growth is supported by rising e-commerce penetration, increasing personalization trends, and expanding experience-based gifting, the market faces structural risks related to demand volatility, intense price competition, supply chain inefficiencies, and shifting consumer preferences.

A major structural risk is the high seasonality of demand, where sales are heavily concentrated around holidays, festivals, weddings, and corporate gifting cycles. This creates revenue volatility and inventory management challenges for retailers throughout the year.

Another key disruption factor is increasing competition from e-commerce platforms and direct-to-consumer brands, which intensifies pricing pressure and reduces margins, especially for standardized and non-premium gift categories.

The market is also exposed to supply chain and logistics disruptions, particularly for customized gifts, cross-border shipments, and time-sensitive deliveries during peak seasonal demand periods.

Additionally, rapid shifts in consumer preferences toward digital gifts, experience-based gifting, and subscription models are disrupting traditional physical gift categories and reshaping product demand patterns.

Global Gifts Retailing Market Risk Factors & Disruption Threats Current Scenario

The current market is characterized by strong growth in e-commerce-based gifting platforms, personalization technologies, and curated gift experiences supported by AI-driven recommendation systems.

Seasonal demand spikes during festivals, holidays, and corporate events continue to drive the majority of revenue, placing significant pressure on inventory planning, logistics capacity, and fulfillment efficiency.

Retailers are increasingly investing in digital transformation, omnichannel retailing, and automated supply chain systems to manage fluctuating demand and improve customer experience.

At the same time, consumer expectations for faster delivery, customization, and premium packaging are increasing operational complexity and cost structures for market participants.

Competition is intensifying as global marketplaces, niche gifting platforms, and luxury retailers expand their digital presence and enhance personalization capabilities.

Key Risk Factors & Disruption Threats Signals in Global Gifts Retailing Market

A major disruption signal is the rapid shift toward experience-based gifting, including travel, events, and subscription services, reducing reliance on traditional physical gift products.

Another important signal is the growing dominance of e-commerce platforms in gifting distribution, enabling algorithm-driven personalization and global product accessibility.

The increasing adoption of AI-powered recommendation engines and customer data analytics is reshaping how consumers discover and purchase gifts online.

Rising demand for same-day and next-day delivery services is transforming logistics models and increasing dependence on highly efficient fulfillment networks.

Additionally, growing environmental awareness is driving demand for sustainable packaging and eco-friendly gifting solutions across global markets.

Strategic Implications of Risk Factors & Disruption Threats in Global Gifts Retailing Market

Retailers must prioritize supply chain agility, inventory optimization, and demand forecasting systems to manage seasonal fluctuations effectively and reduce operational inefficiencies.

Investment in AI-driven personalization, customer behavior analytics, and digital engagement platforms will be essential for improving conversion rates and customer retention.

Companies should strengthen omnichannel strategies by integrating online platforms with offline retail experiences to enhance accessibility and brand engagement.

Expansion of logistics capabilities, including faster delivery networks and localized fulfillment centers, will be critical for meeting rising consumer expectations.

Strategic partnerships with e-commerce platforms, payment providers, and logistics companies will play a key role in improving scalability and global reach.

Global Gifts Retailing Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Gifts Retailing Market is expected to evolve toward highly personalized, digitally driven, and experience-oriented gifting ecosystems.

E-commerce platforms will continue to dominate distribution, supported by AI-based personalization, predictive analytics, and automated recommendation systems that enhance customer engagement.

Experience-based gifting and digital gift cards are expected to gain further traction, gradually reshaping the balance between physical and non-physical gift categories.

Logistics innovation, including faster fulfillment networks and advanced last-mile delivery solutions, will play a central role in improving customer satisfaction during peak demand periods.

Overall, the market will remain growth-oriented but increasingly shaped by digital transformation, seasonal demand volatility, logistics efficiency, and evolving consumer behavior. Long-term leaders will be defined by their ability to deliver highly personalized, convenient, and emotionally engaging gifting experiences across global markets.

Regulatory Landscape

Global Gifts Retailing Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Gifts Retailing Market is shaped by a combination of consumer protection frameworks, digital commerce regulations, taxation policies, and cross-border trade rules. As gifting increasingly shifts toward online and cross-border e-commerce platforms, regulatory oversight is expanding to ensure transparency, product safety, fair trade practices, and secure digital transactions.

Gifts retailers, e-commerce platforms, logistics providers, payment gateways, and manufacturers must comply with regulations covering consumer rights, product labeling, import-export restrictions, data privacy, taxation compliance, and online marketplace governance. The rise of personalized gifts and digital gifting solutions has further introduced regulatory considerations related to intellectual property, customization data handling, and digital payment security.

Government authorities are increasingly focusing on strengthening e-commerce ecosystems, improving consumer trust, and ensuring fair competition across both online and offline retail channels. This is particularly important in a market characterized by high seasonal demand and cross-border transactions.

Global Gifts Retailing Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by strong emphasis on consumer protection, e-commerce governance, and digital transaction security. Consumer protection laws ensure that customers receive accurate product information, fair pricing, transparent return policies, and protection against fraudulent practices in both physical and online retail environments.

E-commerce regulations play a central role in shaping the digital gifting ecosystem. Online platforms are required to maintain transparency in seller listings, pricing algorithms, refund policies, and customer grievance mechanisms. These regulations are increasingly important due to the dominance of digital platforms in gift retailing.

Cross-border trade policies significantly influence the import and export of gifting products, particularly luxury gifts, personalized items, and seasonal merchandise. Customs regulations, tariffs, and international trade agreements impact pricing, availability, and delivery timelines in global gifting markets.

Taxation frameworks, including value-added tax (VAT), goods and services tax (GST), and digital service taxes, also play a critical role in shaping pricing strategies and profitability for retailers operating across multiple jurisdictions.

Additionally, regulations related to product safety, packaging standards, and labeling requirements ensure that gifting products meet quality expectations and comply with health and environmental standards.

Key Regulatory & Policy Environment Signals in Global Gifts Retailing Market

- Consumer Protection Laws: Regulations ensuring fair pricing, transparent returns, product authenticity, and grievance redressal mechanisms.

- E-Commerce Regulations: Governance frameworks for online marketplaces covering seller accountability, pricing transparency, and platform liability.

- Cross-Border Trade Policies: Import/export rules, tariffs, and customs regulations affecting international gifting trade flows.

- Taxation & Digital Commerce Taxes: GST, VAT, and digital taxation policies impacting pricing and platform operations.

- Product Safety & Labeling Standards: Requirements ensuring quality assurance, material disclosure, and consumer safety compliance.

- Data Privacy & Digital Payment Regulations: Rules governing customer data protection, online transactions, and secure payment processing.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging retailers and digital platforms to prioritize compliance, transparency, and customer trust. Strong regulatory adherence is becoming a key differentiator in highly competitive e-commerce-driven gifting markets.

Consumer protection laws are increasing accountability for both online and offline retailers, driving improvements in product authenticity, return policies, and customer service standards. Companies that fail to comply risk reputational damage and reduced consumer confidence.

E-commerce regulations are pushing platforms to improve seller verification systems, enhance fraud detection mechanisms, and provide more transparent pricing and recommendation systems. This is reshaping digital gifting ecosystems.

Cross-border trade regulations are influencing global expansion strategies, encouraging companies to optimize logistics networks, manage tariff impacts, and establish localized distribution hubs to improve delivery efficiency.

Data privacy and digital payment regulations are driving investments in secure transaction systems, encrypted payment gateways, and compliance-focused customer data management platforms, particularly in personalized gifting services.

Global Gifts Retailing Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global gifts retailing market is expected to become more structured and digitally focused as e-commerce continues to dominate retail distribution. Governments are likely to introduce stricter frameworks for online marketplace governance, cross-border digital trade, and consumer data protection.

E-commerce regulations are expected to evolve toward greater platform accountability, improved transparency in recommendation algorithms, and stronger protections against counterfeit and misleading product listings.

Cross-border trade policies may become more harmonized in certain regions, facilitating smoother international gifting flows and reducing friction in customs clearance processes for small parcels and personalized goods.

Taxation systems are expected to further adapt to digital commerce growth, with expanded coverage of online transactions, platform-based taxation models, and improved enforcement mechanisms.

Overall, the future regulatory landscape will be shaped by the convergence of consumer protection laws, e-commerce governance frameworks, cross-border trade policies, taxation systems, and digital payment regulations. Companies that prioritize compliance, transparency, secure transactions, and efficient global logistics will be best positioned to capitalize on long-term opportunities in the evolving global gifts retailing market.